Leiomyosarcoma Treatment Market Size - Analysis

Market Size in USD Bn

CAGR9.2%

| Study Period | 2025-2032 |

| Base Year of Estimation | 2024 |

| CAGR | 9.2% |

| Market Concentration | High |

| Major Players | Pfizer Inc., Novartis AG, Eli Lilly and Company, Bristol-Myers Squibb Company, Merck & Co., Inc. and Among Others |

please let us know !

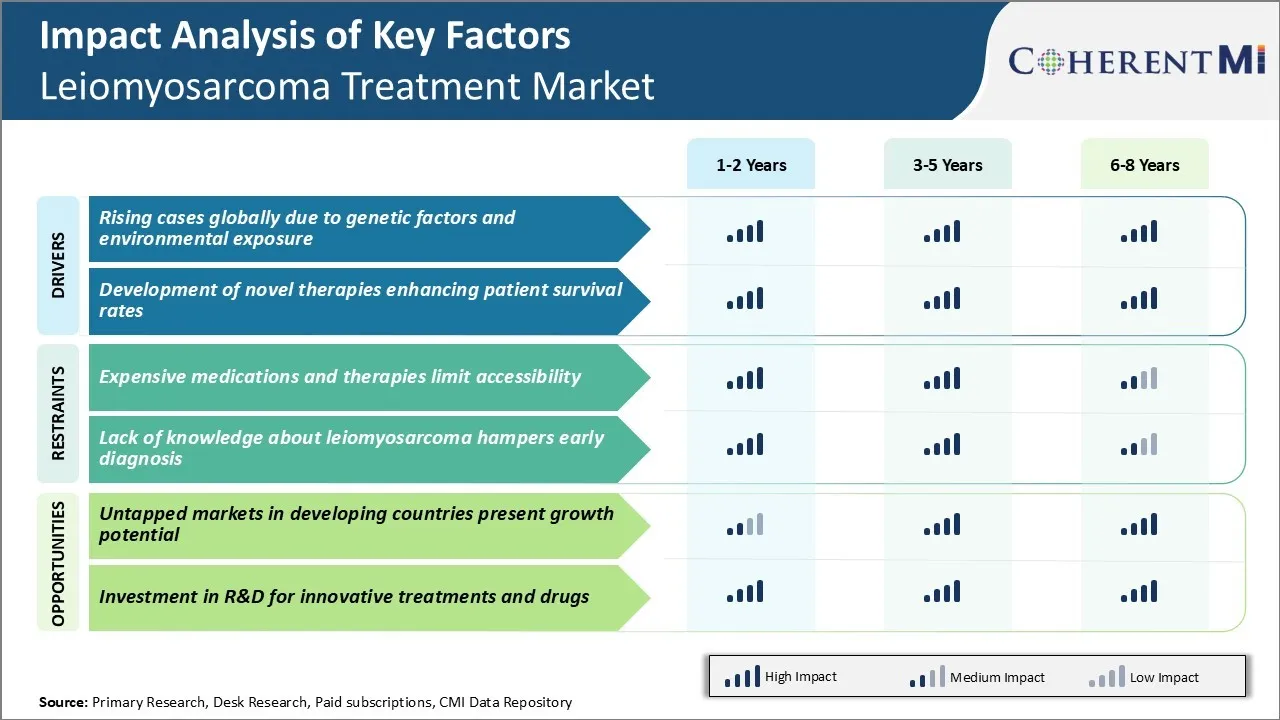

Leiomyosarcoma Treatment Market Trends

One of the prominent drivers augmenting the growth of leiomyosarcoma treatment market is the steadily rising disease prevalence worldwide. Leiomyosarcoma is primarily caused by an interplay of genetic and environmental influences. Prolonged exposure to certain occupational and environmental carcinogens. Industrial workers engaged in petrochemical industry, agriculture and maintenance occupations have demonstrated elevated susceptibility.

