Diabetic Macular Edema Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Diabetic Macular Edema Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Diabetic Macular Edema Market is segmented By Drug Type (Ranibizumab, Aflibercept, Dexamethasone), By Form (Intravitreal Injections, Intravitreal Implants), By Distribution Channel (Hospitals, Specialty Clinics, Pharmacies), By Geography (North America, Latin America, Asia Pacific, Europe, Middle East, and Africa). The report offers the value (in USD billion) for the above-mentioned.

Diabetic Macular Edema Market is segmented By Drug Type (Ranibizumab, Aflibercept, Dexamethasone), B...

Diabetic Macular Edema Market Size - Analysis

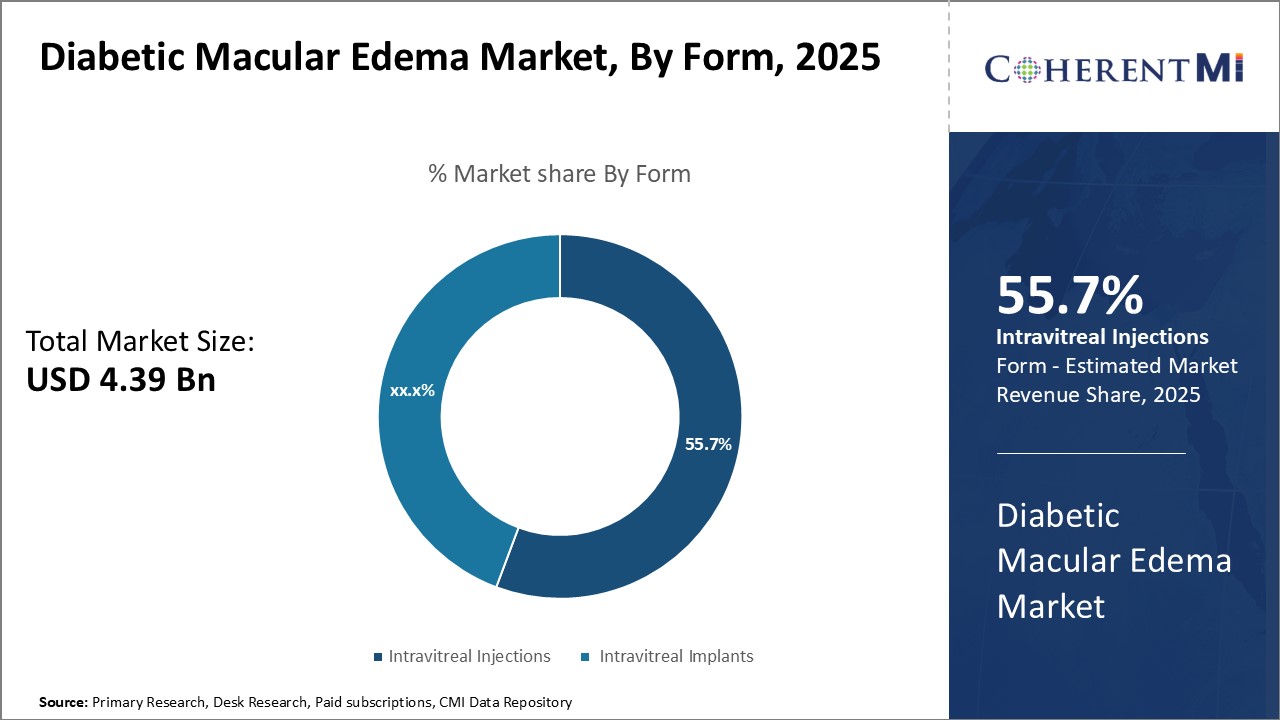

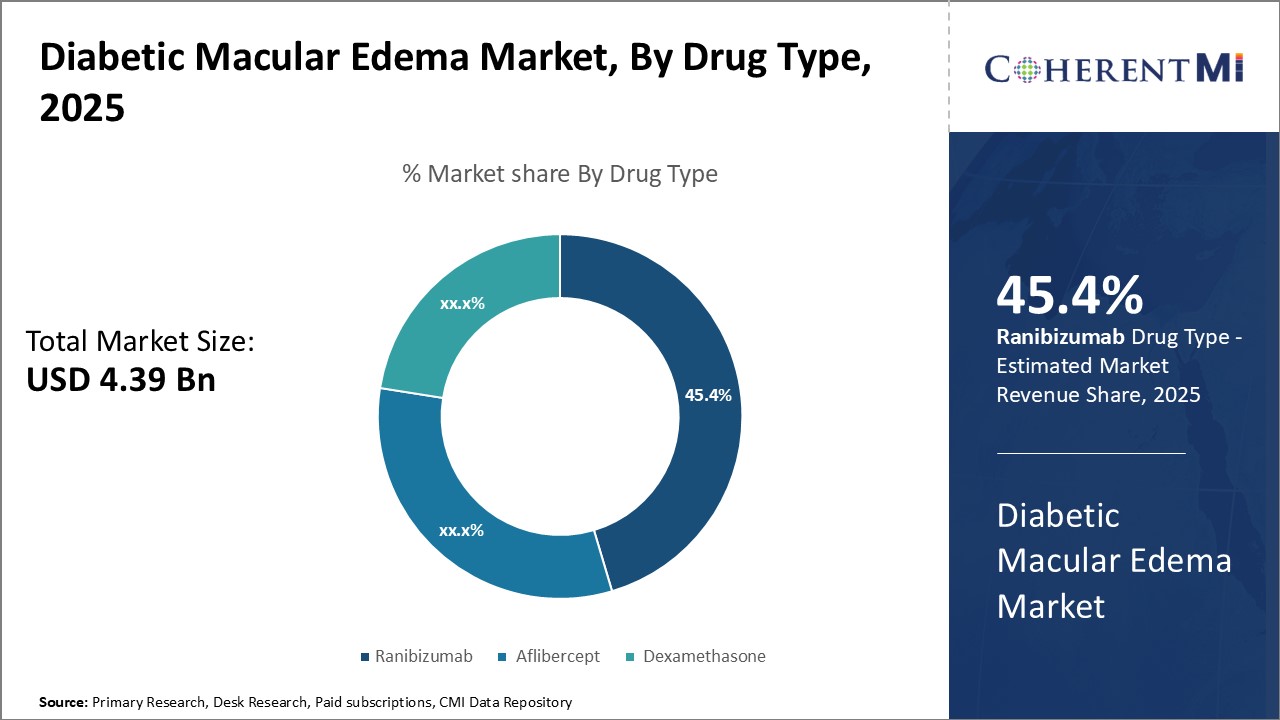

The Global Diabetic Macular Edema Market is estimated to be valued at USD 4.39 Billion in 2025 and is expected to reach USD 5.93 Billion by 2032, growing at a compound annual growth rate (CAGR) of 4.4% from 2025 to 2032.

The market is witnessing positive growth trends over the period. Increasing prevalence of diabetes worldwide along with rise in obese and geriatric population are major factors responsible for the growth of diabetic macular edema market. Accelerated approvals and launches of novel drugs and expanding healthcare infrastructure in emerging markets also support the market expansion. The diabetic macular edema (DME) market is driven by the increasing prevalence of diabetes, leading to a growing number of patients with vision complications. DME is a leading cause of vision loss in diabetic patients, characterized by fluid accumulation in the macula. Key treatments include anti-VEGF therapies such as ranibizumab (Lucentis), aflibercept (Eylea), and corticosteroids like dexamethasone implants. The market is witnessing growth due to advances in these treatments and an aging global population. However, challenges include high costs of therapies, treatment adherence issues, and limited access in developing regions, impacting patient outcomes and market penetration.

Market Size in USD Bn

CAGR4.4%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

4.4%

Market Concentration

High

Major Players

Kodiak Sciences, Roche/Genentech, Regeneron Pharmaceuticals, Gene Signal, Inflammasome Therapeutics and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

