Cardiac Amyloidosis Market Size - Analysis

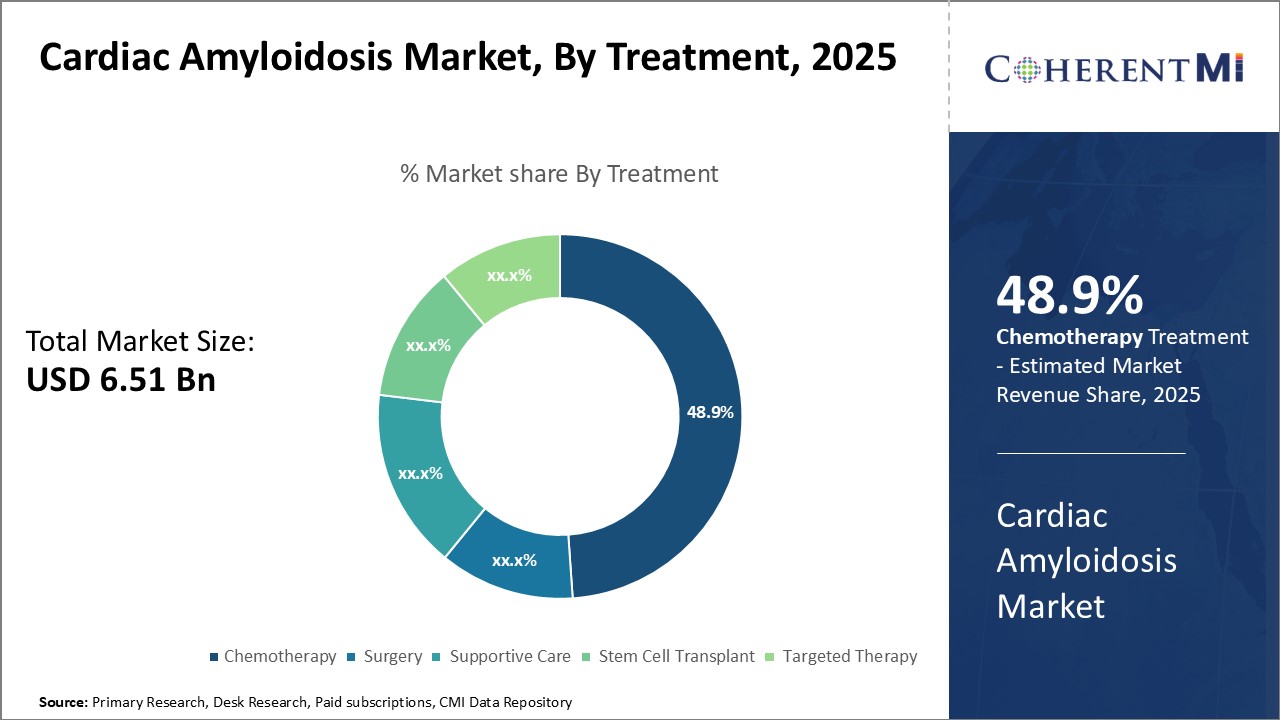

The Global Cardiac Amyloidosis Market is estimated to be valued at USD 6.51 Bn in 2025 and is expected to reach USD 10.05 Bn by 2032, growing at a compound annual growth rate (CAGR) of 6.4% from 2025 to 2032.

Market Size in USD Bn

CAGR6.4%

| Study Period | 2025-2032 |

| Base Year of Estimation | 2024 |

| CAGR | 6.4% |

| Market Concentration | High |

| Major Players | Pfizer, Alnylam Pharmaceuticals, Alexion Pharmaceuticals/Eidos Therapeutics, Ionis Pharmaceuticals, AstraZeneca and Among Others |

please let us know !

