Global ADC Contract Manufacturing Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Global ADC Contract Manufacturing Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Global ADC Contract Manufacturing Market is segmented By Stage of Development(Phase I, Phase II, Phase III), By Process Component(Antibody, HPAPI / Cytotoxic Payload, Conjugation / Linker, Fill / Finish), By Target Indication (Solid Tumors, Hematological Tumors, Others), By Antibody Generation(Second Generation, Third Generation, Fourth Generation, Next Generation), By Antibody Origin (Humanized, Chimeric, Murine, Others), By Type of Linker (Maleimide, SMCC, Tetrapeptide-based linker, Valine-citrulline, Others), By End User (Pharmaceutical Companies, Biotechnology Companies - 30%, Academic & Research Institutes, Others), By Geography (North America, Latin America, Europe, Asia Pacific, Middle East & Africa). The report offers the value (in USD Billion) for the above-mentioned segments.

Global ADC Contract Manufacturing Market is segmented By Stage of Development(Phase I, Phase II, Pha...

Global ADC Contract Manufacturing Market Size - Analysis

The Global ADC Contract Manufacturing Market is estimated to be valued at USD 2.08 Billion in 2025 and is expected to reach USD 5.02 Billion by 2032, growing at a compound annual growth rate (CAGR) of 13.4% from 2025 to 2032. Several factors are contributing to the growth of this market such as rising demand for ADC for cancer treatment, increasing R&D investment for the development of novel ADC, and growing collaboration between pharmaceutical companies and contract manufacturing organizations.

The market trend in the Global ADC Contract Manufacturing industry suggests lucrative opportunities for contract manufacturing organizations to capitalize on. As big pharmaceutical companies continue outsourcing their ADC manufacturing needs, CMOs with requisite expertise, infrastructure and capabilities stand to benefit immensely. Additionally, as newer ADC molecules gain regulatory approvals, the demand for extensive manufacturing capabilities is poised to drive partnerships between drug developers and CMOs.

Market Size in USD Bn

CAGR13.4%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

13.4%

Market Concentration

High

Major Players

AbbVie Contract Manufacturing, Abzena, CARBOGEN AMCIS, Catalent Pharma Solutions, Cerbios-Pharma and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