Diabetic Macular Edema Market Trends

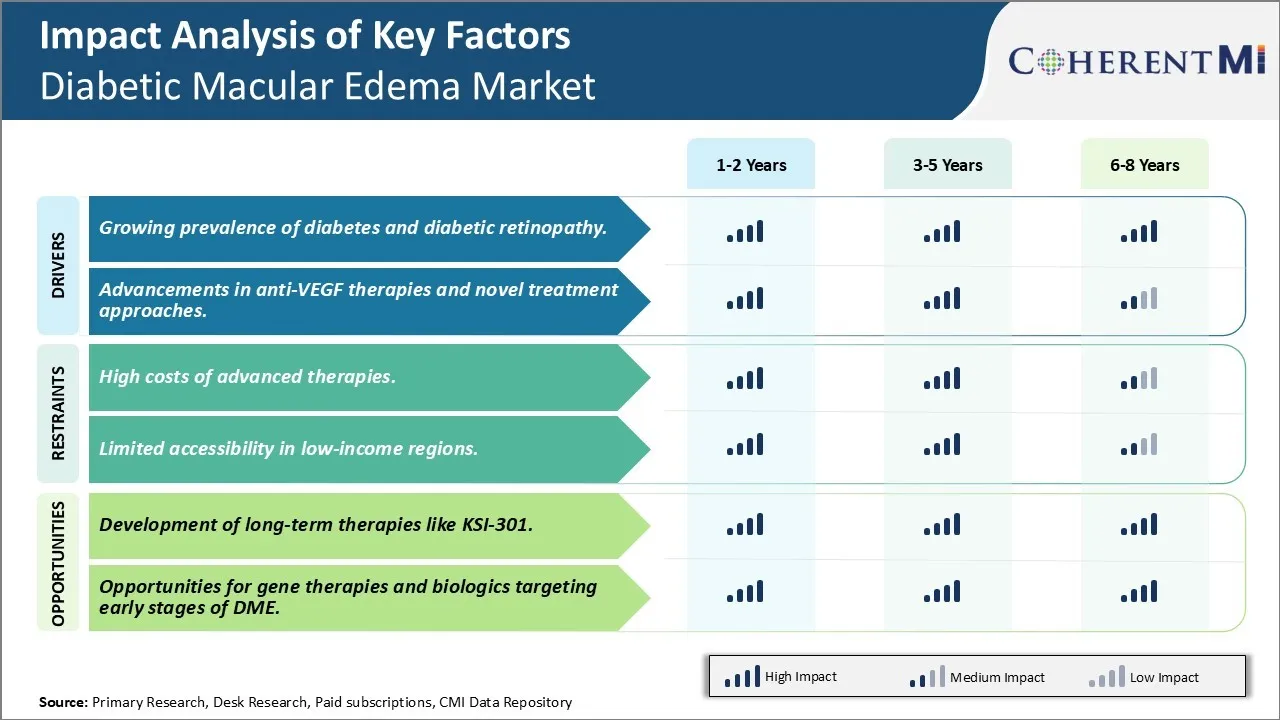

Market Driver - Growing Prevalence of Diabetes and Diabetic Retinopathy Drives the Need for Novel Treatment.

As the prevalence of diabetes continues to grow unabated across the world, so too does the burden of diabetic retinopathy. According to estimates from the International Diabetes Federation, approximately 463 million adults were living with diabetes in 2019 worldwide, and this number is expected to rise to over 700 million by 2045. The alarming increase in the diabetes population is the growing epidemic of obesity and physical inactivity are significant risk factors for the development of type 2 diabetes. Unfortunately, diabetic retinopathy often manifests as a complication of poorly controlled diabetes, with nearly all patients with type 1 diabetes and over 60% of those with type 2 diabetes expected to develop some form of the eye disease over their lifetime.

Diabetic retinopathy occurs when high blood glucose levels damage the tiny blood vessels inside the light-sensitive tissue (retina) at the back of the eye over a period of time. The disease can progress from mild non-proliferative retinopathy involving only microaneurysms and hemorrhages to more advanced proliferative stages marked by the growth of new abnormal blood vessels which can rapidly lead to severe vision loss or blindness if left untreated. It is estimated that approximately one-third of diabetics already have some form of retinopathy at the time of diagnosis of their diabetes. Furthermore, the risk and severity of retinopathy is directly linked to how long a person has had diabetes and the levels of control over their blood glucose, blood pressure, and cholesterol.

As such, the rising tide of diabetes ensures a steady population susceptible to developing diabetic eye diseases such as diabetic macular edema (DME). DME occurs when the retinal blood vessels leak fluid and lipids into the macula - the sensitive central area of the light-sensitive tissue at the back of the eye responsible for sharp, straight-ahead vision. This swelling can distort vision and eventually cause blindness if not urgently treated. Given the overwhelming evidence that diabetic retinopathy and DME risk increases progressively with duration of poorly controlled diabetes, the continued growth in the global diabetes epidemic presents an alarming driver that can fuel the expansion of the diabetic macular edema therapeutics market in the years to come.

Market Driver- Advancements in anti-VEGF Therapies and Novel Treatment Approaches.