Cardiac Amyloidosis Market Trends

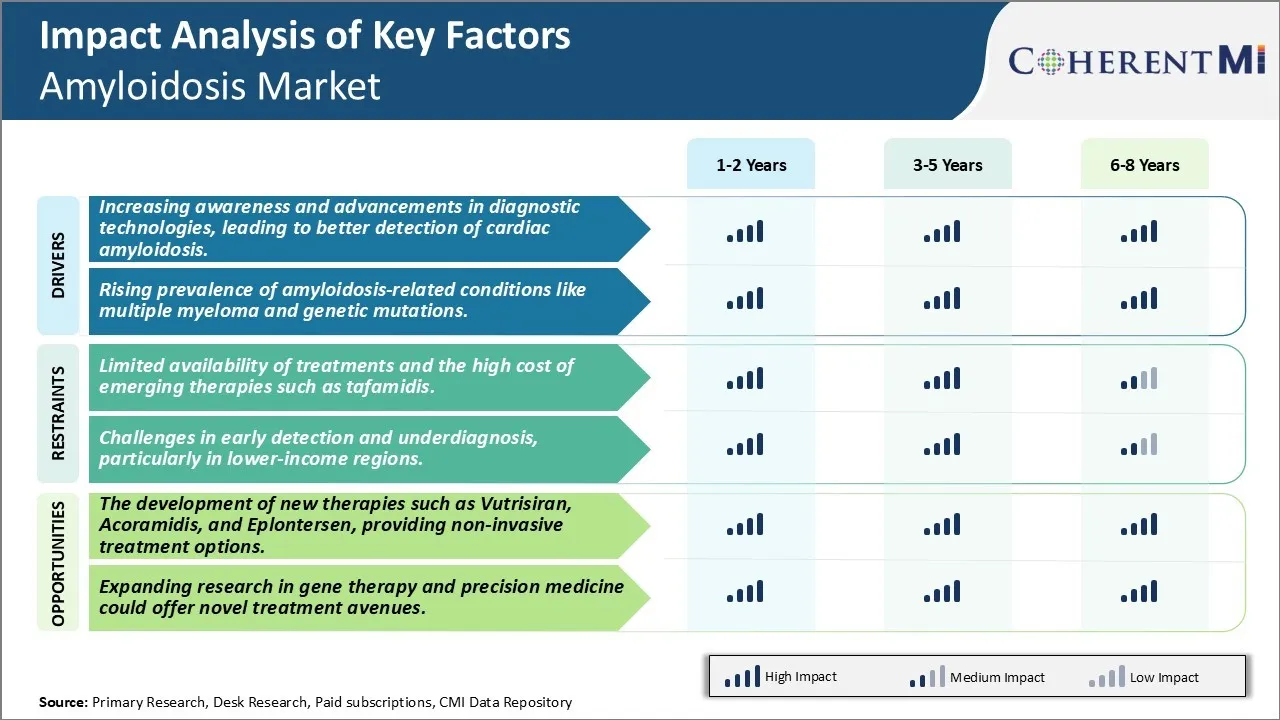

With time, more awareness about cardiac amyloidosis is being created among the medical community as well as general public. Several non-profit organizations as well as government agencies are consistently making efforts to educate people about the importance of early diagnosis of this rare disease. Various awareness campaigns focusing on signs and symptoms of cardiac amyloidosis have helped many patients in realizing that something could be wrong with their heart which has driven the need for consulting doctors. This increase in awareness is further emphasized by the advancements seen in diagnostic technologies in recent years.

The risk factors connected with rising incidence of amyloidosis include increasing prevalence of other diseases known to be associated with it. For instance, the numbers of multiple myeloma cases have gone up in recent years. Multiple myeloma, a cancer of plasma cells is a major cause of AL amyloidosis. Statistics show multiple myeloma occurrences have doubled in the past few decades. Its higher rates naturally translate to elevated amyloidosis caused due to multiple myeloma. Genetic predisposition is another notable risk aspect. Certain gene mutations are linked to inheritance of AA amyloidosis and other types. With advanced understanding of such genetic links, more patients with related hereditary traits are being diagnosed preemptively. Evidence links inflammatory diseases to AA amyloidosis as well. Persistently increasing global incidence of debilitating conditions like rheumatoid arthritis which promote inflammation drive up AA amyloidosis risk. Aging population demographics too contribute as amyloidosis is predominantly a disease affecting older adults. The growing geriatric population cohort expands the number of potential new patients. These trends in adjacent disease landscapes directly influence the rising prevalence of amyloidosis and pose a continued threat.

The Cardiac Amyloidosis Market currently faces significant challenges due to limited availability of effective treatment options and the rising costs of emerging therapies. There are only a few drugs approved for the treatment of amyloidosis and many patients do not respond well or cannot tolerate existing options such as chemotherapy and stem cell transplants. This leaves a major unmet need for novel, more targeted therapies. While promising new drugs like tafamidis offer improved outcomes, their high list prices put them out of reach for many patients and healthcare systems. Tafamidis, for example, costs over USD 225,000 per year in the US. Such exponentially higher drug costs compared to existing standards of care could prove unsustainable for markets and public drug plans. This pricing challenges the ability of patients with rare diseases to access life-changing cures.

Market Opportunity: Development of New Non-Invasive Therapies Creates New Avenues for Market Growth.

Prescribers preferences of Cardiac Amyloidosis Market

Cardiac Amyloidosis typically progresses through three stages - early, middle, and late-stage disease. In early stage, when symptoms are mild, prescribers typically recommend lifestyle modifications like diet, exercise and monitoring of medication intake to control other comorbidities like blood pressure.

