Global Complement Inhibitors Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Global Complement Inhibitors Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Global Complement Inhibitors Market is Segmented By Stage of Development (Paroxysmal Nocturnal Hemoglobinuria (PNH), Atypical Hemolytic Uremic Syndrome (aHUS) , Age-related Macular Degeneration (AMD), Myasthenia Gravis, Others), By Mechanism of Action (C5 Inhibitors, C3 Inhibitors, Terminal Complement Inhibitors, Others), By Route of Administration (Intravenous (IV), Subcutaneous (SC)), By End-User (Hospitals and Specialty Clinics, Retail Pharmacies , Others), By Geography (North America, Latin America, Asia Pacific, Europe, Middle East, and Africa). The report offers the value (in USD billion) for the above-mentioned segments.

Global Complement Inhibitors Market is Segmented By Stage of Development (Paroxysmal Nocturnal Hemog...

Global Complement Inhibitors Market Size - Analysis

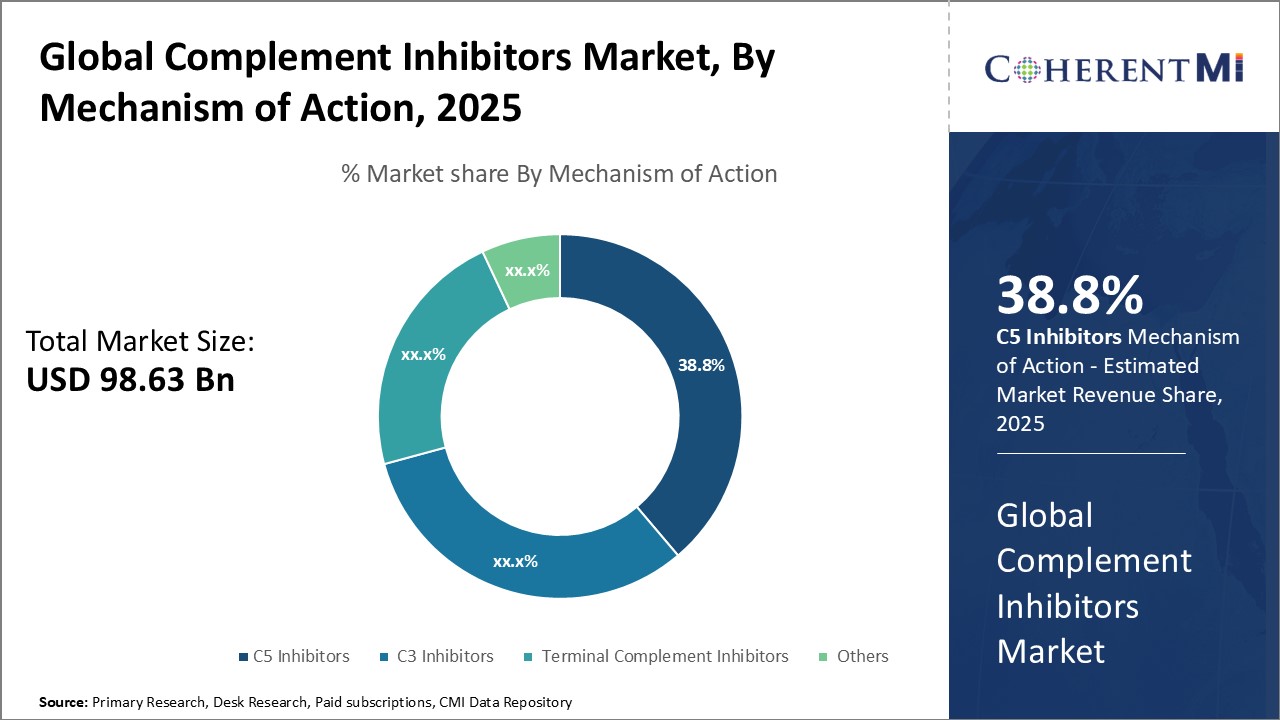

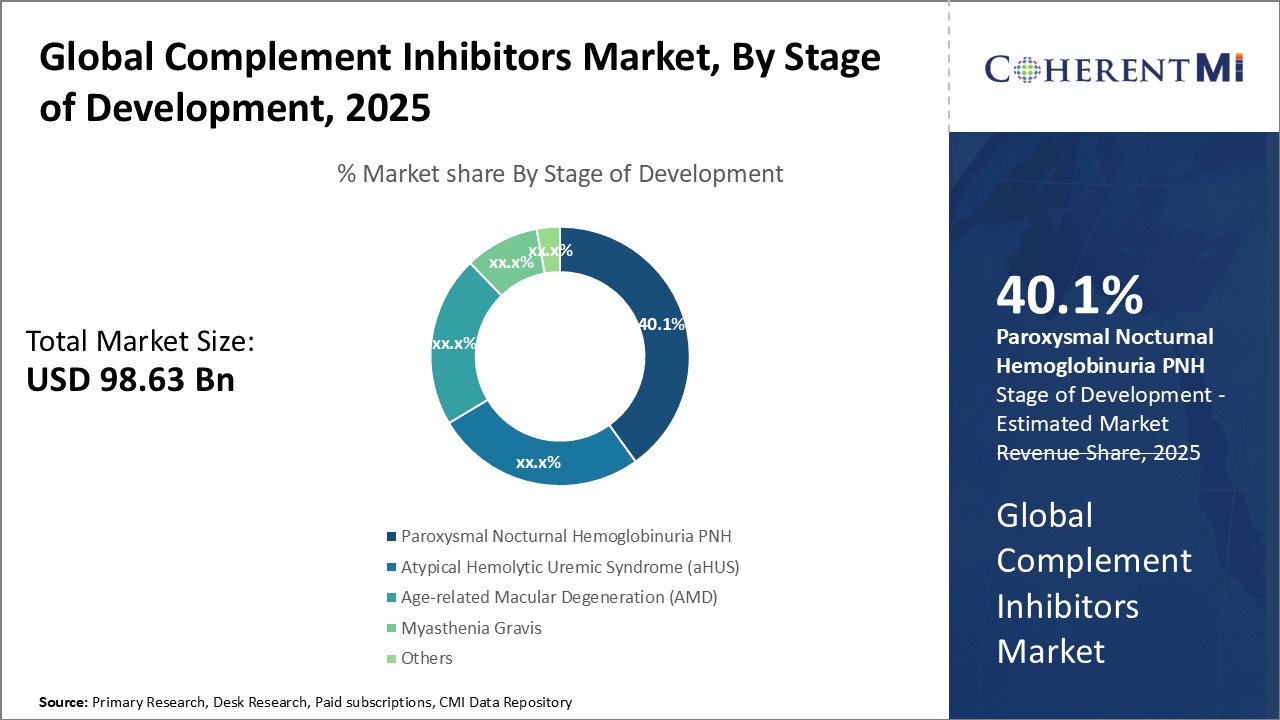

The Global Complement Inhibitors Market is estimated to be valued at USD 98.63 Billion in 2025 and is expected to reach USD 277.07 Billion by 2032, growing at a compound annual growth rate (CAGR) of 15.9% from 2025 to 2032. Complement inhibitors are used for several acute and chronic inflammation conditions driven by complement system dysregulation.

The market is expected to witness a positive growth trend over the forecast period. Rising prevalence of paroxysmal nocturnal hemoglobinuria and atypical hemolytic uremic syndrome indications amenable to treatment with complement inhibitors will drive the demand. Promising results of drugs in the pipeline for expanding approved indications will further support market advances if clinical trials are successful and regulatory approvals are obtained.

Market Size in USD Bn

CAGR15.9%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

15.9%

Market Concentration

High

Major Players

Alexion Pharmaceuticals (AstraZeneca), Apellis Pharmaceuticals, Sanofi, CSL Behring, Takeda Pharmaceuticals and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