Significant progress has been made in recent decades towards developing more effective treatment options for diabetic macular edema. Currently, the standard of care involves the use of intraocular injections of anti-VEGF drugs that inhibit vascular endothelial growth factor - a protein that promotes endothelial cell proliferation and vascular permeability. By blocking VEGF, anti-VEGF therapies help reduce fluid leakage and lessen edema in DME patients. Notably, drugs such as ranibizumab and aflibercept have revolutionized DME treatment since their approval, providing marked vision improvements for many patients.

However, anti-VEGF therapies still have limitations such as the need for frequent eye injections and incomplete response in some individuals. This has intensified research efforts into alternate pharmacological approaches and novel drug delivery technologies. Some promising new strategies under investigation include sustained-release drug delivery systems aimed at extending dosing intervals, corticosteroid therapies targeting different pathways, and molecularly targeted therapies designed to block key mediators of vascular permeability besides VEGF. In the pipeline are also gene therapies employing gene silencing techniques, as well as stem cell therapies employing differentiated retinal pigment epithelial cells.

Forward-thinking pharmaceutical companies have rapidly advanced multiple candidates through clinical trials in pursuit of safer, simpler, and more effective DME therapies. This robust R&D activity reflects the urgent clinical needs as well as commercial opportunities in the expanding DME market. Successful approvals of superior therapies with enhanced safety, efficacy and convenience profiles have the potential to readily displace older anti-VEGF drugs and even expand the addressable patient population.

Market Challenge - High Costs of Advanced Therapies Limits the Market Growth.

One of the major challenges faced in the diabetic macular edema market is the high costs of advanced therapy options. Newer treatment options like intravitreal injections of anti-VEGF drugs have significantly improved visual outcomes for patients compared to older laser photocoagulation therapies. However, these biologic drugs that block vascular endothelial growth factor are also very expensive, with average annual treatment costs estimated to be over USD10,000 per patient. The high drug costs and need for frequent office visits place a heavy financial burden both on patients as well as third-party payers. While these advanced therapies may seem cost-effective from a health outcomes perspective, their pricing remains a barrier for broader adoption and access. Unless alternatives are developed that deliver comparable efficacy but at lower price points, a sizeable portion of those affected by diabetic macular edema may not be able to access or afford regular treatment.

Market Opportunity: Development of long-term therapies like KSI-301.

One promising area of opportunity in the diabetic macular edema market is the development of novel long-acting therapies that can potentially reduce treatment burden. KSI-301, an investigational drug being developed by Kodiak Sciences, represents a potential breakthrough in this regard. If approved, KSI-301 will offer the first long-duration treatment option, with the ability to remain active in the eye for multiple months with just one or two annual injections. This has the potential to significantly improve patient compliance and experience by reducing the need for frequent office visits that currently plague anti-VEGF drugs. From the perspective of the healthcare system and payers as well, long-acting therapies like KSI-301 that allow fewer number of administrations can lower overall costs of care. Their pricing is also expected to be more affordable in comparison to existing drugs. With a favorable safety profile demonstrated so far in clinical trials, KSI-301 has the capability to transform treatment landscape for diabetic macular edema worldwide.

Prescribers preferences of Diabetic Macular Edema Market

Diabetic Macular Edema (DME) treatment follows a step-wise approach based on the severity of edema. Initial mild cases are often treated with anti-VEGF agents that target Vascular Endothelial Growth Factor, a protein linked to increased permeability of blood vessels in the eye. Common anti-VEGF medications used are Lucentis (ranibizumab) and Eylea (aflibercept), administered via intravitreal injections monthly until resolution is achieved, then as needed based on retreat criteria.

For more severe DME, corticosteroids may be prescribed rather than anti-VEGFs as the initial line of treatment. Intravitreal implants such as Ozurdex (dexamethasone) provide sustained drug release over months and reduce injection frequency compared to periocular steroids. However, cataract formation is a potential risk with Ozurdex.

When DME becomes refractory to anti-VEGF monotherapy or corticosteroids, combination therapy may be attempted by prescribing anti-VEGF agents along with corticosteroid implants. This dual approach aims to reduce edema rapidly with steroids while preventing future recurrences through continued VEGF blockade by anti-VEGF drugs.

Other factors influencing prescribers include drug safety, route of administration, retreatment flexibility, and cost effectiveness. Individual patient factors such as risk of complications and adherence also play a role in regimen selection. Close monitoring is needed to assess treatment response at each stage to inform next steps.