Global ADC Contract Manufacturing Market Trends

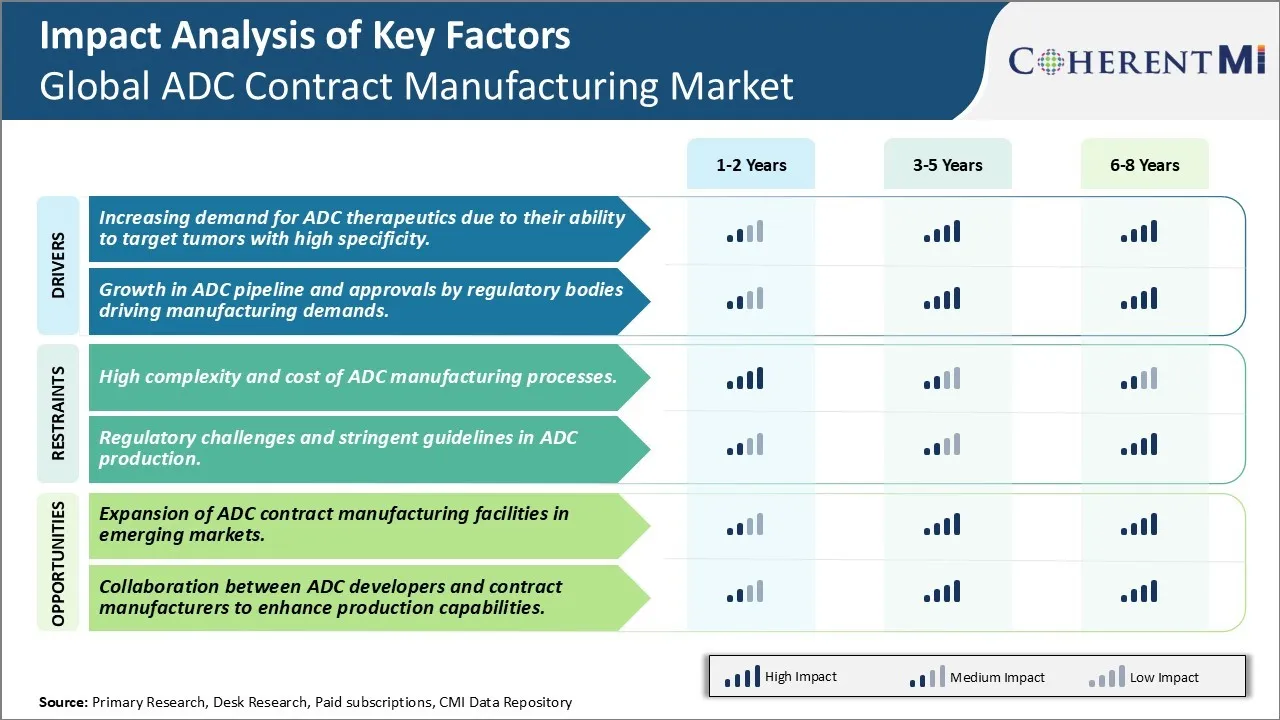

Market Driver - Increasing demand for ADC therapeutics due to their ability to target tumors with high specificity

The rise of antibody drug conjugates has been a key breakthrough in oncology. ADCs work by combining monoclonal antibodies with highly potent anti-cancer payloads through chemical linkers. This allows them to deliver cytotoxic molecules directly and selectively to cancer cells, thereby improving treatment outcomes for patients. The antibody component of ADCs acts as a targeting agent by binding to specific antigens expressed on the surface of tumor cells. The linker then releases the drug payload inside the cancer cell, minimizing toxic effects on healthy tissues. This targeted delivery enables ADCs to kill tumor cells with specificity and precision, leading to strong clinical benefits.

Many new ADCs under development incorporate potent drugs like auristatins and maytansinoids that are up to a thousand times more cytotoxic than conventional chemotherapies. Clinical trials have shown that these ADC payloads can eradicate even treatment-resistant cancer types. As oncologists continue optimizing the antigen-targeting antibodies and drug-linker combinations in ADCs, their therapeutic efficacy is increasing. Several ADC drugs have been commercialized for cancers like breast and blood disorders in recent years. Current therapies like Kadcyla and Adcetris have substantially improved outcomes for patients with limited treatment options. As more positive data emerges from clinical trials, the acceptance and demand for ADCs as a class of targeted biologics is growing rapidly in the pharmaceutical industry and medical community.

Growth in ADC pipeline and approvals by regulatory bodies driving manufacturing demands

There has been a dramatic expansion in the number of antibody-drug conjugates in clinical trials over the past decade. Currently, there are almost 50 ADCs in late-stage or registration studies targeting a wide variety of cancers. Many biopharma corporations and research institutes recognize the revenue potential of these high-value oncology biologics. considerable resources are being invested into developing promising new ADC candidates and scaling up early programs. Most major players in the biotech arena now have internal ADC programs or strategic partnerships focused on these agents.

Regulatory bodies are also exhibiting greater openness towards approving ADCs based on early phase trial results and less restrictive targets. In recent years, the FDA and EMA have granted accelerated review and priority reviews to several ADCs. Streamlined pathways are encouraging increased funding into pivotal studies and commercial-scale manufacturing activities. Once an ADC gains approval, pharmaceutical sponsors want to maximize revenue by rapidly making their treatment available to markets worldwide. This drives tremendous demand for specialist contract manufacturing organizations with expertise across the complex production and analytical testing requirements of ADC therapeutics. Growing regulatory confidence in the class combined with heightening pressures to commercialize pipelines is significantly boosting needs for large-scale ADC manufacturing capacities.

Market Challenge - High complexity and cost of ADC manufacturing processes

The development and manufacturing of antibody-drug conjugates (ADCs) poses significant challenges to pharmaceutical companies due to the highly complex nature of ADC production. The process involves the chemical attachment of cytotoxic molecules to monoclonal antibodies, which must be done with great precision to ensure the drug is properly attached without compromising the function and targeting ability of the antibody. Achieving consistent and reliable conjugation is difficult and requires extensive research and engineering. Any small change or lack of control during the conjugation reaction can lead to batch-to-batch variability and product failure. Additionally, due to the sensitive nature of ADCs, manufacturers must implement rigorous quality control and ensure sterility throughout the entire production process. meeting regulatory requirements increases costs substantially. The multiple complex manufacturing steps and stringent quality standards have resulted in ADC production being much costlier than traditional drug development routes. This high cost can be a barrier for pharmaceutical companies and reduce the commercial viability of some ADC programs.