Global Complement Inhibitors Market Trends

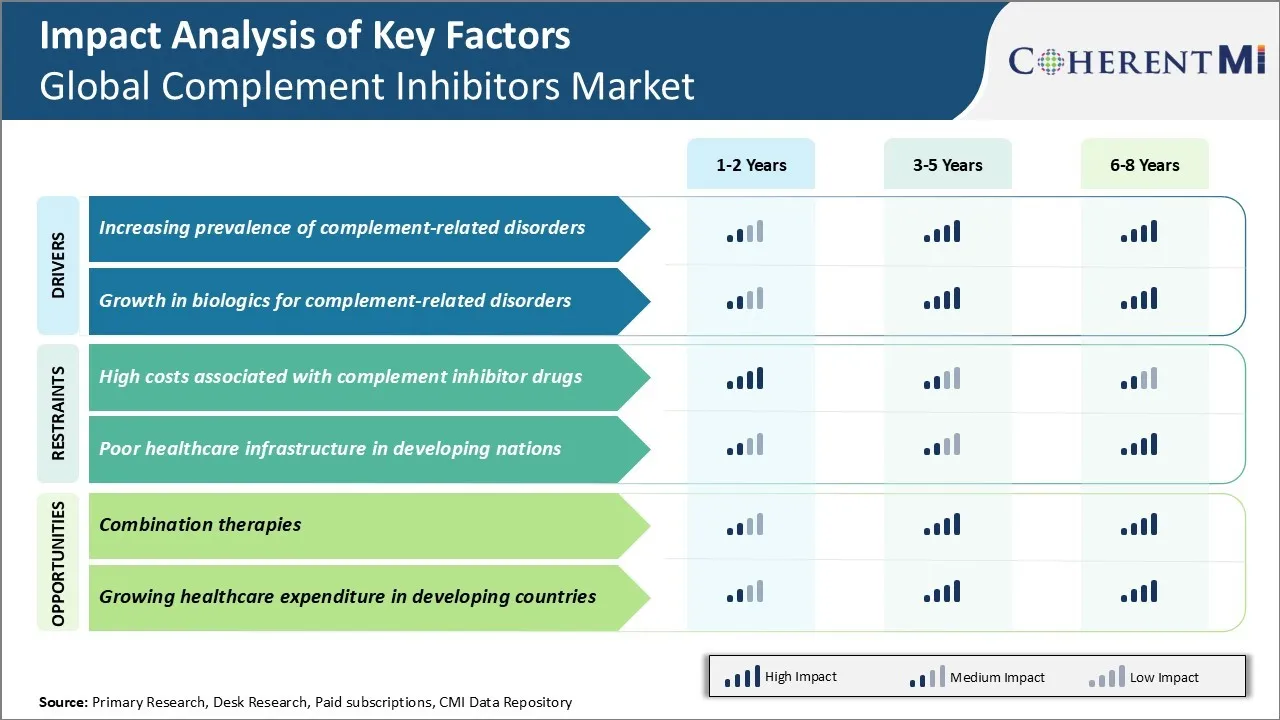

Market Driver - Increasing prevalence of complement-related disorders

The global burden of complement-related disorders has been rising significantly over the past few decades. Complement dysregulation and overactivation play an important role in the pathology of various autoimmune and inflammatory conditions such as atypical hemolytic uremic syndrome (aHUS), paroxysmal nocturnal hemoglobinuria (PNH), myasthenia gravis (MG), and age-related macular degeneration (AMD). Epidemiological studies suggest that the incidence and prevalence of such conditions are increasing worldwide mainly due to aging populations and improved diagnostics. For instance, the prevalence of aHUS in the United States is estimated to be approximately 1-9 cases per million with an incidence rate of 2 new cases per million persons per year. In Europe, the prevalence of PNH is estimated to be between 1-5 cases per million. Rising longevity coupled with growing awareness about rare conditions is expected to further escalate diagnosis rates of complement-related disorders going forward. As these disorders can severely impact quality of life, there exists a strong clinical need for developing targeted treatment approaches to address underlying complement dysregulation. Therefore, the growing patient pool of various complement-related conditions will likely drive robust demand and uptake of emerging complement inhibitors over the coming years.

Growth in biologics for complement-related disorders

The global complement inhibitors market is witnessing positive transformation encouraged by rising R&D investments of leading pharma companies in developing novel biologics. Several new biologic drug candidates that selectively target specific components of the complement cascade are currently at various stages of clinical trials. For instance, Phase 3 trials of eculizumab (Soliris), the first-in-class anti-C5 monoclonal antibody for treating aHUS, have demonstrated strong safety and efficacy data. Likewise, Phase 3 trials of ravulizumab (Ul Tomiris), a long-acting C5 inhibitor, have reportedly met their primary endpoints in aHUS. In addition, several biotechs are evaluating therapeutic antibodies against C3, factor B, C1s and others in early to mid-stage clinical studies for conditions like AMD, rheumatoid arthritis, myocardial infarction etc. If proven safe and effective, these biologics are expected to capture significant market share by address currently unmet needs. Furthermore, the launch of promising new biologics as well as potential approvals of recently investigated assets will increase treatment options for patients and physicians alike. This, along with availability of innovative administration methods like subcutaneous formulations, is expected to positively drive market demand over the forecast period.