Treatment Option Analysis of Diabetic Macular Edema Market

Diabetic Macular Edema (DME) has four stages - mild, moderate, severe, and proliferative. In mild DME, anti-VEGF injections like Eylea or Lucentis are first-line options. These drugs inhibit Vascular Endothelial Growth Factor, reducing fluid buildup and swelling.

As DME progresses to moderate levels, patients may first try these anti-VEGF injections, typically receiving one every 4-6 weeks until vision stabilizes. Steroids like Ozurdex or Iluvien may also be used. As biodegradable intravitreal implants, they slowly release medication over months, reducing treatment burden.

For severe DME, anti-VEGFs remain the standard due to demonstrated long-term vision benefits. However, some patients require additional therapy and may undergo a focal/grid laser procedure. This selectively targets leaking macular regions, helping stabilize vision.

The most advanced stage is proliferative or neovascular DME. Patients develop new, abnormal blood vessels which leak protein/fluid. Combined therapy is preferred - intravitreal anti-VEGF injections along with laser or steroid treatments to reduce vessel growth.

Overall, anti-VEGF drugs are favored across DME stages given strong efficacy and safety data. Steroids provide an alternative for select cases by requiring less frequent dosing. Laser remains invaluable for advanced DME stages by complementing medication and slowing disease progression when used together.

Key winning strategies adopted by key players of Diabetic Macular Edema Market

Expansion of Indications: Gainung additional approved indications allows companies to target a broader patient population. For example, in 2015 Roche gained an expanded approval for Lucentis to treat DME. This helped Lucentis, which was already approved for wet age-related macular degeneration, expand its addressable market for DME treatment.

Aggressive Marketing Campaigns: Pharmaceutical companies invest heavily in promoting awareness of new treatment options among retina specialists. For instance, Regeneron spent over USD 500 million in 2015 alone on promotional activities for Eylea. Such efforts educated doctors about clinical trial results and helped establish Eylea as a premier first-line therapy for DME.

Partnerships and Licensing Deals: Companies partner to leverage each other's expertise and resources. For example, in 2015 Bayer signed a deal giving it rights to market Eylea outside the U.S., while Regeneron retained commercialization in its home market. This partnership boosted Eylea's global commercial presence.

Strategic Acquisitions: Acquiring complementary assets and technologies allows for horizontal integration. For example, Allergan acquired Recipharm in 2018 for USD753 million to expand its manufacturing capacity for producing biosimilars and treatments for retinal diseases like DME.

This analysis highlights real-world examples of strategies that helped lead players like Regeneron, Roche and Allergan grow their market share and better compete in the highly lucrative market.

Segmental Analysis of Diabetic Macular Edema Market

Insights, By Drug Type, Rising Eye Health Awareness Boosts Ranibizumab Adoption.

By Drug Type, Ranibizumab contributes the highest share 45.4% in 2025 owing to its widespread adoption among doctors and patients. Ranibizumab was one of the earliest drugs developed specifically for treating diabetic macular edema. As a monotherapy treatment administered through intravitreal injections, Ranibizumab provides a simple and targeted approach for managing fluid buildup in the retina.

Ranibizumab's differentiation from existing corticosteroid and laser therapies helped raise awareness of diabetic macular edema as a vision-threatening condition. Promotional activities by the drug manufacturer educating physicians and the public about the importance of timely treatment have been highly successful. As eye health has moved up the priority list for those living with diabetes, more patients are proactively seeking out therapy options like Ranibizumab before their vision deteriorates significantly.

Positive clinical evidence also supports Ranibizumab's popularity. Numerous long-term studies have consistently proven its efficacy in improving visual acuity when administered according to the prescribed monthly dosing protocol. Doctors feel confident recommending Ranibizumab knowing it can restore vision that may otherwise be permanently lost. This reassurance gives patients peace of mind that they are benefiting from an established therapy. Ranibizumab's first-mover advantage and strong branding as a dedicated anti-VEGF treatment have made it the standard of care for many eye specialists.

Insights, By Form, Convenience Drives Preference for Intravitreal Injections.

By Form, Intravitreal Injections contribute the highest share 55.7% in 2025. The Non-invasive nature and short treatment duration of intravitreal injections make them highly preferable to alternative forms such as implants.