Market Opportunity - Expansion of ADC contract manufacturing facilities in emerging markets

The rapidly developing biotechnology industry in emerging markets presents a significant opportunity for the growth of antibody-drug conjugate contract manufacturing. Countries such as China, India, and South Korea have made large investments in biomanufacturing infrastructure and talent over recent years and now have world-class facilities and capabilities that are on par with top ADC contract manufacturers in traditional markets. With lower operating costs compared to developed regions, these emerging market CDMOs offer a compelling value proposition to pharmaceutical companies looking to produce ADCs in a cost-effective manner. We have already seen leading global CDMOs such as WuXi Biologics establishing extensive ADC capabilities across multiple sites in China and India. As more biopharma companies recognize the benefits of emerging market contract services for this complex modality, we can expect continued expansion of ADC manufacturing capacities among CDMOs in these regions. This will help increase global supply and lower production costs, facilitating increased patient access to promising new ADC therapeutic options.

Key winning strategies adopted by key players of Global ADC Contract Manufacturing Market

Focus on quality and reliability: Leading players like Lonza, Samsung BioLogics and WuXi Biologics have focused heavily on quality and reliability in their manufacturing operations. They have invested in the latest technologies and facilities to ensure adherence to stringent regulatory standards. Their consistent track record of delivering high quality biosimilars and biologics on time has helped win the trust of big biopharma clients.

Expand manufacturing capabilities: To meet the growing demand, many players have expanded their overall manufacturing capacities as well as capabilities over the past 5 years. For instance, in 2017 Lonza doubled its Singapore facility's capacity to support monoclonal antibody production. Similarly, Samsung Biologics invested $2.5 billion to build its new plant in Songdo, South Korea which became operational in 2018. This has allowed them to take on larger and more complex manufacturing deals.

Diversify service offerings: In addition to 'fill and finish' operations, market leaders provide other critical services like analytical development, process development and cell line development under one roof. This 'one-stop-shop' approach saves time and cost for biotech clients. For example, more than 60% of WuXi Biologics' revenue now comes from non-CMC services like toxicology and pharmacokinetics studies.

Form strategic partnerships: Companies focus on forming strategic global partnerships with leading research institutions and biotechs. For instance, in 2019 Samsung Biologics partnered with AstraZeneca's cell and gene therapy arm to supply manufacturing support. These partnerships give access to a steady pipeline of potential new projects.

Geographic expansion: To cater to the growing overseas demand, players have expanded their geographic footprint through new facilities. For example, Lonza establishedsites in the US, Switzerland, Singapore and China between 2015-2018 to serve both local and international clients better.