In late-stage disease, when the above medications start becoming ineffective, prescribers consider stem cell transplantation (SCT) as the main treatment approach. SCT has shown to halt progression and even enable remission if performed early enough. Prescribers prefer to recommend SCT when organs are still functioning adequately and the patient is otherwise physically fit. Before recommending SCT, prescribers also consider factors like availability of donor, affordability and post-SCT medical support system required.

Treatment Option Analysis of Cardiac Amyloidosis Market

Cardiac Amyloidosis has four main stages - Stage 1 involves no symptoms, Stage 2 includes mild heart strain, Stage 3 presents moderate strain with possible mild heart failure, and Stage 4 features severe strain and heart failure.

As the disease progresses to Stage 3, standard heart failure medications like ACE inhibitors or ARBs are prescribed to control blood pressure and reduce strain. Mineralocorticoid receptor antagonists like spironolactone may also be used. For light strain, this combination is preferred due to minimal side effects.

In summary, treatments are tailored based on disease stage and symptom severity, focusing first on underlying causes then optimizing heart function. Lifestyle changes and monitoring alone address early Stage 1, while later Stages 3 and 4 require multidrug therapy plus experimental options to improve quality of life.

Key winning strategies adopted by key players of Cardiac Amyloidosis Market

Focus on Developing Novel Treatments: Developing novel disease-modifying therapies is a key strategy adopted by major players to gain an edge in the market. For example, in 2020, Alnylam Pharmaceuticals launched Oxlumo (lumasiran) for Primary Hyperoxaluria Type 1 (PH1), the first and only approved RNAi therapeutic for this rare disease. Oxlumo demonstrated significant reductions in urinary oxalate and enhanced kidney preservation in clinical trials. This drug approval established Alnylam as the leader in developing transformative therapies for amyloidosis disorders.

Strategic Collaborations and M&As: Partnerships allow players to gain access to new pipeline assets, technologies and broader geographical reach. For example, Ionis Pharmaceuticals collaborated with Pfizer to develop RNA-targeted therapies for ATTR amyloidosis and acquired Akcea Therapeutics in 2019 to expand its rare disease business. This helped Ionis emerge as a major player in the field.

Segmental Analysis of Cardiac Amyloidosis Market

Insights, By Treatment, Chemotherapy is Expected to Drive Treatment Adoption in the Forecast Period.

Insights, By Treatment, Chemotherapy is Expected to Drive Treatment Adoption in the Forecast Period.By Treatment, chemotherapy contributes the highest share of the market. However, its therapeutic scope is being enhanced by the advent of Targeted Therapy. Chemotherapeutic regimens continue to be central to AL amyloidosis treatment due to their ability to directly cytoreduce the aberrant plasma cell population. Nevertheless, chemotherapy also causes non-specific cytotoxicity, limiting drug doses and negatively impacting quality of life. Targeted therapies now supplement chemotherapy by offering mechanisms to disrupt pathogenic light chain production and amyloid formation more selectively. Drugs such as proteasome inhibitors reduce misfolded protein load in the endoplasmic reticulum, alleviating plasma cell stress. Immunomodulators regulate pathogenic immunoglobulin expression through epigenetic changes. Monoclonal antibodies help clear amyloid deposits and facilitate tissue repair. These targeted agents allow lower cytotoxic exposures while improving treatment outcomes. Their availability is helping optimize chemotherapy regimens and enhance disease control, thus driving the market for combination regimens.

By End-user, Hospitals contribute the highest share of the market. This can be attributed to the vulnerable patient demographics who typically suffer from AL amyloidosis. The disease commonly affects the elderly and is associated with decreased performance status due to organ dysfunction often involving the heart, kidneys and liver. Its nonspecific clinical manifestations also pose diagnostic challenges requiring specialized multidisciplinary teams. Initial symptom misattribution further risks disease progression before definitive diagnosis and treatment. Given the involvement of multiple critical organ systems, patients generally require in-hospital management under close physician supervision. They benefit from the elaborate diagnostic facilities, round-the-clock monitoring and multi-specialty consultative support provided preferentially by tertiary or quaternary care facilities. Additionally, the nature of chemotherapeutic regimens necessitates administration within the hospital setting. The concentration of infrastructure and expertise in hospitals to address the complex needs of AL amyloidosis patients struggling with disability thereby sustains their leading role as preferred sites of amyloidosis case management.