Market Challenge - High costs associated with complement inhibitor drugs

One of the major challenges faced by the global complement inhibitors market is the high costs associated with these drugs. Developing novel drugs is an expensive process and complement inhibitors mainly target rare diseases. This increases the overall R&D costs for pharmaceutical companies and results in high drug prices. For instance, the costs of drugs like Soliris (eculizumab) and Ultomiris (ravulizumab) which are used for paroxysmal nocturnal hemoglobinuria can be over $500,000 per patient annually. Due to such high costs, many patients lack access to these life-saving drugs particularly in developing regions. The high costs also put financial pressure on healthcare systems and insurance companies. Pharmaceutical companies need to balance drug development costs and ensure treatment affordability. Governments and organizations are working on policies and programs to increase access but the current drug prices remain unaffordable for many. This challenge of high drug costs can negatively impact market growth if not addressed properly.

Market Opportunity - Combination therapies for market

One significant opportunity for the complement inhibitors market lies in the development of combination therapies. Combining complement inhibitors with other drug classes can enhance therapeutic efficacy and expand the eligible patient population. Research shows that complement dysregulation often co-exists with dysfunctions of other physiological pathways. Targeting multiple pathways simultaneously through combination regimens is scientifically more rational. Ongoing clinical trials are evaluating complement inhibitors in combination with drugs for rheumatoid arthritis, systemic lupus erythematosus, paroxysmal nocturnal hemoglobinuria and other rare diseases. These combination therapies have the potential to achieve superior clinical outcomes compared to monotherapies. Combination regimens also allow drugs to be used at lower doses, reducing safety concerns and drug costs. If successful, combination therapies will help complement inhibitors access newer indications and significantly grow the market size in the coming years. Pharmaceutical companies are making large investments in combination therapy development which can be a major growth driver.

Key winning strategies adopted by key players of Global Complement Inhibitors Market

Leading players like Alexion Pharmaceuticals and Apellis Pharmaceuticals have focused on expanding their product portfolios through acquisitions and strategic collaborations. For instance, in 2021, Alexion acquired Portola Pharmaceuticals for US$1.41 billion to expand its pipeline of complement inhibitors for hematology and nephrology disorders. This acquisition brought Alexion Andexxa, the only FDA-approved factor Xa inhibitor antidote.

Companies are also investing heavily in R&D to develop novel therapies. For example, in 2020 Apellis completed two Phase 3 trials (PEGGASUS and OAKS) evaluating pegcetacoplan for PNH and geographic atrophy, respectively. The successful results led to FDA approval of pegcetacoplan (Empaveli) for PNH in 2021, making it the first targeted C3 therapy. This expanded Apellis' portfolio beyond PNH into other complement-driven diseases.

Adopting a niche market strategy has also proven effective for companies. For example, Achillion Pharmaceuticals focused on developing oral factor D inhibitors for C3 glomerulopathy and other complement-mediated diseases. This helped Achillion become an attractive acquisition target, with Abbott Laboratories acquiring Achillion in 2020 for $930 million.

Companies often pursue geographic expansion opportunities as well. For instance, in 2018 Alexion launched Ultomiris in the EU for adults with PNH after FDA approval in 2019. This helped Alexion establish itself as the leader in PNH treatment and gain a strong foothold in international markets.

In summary, strategic acquisitions and collaborations, increased R&D investments, niche market strategies, and geographic expansion have been some of the key winning formulas adopted by leaders in the global complement inhibitors market to achieve successful growth and market dominance.

Segmental Analysis of Global Complement Inhibitors Market

By Stage of Development - Rising Prevalence and No Approved Treatment

In terms of By Stage of Development, Paroxysmal Nocturnal Hemoglobinuria (PNH) contributes the highest share of the market owing to its rising prevalence globally and lack of approved treatment options. PNH affects both male and female equally and causes destruction of red blood cells. The prevalence of PNH is estimated to be around 1 to 5 cases per million people. With no permanent cure available, lifelong treatments are required to manage the symptoms. Currently approved treatments like eculizumab only control hemolysis but do not cure the disease. This unmet need in the market provides a major growth opportunity for complement inhibitors targeting PNH. Novel therapies in the pipeline can potentially provide complete remission to patients if approved, thereby driving higher adoption and market share for PNH segment.