Segmental Analysis of Global ADC Contract Manufacturing Market

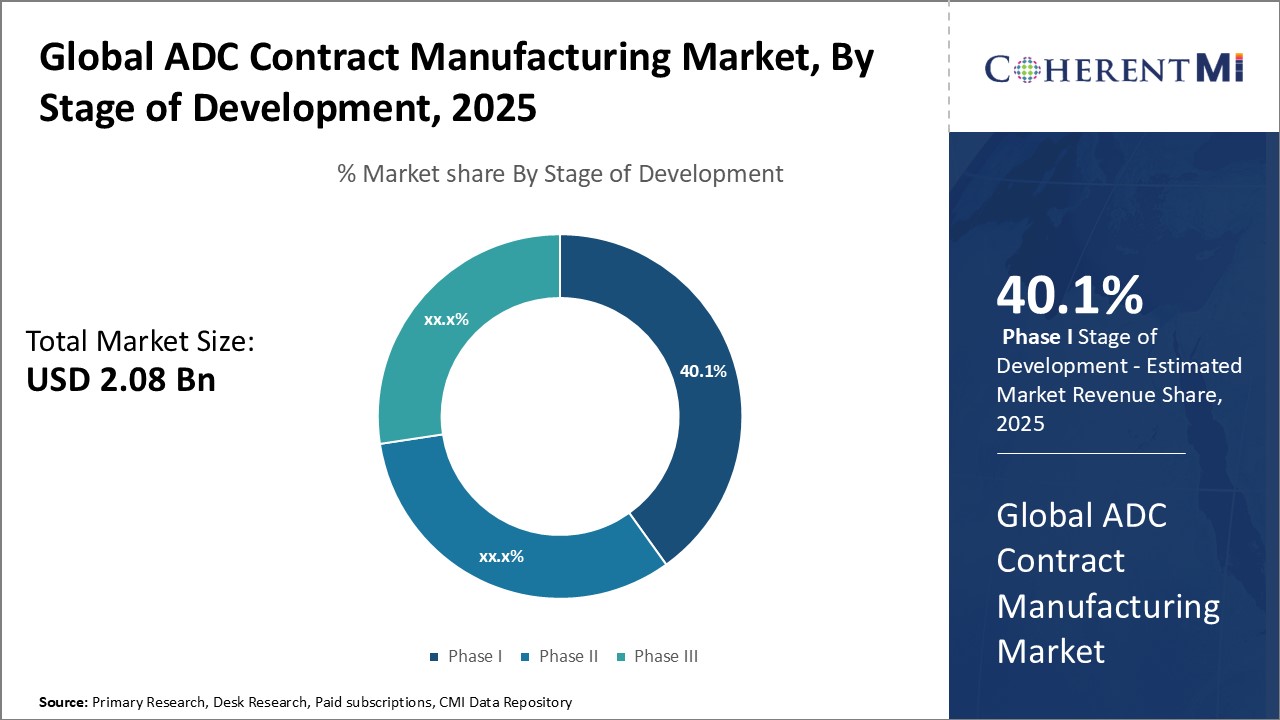

By Stage of Development - Advantages of Early Research Drive Phase I Dominance

In terms of By Stage of Development, Phase I contributes the highest share of the market owing to the inherent advantages in early research. Phase I clinical trials represent the initial testing of an ADC in humans, primarily aimed at evaluating safety and determining safe dosage ranges. At this early stage, there are fewer regulatory hurdles and development costs are relatively low compared to later phases. This allows for faster iteration and extensive testing of different antibody-drug conjugates against the same target without major investment. Additionally, Phase I provides proof-of-concept data on whether an ADC binds to and affects the intended target as expected based on preclinical studies. Obtaining this human validation at an early stage de-risks further development and helps strategic decision making.

Small biotech and academic research centers frequently outsource Phase I trials given limited in-house capabilities and resources for conducting human studies. Larger pharmaceutical companies also often rely on contract manufacturers for Phase I to efficiently explore a wide variety of early-stage candidates before committing significant capital. The modular nature of Phase I trials also lends itself well to the contract development model, allowing companies to rapidly generate preliminary data on multiple ADCs in parallel. Given these advantages, Phase I has emerged as an attractive outsourcing segment that drives significant demand for experienced contract manufacturers able to deliver efficient first-in-human testing.