Additional Insights of Cardiac Amyloidosis Market

Cardiac amyloidosis is a progressive and often underdiagnosed condition characterized by the deposition of amyloid fibrils in heart tissue, leading to heart failure and related complications. It predominantly affects older adults, with prevalence rates increasing significantly in individuals over 70 years old. Transthyretin amyloidosis (ATTR-CM) is the most common form of cardiac amyloidosis, accounting for over 80% of cases, while light-chain amyloidosis (AL-CM) remains a rarer form. Recent advancements in diagnostic techniques, such as non-invasive imaging and genetic testing, have contributed to better diagnosis rates. However, treatment options are still limited, with Pfizer’s VYNDAQEL being one of the few approved therapies. Emerging treatments like Acoramidis, Vutrisiran, and Eplontersen are expected to address some of the unmet needs, offering new hope for patients. As more therapies gain regulatory approval, the market is expected to experience steady growth, particularly in the US and Japan, where regulatory approvals have been more forthcoming. The introduction of new drugs and improved diagnostic tools presents a promising outlook for the future of cardiac amyloidosis treatment.

Competitive overview of Cardiac Amyloidosis Market

The major players operating in the Cardiac Amyloidosis Market include Pfizer, Alnylam Pharmaceuticals, Alexion Pharmaceuticals, Ionis Pharmaceuticals, AstraZeneca, BridgeBio Pharma, Novartis AG, Bristol-Myers Squibb Company, Sanofi SA, Ionis Pharmaceuticals, Eidos Therapeutics, Oncopeptides AB and Celegene Corporation.

Cardiac Amyloidosis Market Leaders

- Pfizer

- Alnylam Pharmaceuticals

- Alexion Pharmaceuticals/Eidos Therapeutics

- Ionis Pharmaceuticals

- AstraZeneca

Cardiac Amyloidosis Market - Competitive Rivalry

Cardiac Amyloidosis Market

(Dominated by major players)

(Highly competitive with lots of players.)

Recent Developments in Cardiac Amyloidosis Market

- In December 2023, BridgeBio Pharma submitted an NDA for Acoramidis to the FDA for treating transthyretin amyloidosis cardiomyopathy (ATTR-CM), which is expected to improve patient outcomes and broaden treatment availability.

- In May 2019, Pfizer's VYNDAQEL received FDA approval for treating cardiomyopathy caused by transthyretin amyloidosis (ATTR-CM), marking a milestone for non-invasive treatment options.

- In March 2019, VYNDAQEL received approval in Japan under the SAKIGAKE designation, further expanding its market potential in Asia for the treatment of ATTR-CM.

Cardiac Amyloidosis Market Segmentation

- By Product Type

- Light Chain Amyloidosis (AL-CM)

- Transthyretin Amyloidosis (ATTR-CM)

- By Treatment

- Chemotherapy

- Surgery

- Supportive Care

- Stem Cell Transplant

- Targeted Therapy

- By End-user

- Hospitals

- Ambulatory Surgical Centers

- Clinics

Would you like to explore the option of buying individual sections of this report?

Ghanshyam Shrivastava - With over 20 years of experience in the management consulting and research, Ghanshyam Shrivastava serves as a Principal Consultant, bringing extensive expertise in biologics and biosimilars. His primary expertise lies in areas such as market entry and expansion strategy, competitive intelligence, and strategic transformation across diversified portfolio of various drugs used for different therapeutic category and APIs. He excels at identifying key challenges faced by clients and providing robust solutions to enhance their strategic decision-making capabilities. His comprehensive understanding of the market ensures valuable contributions to research reports and business decisions.

Ghanshyam is a sought-after speaker at industry conferences and contributes to various publications on pharma industry.

Frequently Asked Questions :

How Big is the Cardiac Amyloidosis Market?

The Global Cardiac Amyloidosis Market is estimated to be valued at USD 6.51 Bn in 2025 and is expected to reach USD 10.05 Bn by 2032.

What will be the CAGR of the Cardiac Amyloidosis Market?

The CAGR of the Cardiac Amyloidosis Market is projected to be 6.2% from 2024-2031.

What are the major factors driving the Cardiac Amyloidosis Market growth?

The increasing awareness and advancements in diagnostic technologies, leading to better detection of cardiac amyloidosis and rising prevalence of amyloidosis-related conditions like multiple myeloma and genetic mutations are the major factors driving the Cardiac Amyloidosis Market.

What are the key factors hampering the growth of the Cardiac Amyloidosis Market?

The limited availability of treatments and the high cost of emerging therapies such as tafamidis and challenges in early detection and underdiagnosis, particularly in lower-income regions are the major factor hampering the growth of the Cardiac Amyloidosis Market.

Which is the leading Product Type in the Cardiac Amyloidosis Market?

Light Chain Amyloidosis (AL-CM) is the leading Product Type segment.

Which are the major players operating in the Cardiac Amyloidosis Market?

Pfizer, Alnylam Pharmaceuticals, Alexion Pharmaceuticals, Ionis Pharmaceuticals, AstraZeneca, BridgeBio Pharma, Novartis AG, Bristol-Myers Squibb Company, Sanofi SA, Ionis Pharmaceuticals, Eidos Therapeutics, Oncopeptides AB, Celegene Corporation are the major players.