Intravitreal injections allow drugs to be accurately delivered directly to the back of the eye in a matter of minutes during an office visit. Patients find the convenience of brief monthly visits less disruptive than undergoing surgery or lengthy examinations required for implants. Busy schedules and distance to clinics are fewer barriers as appointments are quick to complete.

Eye doctors also favor intravitreal injections due to their procedural simplicity compared to implants. Specialized surgical skills and long procedure times are not needed. Risks of potential complications from an implant insertion like endophthalmitis are also avoided. This allows injections to be safely administered in any capable clinical setting versus implants usually requiring hospital facilities.

As new anti-VEGF drugs have entered the market, their availability in pre-filled syringes designed specifically for intravitreal delivery enhances ease of administration even further. These formulation advances reinforce injections as the preferred form for delivering prompt treatment to diabetic macular edema patients.

Insights, By Distribution Channel, Established Distribution Channels Drive Hospital Uptake.

In terms of By Distribution Channel, Hospitals are expected to contribute the highest share in 2024 thanks to their accessibility and resources. Hospitals have long been the predominant setting for diabetic eye care management and treatment.

Well-established infrastructure, personnel and equipment in hospital ophthalmology departments allow them to perform the high volume of eye procedures and assessments needed for diabetic macular edema patients. The capabilities to promptly handle intravitreal injections on scheduled treatment days or unforeseen acute cases through emergency services are valuable for managing this chronic condition.

Close working relationships between hospitals and referrals from primary care and diabetes specialists also contribute to the consistent patient volumes they receive. Lower thresholds for specialists to accept new referrals versus private clinics facilitate proper ongoing management. Hospitals are frequently covered by public and private health plans, removing financial barriers to care.

Training of ophthalmologists has traditionally occurred in hospital environments as well. This deepens the expertise and experience base within facilities and leads to preferences among retinal specialists to conduct their practices in association with hospitals. As a result, these distribution channels will remain highly prominent.

Additional Insights of Diabetic Macular Edema Market

The DME market is rapidly evolving with innovative therapies that aim to provide long-term control over vision loss caused by macular swelling. Companies are focusing on novel mechanisms of action to address both the underlying causes of DME and its symptomatic relief. For instance, Kodiak Sciences' KSI-301 represents a significant leap by promising sustained efficacy for up to 6 months, potentially reducing treatment frequency while improving patient outcomes. The development of gene therapies, biologics, and small molecules, as well as efforts to target both the retinal and vascular damage caused by diabetes, represent new frontiers in this field. Collaborations and acquisitions among key players further emphasize the dynamic nature of this market, as they pool resources to overcome existing therapeutic challenges.

Competitive overview of Diabetic Macular Edema Market

The major players operating in the Diabetic Macular Edema Market include Kodiak Sciences, Roche/Genentech, Regeneron Pharmaceuticals, Gene Signal, Inflammasome Therapeutics, Alimera Sciences, Novartis, Bayer, F.Hoffman La-Roche, Genetech, KalVista Pharmaceuticals, Ocugen Inc and Daiichi Sankyo.

Diabetic Macular Edema Market Leaders

Kodiak Sciences

Roche/Genentech

Regeneron Pharmaceuticals

Gene Signal

Inflammasome Therapeutics

*Disclaimer: Major players are listed in no particular order.

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Diabetic Macular Edema Market

In May 2024, Kodiak Sciences announced positive results from Phase III trials for Tarcocimab Tedromer, potentially reducing the frequency of anti-VEGF injections. This development could significantly improve treatment adherence and outcomes for DME patients.

In April 2024, Gene Signal's Phase II trial of Aganirsen demonstrated promising results in reducing corneal neovascularization, providing a new pathway for treating advanced diabetic macular edema.

In March 2024, Inflammasome Therapeutics announced a breakthrough in its early-stage trials for K8, which targets underlying neurodegeneration in DME.

Diabetic Macular Edema Market Report - Table of Contents

. RESEARCH OBJECTIVES AND ASSUMPTIONS

Research Objectives

Assumptions

Abbreviations

MARKET PURVIEW

Report Description

Market Definition and Scope

Executive Summary

Diabetic Macular Edema Market, By Drug Type

Diabetic Macular Edema Market, By Form

Diabetic Macular Edema Market, By Distribution Channel

Coherent Opportunity Map (COM)

MARKET DYNAMICS, REGULATIONS, AND TRENDS ANALYSIS

Market Dynamics

Impact Analysis

Key Highlights

Regulatory Scenario

Product Launches/Approvals

PEST Analysis

PORTER’s Analysis

Merger and Acquisition Scenario

Global Diabetic Macular Edema Market, By Drug Type, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Ranibizumab

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Aflibercept

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Dexamethasone

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Diabetic Macular Edema Market, By Form, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Intravitreal Injections

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Intravitreal Implants

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Diabetic Macular Edema Market, By Distribution Channel, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Hospitals

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Specialty Clinics

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Pharmacies

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Diabetic Macular Edema Market, By Region, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Drug Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Form, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Distribution Channel, 2020-2032, Value (USD Bn)

U.S.