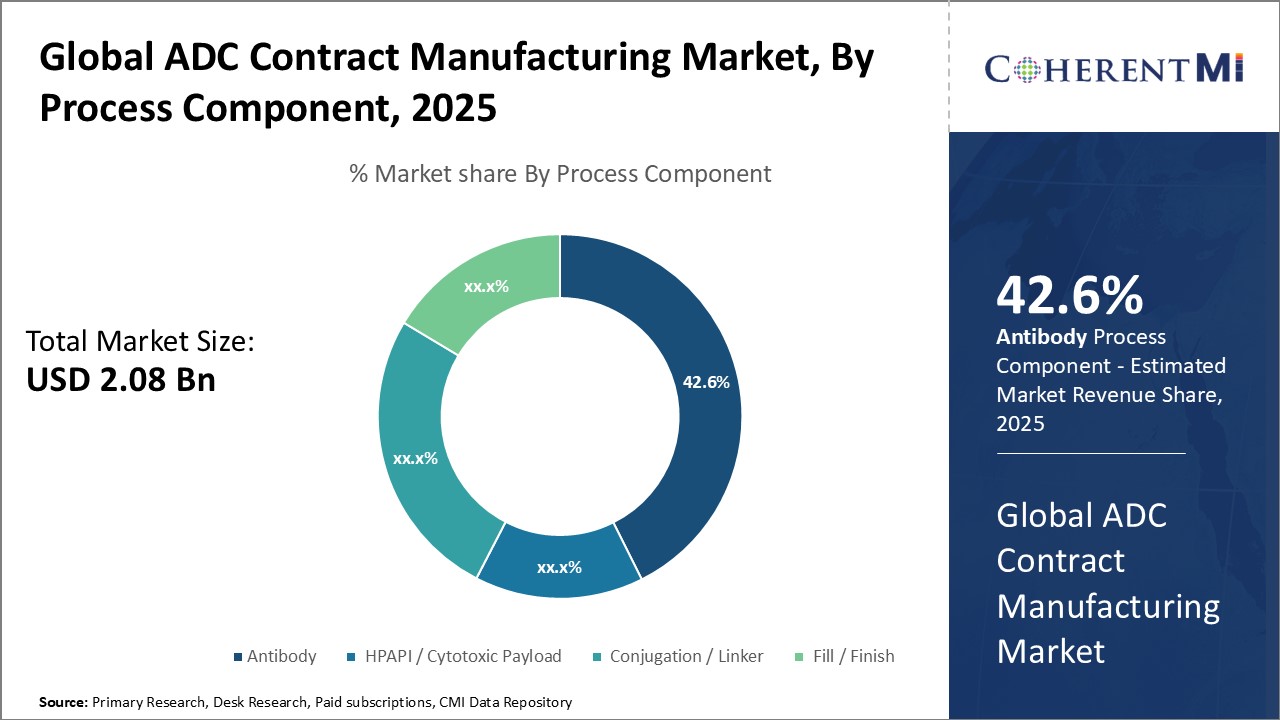

By Process Component - Antibody Complexity Drives Outsourcing

In terms of By Process Component, Antibody contributes the highest share of the market owing to its key role and technical complexity. The antibody is the core targeting element that delivers the cytotoxic drug payload to tumor cells, making its selection, development and manufacturing critical to an ADC's success. However, generating the appropriate antibody with optimal affinity, specificity and drug-loading properties requires extensive protein engineering expertise. Characterization of the antibody also presents analytical challenges given its large size and heterogeneous nature. Additionally, scaling up antibody production from research to commercial levels involves optimization across cell culture, purification and quality control - capabilities well beyond many smaller oncology-focused companies.

Outsourcing antibody development and manufacturing allows businesses to gain access to experienced teams, robust production platforms and advanced quality systems needed for clinical and commercial-scale antibody production. Contract manufacturers have made significant investments developing expertise in cell line development, protein expression and purification particularly suited for ADC antibodies. They also offer flexible, customizable services from antigen design and hybridoma development through manufacturing and stability testing. Given the antibody's importance and technical barriers involved, outsourcing this critical component allows companies to stay focused on their core expertise while minimizing investment and project risk. This drives strong demand for experienced CDMOs specialized in ADC antibodies.

By Target Indication - Difficulties in Solid Tumors Drive Clinical Trials

In terms of By Target Indication, Solid Tumors contribute the highest share of the market owing to ongoing challenges treating these cancers. Solid tumors encompass many common and difficult-to-treat cancers such as breast, lung and pancreatic tumors that together represent a majority of cancer diagnoses. While hematological and other liquid tumors may be addressed through systemic treatment approaches like chemotherapy, solid tumors pose additional barriers to effective drug delivery given their physical structure and protective extracellular matrix. This limits the efficacy of existing treatment paradigms and presents an ongoing need for novel oncology agents like ADCs that can penetrate solid tumors. Additionally, solid tumors are more heterogeneous with subpopulations of cells presenting different drug sensitivities and resistance mechanisms. This complexity contributes to high rates of relapse even following initial response to treatment. ADCs aim to overcome these challenges through targeted delivery of potent payloads specifically to cancer cells. Demonstrating efficacy in solid tumors through clinical trials is a critical hurdle that can validate an entirely new drug class. As a result, expanding clinical research remains a priority as biotechs and pharmaceutical companies work to develop ADCs addressing solid tumor cancers with high unmet need like those of the lung, breast and pancreas. This drives strong demand for experienced CMOs to support numerous clinical studies still needed to establish ADCs for solid tumor indications.

Additional Insights of Global ADC Contract Manufacturing Market

The ADC contract manufacturing market is poised for substantial growth, driven by the increasing demand for antibody drug conjugates (ADCs) which are recognized for their specificity in targeting cancer cells while minimizing off-target effects. The market's expansion is heavily influenced by the complex nature of ADC production, which requires specialized expertise and cutting-edge technology, often leading drug developers to outsource these manufacturing operations. The industry is currently dominated by North American and European manufacturers, with significant investments being made in facility expansions to meet growing demand. As the market evolves, strategic partnerships and acquisitions are expected to play a crucial role in enhancing production capabilities and maintaining competitive advantage. With a forecasted CAGR of 13.2%, the market is expected to reach US$ 1.83 billion by 2024, reflecting its significant growth potential over the next decade.