By Mechanism of Action - Targeted Inhibition Rising as Preferred Mechanism

In terms of By Mechanism of Action, C5 Inhibitors contributes the highest share of the market driven by their targeted inhibition of the complement cascade. C5 Inhibitors block the activation of C5 protein which plays a central role in inflammation and cell lysis. Inhibition of C5 is preferred over blocking upstream components as it prevents the formation of pro-inflammatory factors like C3a and C5a. This makes C5 inhibitors safer with lesser side effects compared to drugs inhibiting C3 or earlier stages. Their selective mechanism allows achieving better efficacy goals with optimized dosing. Higher selectivity and precision make C5 inhibitors the most prescribed class contributing to their expanding market share over other mechanism classes.

By Route of Administration - Growing IV to SC Switch and Self-administration

In terms of By Route of Administration, Intravenous (IV) contributes the highest share currently, though Subcutaneous (SC) segment is growing at a faster rate. The sales of IV segment are growing due to shortage of treatment options and continued use for certain indications. However, for chronic indications, frequent hospital visits for IV administration lower patient adherence. The ease of self-administration with SC routes is increasing preference. Drugs in the pipeline with SC formulations are expected to drive higher switching from IV to SC. This would boost the SC segment by providing independence to patients and doctors while gaining popularity over hospital-controlled IV regimens.

Competitive overview of Global Complement Inhibitors Market

The major players operating in the Global Complement Inhibitors Market include Regeneron Pharmaceuticals, Pharming Group, BioCryst Pharmaceuticals, Amgen, Omeros Corporation, Ionis Pharmaceuticals, Genentech (Roche), Novartis, Hoffmann-La Roche, Eisai Co., Ltd., Akari Therapeutics, Care Pharma, NovelMed Therapeutics, Zymeworks Inc. and Daiichi Sankyo.

Global Complement Inhibitors Market Leaders

Alexion Pharmaceuticals (AstraZeneca)

Apellis Pharmaceuticals

Sanofi

CSL Behring

Takeda Pharmaceuticals

*Disclaimer: Major players are listed in no particular order.

Global Complement Inhibitors Market - Competitive Rivalry

Global Complement Inhibitors Market

Market Consolidated (Dominated by major players)

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Global Complement Inhibitors Market

On 08 August 2024, Novartis has announced that the U.S. FDA has granted accelerated approval for Fabhalta (iptacopan), a first-in-class complement inhibitor, for reducing proteinuria in adults with primary immunoglobulin A nephropathy (IgAN) at risk of rapid disease progression.

On April 2024, Voydeya (danicopan) has received approval in the US as an add-on therapy to ravulizumab (Ultomiris) or eculizumab (Soliris) for treating extravascular haemolysis (EVH) in adults with paroxysmal nocturnal haemoglobinuria (PNH). This first-in-class, oral Factor D inhibitor is intended for the 10-20% of PNH patients who experience significant EVH despite C5 inhibitor treatment.

On March 2024, ULTOMIRIS (ravulizumab-cwvz) has been approved by the FDA as the first and only long-acting C5 complement inhibitor for treating adult patients with anti-aquaporin-4 (AQP4) antibody-positive neuromyelitis optica spectrum disorder (NMOSD).

Global Complement Inhibitors Market Report - Table of Contents

RESEARCH OBJECTIVES AND ASSUMPTIONS

Research Objectives

Assumptions

Abbreviations

MARKET PURVIEW

Report Description

Market Definition and Scope

Executive Summary

Global Complement Inhibitors Market, By Stage of Development

Global Complement Inhibitors Market, By Mechanism of Action

Global Complement Inhibitors Market, By Route of Administration

Global Complement Inhibitors Market, By End-User

Coherent Opportunity Map (COM)

MARKET DYNAMICS, REGULATIONS, AND TRENDS ANALYSIS

Market Dynamics

Impact Analysis

Key Highlights

Regulatory Scenario

Product Launches/Approvals

PEST Analysis

PORTER’s Analysis

Merger and Acquisition Scenario

Global Complement Inhibitors Market, By Stage of Development, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Paroxysmal Nocturnal Hemoglobinuria (PNH)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Atypical Hemolytic Uremic Syndrome (aHUS)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Age-related Macular Degeneration (AMD)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Myasthenia Gravis

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Others

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Complement Inhibitors Market, By Mechanism of Action, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

C5 Inhibitors

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

C3 Inhibitors

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Terminal Complement Inhibitors

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Others

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Complement Inhibitors Market, By Route of Administration, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Intravenous (IV)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Subcutaneous (SC)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Complement Inhibitors Market, By End-User, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Hospitals and Specialty Clinics

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Retail Pharmacies

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Others

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Complement Inhibitors Market, By Region, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Mechanism of Action , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-User , 2020-2032, Value (USD Bn)

U.S.