Canada

Latin America

Introduction

Market Size and Forecast, By Drug Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Form, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Distribution Channel, 2020-2032, Value (USD Bn)

Brazil

Argentina

Mexico

Rest of Latin America

Europe

Introduction

Market Size and Forecast, By Drug Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Form, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Distribution Channel, 2020-2032, Value (USD Bn)

Germany

U.K.

Spain

France

Italy

Russia

Rest of Europe

Asia Pacific

Introduction

Market Size and Forecast, By Drug Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Form, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Distribution Channel, 2020-2032, Value (USD Bn)

China

India

Japan

Australia

South Korea

ASEAN

Rest of Asia Pacific

Middle East

Introduction

Market Size and Forecast, By Drug Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Form, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Distribution Channel, 2020-2032, Value (USD Bn)

GCC Countries

Israel

Rest of Middle East

Africa

Introduction

Market Size and Forecast, By Drug Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Form, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Distribution Channel, 2020-2032, Value (USD Bn)

South Africa

North Africa

Central Africa

COMPETITIVE LANDSCAPE

Kodiak Sciences

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Roche/Genentech

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Regeneron Pharmaceuticals

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Gene Signal

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Inflammasome Therapeutics

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Alimera Sciences

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Novartis

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Bayer

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

F.Hoffman La-Roche

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Genetech

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

KalVista Pharmaceuticals

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Ocugen Inc

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Daiichi Sankyo

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analyst Recommendations

Wheel of Fortune

Analyst View

Coherent Opportunity Map

References and Research Methodology

References

Research Methodology

About us

Diabetic Macular Edema Market Segmentation

By Drug Type

Ranibizumab

Aflibercept

Dexamethasone

By Form

Intravitreal Injections

Intravitreal Implants

By Distribution Channel

Hospitals

Specialty Clinics

Pharmacies

Would you like to explore the option of buying individual sections of this report?

About author

Vipul Patil is a dynamic management consultant with 6 years of dedicated experience in the pharmaceutical industry. Known for his analytical acumen and strategic insight, Vipul has successfully partnered with pharmaceutical companies to enhance operational efficiency, cross broader expansion, and navigate the complexities of distribution in markets with high revenue potential.

Frequently Asked Questions :

How Big is the Diabetic Macular Edema Market?

The Global Diabetic Macular Edema Market is estimated to be valued at USD 4.39 Billion in 2025 and is expected to reach USD 5.93 Billion by 2032.

What will be the CAGR of the Diabetic Macular Edema Market?

The CAGR of the Diabetic Macular Edema Market is projected to be 4.23% from 2024 to 2031.

What are the major factors driving the Diabetic Macular Edema Market growth?

The growing prevalence of diabetes and diabetic retinopathy. and advancements in Anti-VEGF therapies and novel treatment approaches are the major factor driving the Diabetic Macular Edema Market.

What are the key factors hampering the growth of the Diabetic Macular Edema Market?

The high costs of advanced therapies. and limited accessibility in low-income regions are the major factor hampering the growth of the Diabetic Macular Edema Market.

Which is the leading Drug Type in the Diabetic Macular Edema Market?

The leading Drug Type segment is Ranibizumab.

Which are the major players operating in the Diabetic Macular Edema Market?

Kodiak Sciences, Roche/Genentech, Regeneron Pharmaceuticals, Gene Signal, Inflammasome Therapeutics, Alimera Sciences, Novartis, Bayer, F.Hoffman La-Roche, Genetech, KalVista Pharmaceuticals, Ocugen Inc, Daiichi Sankyo are the major players.

Missing comfort of reading report in your local language? Find your preferred language :

Insights, By Drug Type, Rising Eye Health Awareness Boosts Ranibizumab Adoption.

Insights, By Drug Type, Rising Eye Health Awareness Boosts Ranibizumab Adoption.