Competitive overview of Global ADC Contract Manufacturing Market

The major players operating in the Global ADC Contract Manufacturing Market include Formosa Laboratories, GBI, Lonza, MabPlex, MilliporeSigma, Piramal Pharma Solutions, Recipharm AB, Sterling Pharma Solutions, WuXi Biologics, Minakem, Aurigene Pharmaceutical Services, Porton Pharma, PROVEO (Cerbios-Pharma SA), Axplora and Avid Bioservices.

Global ADC Contract Manufacturing Market Leaders

AbbVie Contract Manufacturing

Abzena

CARBOGEN AMCIS

Catalent Pharma Solutions

Cerbios-Pharma

*Disclaimer: Major players are listed in no particular order.

Global ADC Contract Manufacturing Market - Competitive Rivalry

Global ADC Contract Manufacturing Market

Market Consolidated (Dominated by major players)

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Global ADC Contract Manufacturing Market

On February 2024, Samsung Biologics has partnered with LegoChem Biosciences to support their antibody-drug conjugate (ADC) program aimed at treating solid tumors. Samsung Biologics will provide antibody development and drug substance manufacturing services. LegoChem Biosciences plans to submit an Investigational New Drug application to the U.S. FDA in early 2025, with promising non-clinical efficacy results.

In October 2023, Lonza signed a manufacturing agreement to boost ADC production with new bioconjugation suites in Visp, Switzerland.

In September 2023, WuXi Biologics collaborated with Mabwell Therapeutics to expedite ADC research and commercialization.

On May 2024, AstraZeneca plans to build a US$1.5 billion manufacturing facility in Singapore for antibody drug conjugates (ADCs), set to be operational by 2029. This will be AstraZeneca's first facility to cover the entire ADC manufacturing process, enhancing its global supply of these next-generation cancer treatments. The project is supported by the Singapore Economic Development Board.

Global ADC Contract Manufacturing Market Report - Table of Contents

RESEARCH OBJECTIVES AND ASSUMPTIONS

Research Objectives

Assumptions

Abbreviations

MARKET PURVIEW

Report Description

Market Definition and Scope

Executive Summary

Global ADC Contract Manufacturing Market, By Stage of Development

Global ADC Contract Manufacturing Market, By Process Component

Global ADC Contract Manufacturing Market, By Target Indication

Global ADC Contract Manufacturing Market, By Antibody Generation

Global ADC Contract Manufacturing Market, By Antibody Origin

Global ADC Contract Manufacturing Market, By Type of Linker

Global ADC Contract Manufacturing Market, By End User

Coherent Opportunity Map (COM)

MARKET DYNAMICS, REGULATIONS, AND TRENDS ANALYSIS

Market Dynamics

Impact Analysis

Key Highlights

Regulatory Scenario

Product Launches/Approvals

PEST Analysis

PORTER’s Analysis

Merger and Acquisition Scenario

Global ADC Contract Manufacturing Market, By Stage of Development, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Phase I

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Phase II

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Phase III

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global ADC Contract Manufacturing Market, By Process Component, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Antibody

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

HPAPI / Cytotoxic Payload

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Conjugation / Linker

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Fill / Finish

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global ADC Contract Manufacturing Market, By Target Indication, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Solid Tumors

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Hematological Tumors

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Others

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global ADC Contract Manufacturing Market, By Antibody Generation, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Second Generation

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Third Generation

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Fourth Generation

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Next Generation

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global ADC Contract Manufacturing Market, By Antibody Origin, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Humanized

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Chimeric

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Murine

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Others

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global ADC Contract Manufacturing Market, By Type of Linker, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Maleimide

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

SMCC

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Tetrapeptide-based linker

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Valine-citrulline

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Others

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global ADC Contract Manufacturing Market, By End User, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Pharmaceutical Companies

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Biotechnology Companies - 30%

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Academic & Research Institutes

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Others

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global ADC Contract Manufacturing Market, By Region, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Process Component , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Target Indication , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Generation , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Origin , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Type of Linker , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End User , 2020-2032, Value (USD Bn)

U.S.

Canada

Latin America

Introduction

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Process Component , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Target Indication , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Generation , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Origin , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Type of Linker , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End User , 2020-2032, Value (USD Bn)

Brazil

Argentina

Mexico

Rest of Latin America

Europe

Introduction

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Process Component , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Target Indication , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Generation , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Origin , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Type of Linker , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End User , 2020-2032, Value (USD Bn)

Germany

U.K.