Canada

Latin America

Introduction

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Mechanism of Action , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-User , 2020-2032, Value (USD Bn)

Brazil

Argentina

Mexico

Rest of Latin America

Europe

Introduction

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Mechanism of Action , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-User , 2020-2032, Value (USD Bn)

Germany

U.K.

Spain

France

Italy

Russia

Rest of Europe

Asia Pacific

Introduction

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Mechanism of Action , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-User , 2020-2032, Value (USD Bn)

China

India

Japan

Australia

South Korea

ASEAN

Rest of Asia Pacific

Middle East

Introduction

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Mechanism of Action , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-User , 2020-2032, Value (USD Bn)

GCC Countries

Israel

Rest of Middle East

Africa

Introduction

Market Size and Forecast, By Stage of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Mechanism of Action , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-User , 2020-2032, Value (USD Bn)

South Africa

North Africa

Central Africa

COMPETITIVE LANDSCAPE

Regeneron Pharmaceuticals

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Pharming Group

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

BioCryst Pharmaceuticals

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Amgen

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Omeros Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Ionis Pharmaceuticals

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Genentech (Roche)

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Novartis

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

F. Hoffmann-La Roche

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Eisai Co., Ltd.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Akari Therapeutics

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Care Pharma

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

NovelMed Therapeutics

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Zymeworks Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Daiichi Sankyo

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analyst Recommendations

Wheel of Fortune

Analyst View

Coherent Opportunity Map

References and Research Methodology

References

Research Methodology

About us

Global Complement Inhibitors Market Segmentation

By Stage of Development

Paroxysmal Nocturnal Hemoglobinuria (PNH)

Atypical Hemolytic Uremic Syndrome (aHUS)

Age-related Macular Degeneration (AMD)

Myasthenia Gravis

Others

By Mechanism of Action

C5 Inhibitors

C3 Inhibitors

Terminal Complement Inhibitors

Others

By Route of Administration

Intravenous (IV)

Subcutaneous (SC)

By End-User

Hospitals and Specialty Clinics

Retail Pharmacies

Others

Would you like to explore the option of buying individual sections of this report?

About author

Ghanshyam Shrivastava - With over 20 years of experience in the management consulting and research, Ghanshyam Shrivastava serves as a Principal Consultant, bringing extensive expertise in biologics and biosimilars. His primary expertise lies in areas such as market entry and expansion strategy, competitive intelligence, and strategic transformation across diversified portfolio of various drugs used for different therapeutic category and APIs. He excels at identifying key challenges faced by clients and providing robust solutions to enhance their strategic decision-making capabilities. His comprehensive understanding of the market ensures valuable contributions to research reports and business decisions.

Ghanshyam is a sought-after speaker at industry conferences and contributes to various publications on pharma industry.

Frequently Asked Questions :

How big is the Global Complement Inhibitors Market?

The Global Complement Inhibitors Market is estimated to be valued at USD 98.63 in 2025 and is expected to reach USD 277.07 Billion by 2032.

What are the major factors driving the Global Complement Inhibitors Market growth?

The increasing prevalence of complement-related disorders and growth in biologics for complement-related disorders are the major factor driving the Global Complement Inhibitors Market.

Which is the leading Stage Of Development in the Global Complement Inhibitors Market?

The leading Stage Of Development segment is Paroxysmal Nocturnal Hemoglobinuria (PNH) .

Which are the major players operating in the Global Complement Inhibitors Market?

Regeneron Pharmaceuticals, Pharming Group, BioCryst Pharmaceuticals, Amgen, Omeros Corporation, Ionis Pharmaceuticals, Genentech (Roche), Novartis, Hoffmann-La Roche, Eisai Co., Ltd., Akari Therapeutics, Care Pharma, NovelMed Therapeutics, Zymeworks Inc., Daiichi Sankyo are the major players.

What will be the CAGR of the Global Complement Inhibitors Market?

The CAGR of the Global Complement Inhibitors Market is projected to be 15.9% from 2025-2032.

Missing comfort of reading report in your local language? Find your preferred language :

By Stage of Development - Rising Prevalence and No Approved Treatment

By Stage of Development - Rising Prevalence and No Approved Treatment