Spain

France

Italy

Russia

Rest of Europe

Asia Pacific

Introduction

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Process Component , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Target Indication , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Generation , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Origin , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Type of Linker , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End User , 2020-2032, Value (USD Bn)

China

India

Japan

Australia

South Korea

ASEAN

Rest of Asia Pacific

Middle East

Introduction

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Process Component , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Target Indication , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Generation , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Origin , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Type of Linker , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End User , 2020-2032, Value (USD Bn)

GCC Countries

Israel

Rest of Middle East

Africa

Introduction

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Process Component , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Target Indication , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Generation , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Antibody Origin , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Type of Linker , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End User , 2020-2032, Value (USD Bn)

South Africa

North Africa

Central Africa

COMPETITIVE LANDSCAPE

Formosa Laboratories

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

GBI

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Lonza

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

MabPlex

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

MilliporeSigma

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Piramal Pharma Solutions

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Recipharm AB

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Sterling Pharma Solutions

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

WuXi Biologics

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Minakem

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Aurigene Pharmaceutical Services

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Porton Pharma

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

PROVEO (Cerbios-Pharma SA)

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Axplora

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Avid Bioservices

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analyst Recommendations

Wheel of Fortune

Analyst View

Coherent Opportunity Map

References and Research Methodology

References

Research Methodology

About us

Global ADC Contract Manufacturing Market Segmentation

By Stage of Development

Phase I

Phase II

Phase III

By Process Component

Antibody

HPAPI / Cytotoxic Payload

Conjugation / Linker

Fill / Finish

By Target Indication

Solid Tumors

Hematological Tumors

Others

By Antibody Generation

Second Generation

Third Generation

Fourth Generation

Next Generation

By Antibody Origin

Humanized

Chimeric

Murine

Others

By Type of Linker

Maleimide

SMCC

Tetrapeptide-based linker

Valine-citrulline

Others

By End User

Pharmaceutical Companies

Biotechnology Companies - 30%

Academic & Research Institutes

Others

Would you like to explore the option of buying individual sections of this report?

About author

Ghanshyam Shrivastava - With over 20 years of experience in the management consulting and research, Ghanshyam Shrivastava serves as a Principal Consultant, bringing extensive expertise in biologics and biosimilars. His primary expertise lies in areas such as market entry and expansion strategy, competitive intelligence, and strategic transformation across diversified portfolio of various drugs used for different therapeutic category and APIs. He excels at identifying key challenges faced by clients and providing robust solutions to enhance their strategic decision-making capabilities. His comprehensive understanding of the market ensures valuable contributions to research reports and business decisions.

Ghanshyam is a sought-after speaker at industry conferences and contributes to various publications on pharma industry.

Frequently Asked Questions :

How big is the Global ADC Contract Manufacturing Market?

The Global ADC Contract Manufacturing Market is estimated to be valued at USD 2.08 in 2025 and is expected to reach USD 5.02 Billion by 2032.

What are the major factors driving the Global ADC Contract Manufacturing Market growth?

The increasing demand for adc therapeutics due to their ability to target tumors with high specificity. and growth in adc pipeline and approvals by regulatory bodies driving manufacturing demands. are the major factor driving the Global ADC Contract Manufacturing Market.

Which is the leading Stage Of Development in the Global ADC Contract Manufacturing Market?

The leading Stage Of Development segment is Phase III.

Which are the major players operating in the Global ADC Contract Manufacturing Market?

Formosa Laboratories, GBI, Lonza, MabPlex, MilliporeSigma, Piramal Pharma Solutions, Recipharm AB, Sterling Pharma Solutions, WuXi Biologics, Minakem, Aurigene Pharmaceutical Services, Porton Pharma, PROVEO (Cerbios-Pharma SA), Axplora, Avid Bioservices are the major players.

What will be the CAGR of the Global ADC Contract Manufacturing Market?

The CAGR of the Global ADC Contract Manufacturing Market is projected to be 13.4% from 2025-2032.

Missing comfort of reading report in your local language? Find your preferred language :

By Stage of Development - Advantages of Early Research Drive Phase I Dominance

By Stage of Development - Advantages of Early Research Drive Phase I Dominance