Unfortunately, growing industrialization and urbanization over the past few decades have aggravated community-level exposure to aforementioned environmental risk factors on a global scale. Developing countries lacking stringent safety regulations have borne the maximum brunt. Additionally, increased lifespan and aging demography even in developed countries imply a constantly expanding pool of elderly population under threat.

Another key promoter for leiomyosarcoma treatment market is the ongoing research and success in introducing novel treatment methods with improved efficacy. Over the last decade, significant breakthroughs have been made in unravelling the molecular pathways involved in leiomyosarcoma pathogenesis.

Preliminary data indicate these targeted and immune-based treatment options may help improve progression-free and overall survival when administered alone or in combination with existing standards of care. If ongoing phase 3 trials validate their safety and efficacy profiles, several novel systemic therapies are expected to receive regulatory approvals in the coming years. Their commercial introduction will go a long way in enhancing patient outcomes by curtailing recurrence, extending survival periods and providing newer lines of treatment after failure of first line therapy. This vastly improved treatment landscape raises hope of containing disease fatality rates over the next decade.

One of the major challenges faced by the leiomyosarcoma treatment market is the high cost of available medications and therapies. Leiomyosarcoma is a rare type of cancer and available treatment options are very limited. The drugs approved by regulatory authorities for leiomyosarcoma treatment have a very high cost of therapy, sometimes running into hundreds of thousands of dollars for a full course of treatment. This makes the treatment unaffordable for many patients.

The lack of affordable generic alternatives in the market further exacerbates the problem. Unless newer low-cost treatment alternatives are identified, the issue of accessibility is likely to remain a major challenge constraining market growth.

Market Opportunity - Untapped Markets in Developing Countries Present Growth Potential for Market

Countries such as India, Brazil, China, South Africa and others present a huge market potential considering their large population bases and improving medical capabilities. However, awareness levels regarding leiomyosarcoma remain relatively low in the developing world compared to developed markets. With focused marketing and educational initiatives, significant headway can be made into previously untapped markets and new patient pools.

Prescribers preferences of Leiomyosarcoma Treatment Market

Leiomyosarcoma is an advanced form of soft tissue cancer that has multi-line treatment options depending on the stage and progression of the disease. In early stages (I-II), surgery to remove the tumor is the primary line of treatment. For late stage or metastatic disease (III-IV), chemotherapy is prescribed as the frontline treatment. Doxorubicin or gemcitabine alone or in combination with docetaxel are common first-line options. If the cancer progresses, pazopanib (Votrient) is often prescribed as the second-line treatment.

Immunotherapies like pembrolizumab (Keytruda) are emerging as promising alternatives in pre-treated patients. Given the limited treatment options and high unmet need, prescribers actively consider enrollment in clinical trials evaluating new drugs. The response duration to prior therapies and tolerability profile strongly influences individual prescribing decisions.

Treatment Option Analysis of Leiomyosarcoma Treatment Market

Leiomyosarcoma can be categorized into localized, locally advanced or metastatic stages depending on the extent of disease spread. For localized disease, surgery remains the mainstay of treatment with negative margins being the goal. For tumors deemed unresectable, neoadjuvant (pre-operative) or adjuvant (post-operative) radiation along with chemotherapy may be employed.

For patients who progress on first-line chemotherapy or are unsuitable for it, pazopanib monotherapy remains a standard second-line option. Pazopanib is a multi-kinase inhibitor targeting vascular endothelial growth factor receptors which promotes tumor angiogenesis. Its brand name is Votrient. Median progression-free survival with pazopanib is 4.6 months based on clinical evidence.

Key winning strategies adopted by key players of Leiomyosarcoma Treatment Market

Focus on targeted therapies: Major players like Pfizer, Johnson & Johnson have focused on developing targeted therapies for LMS treatment. In 2017, Johnson & Johnson's drug Votrient (pazopanib) was approved for advanced LMS. It targets VEGFR pathways which are important for tumor growth. This helped widen treatment options beyond traditional chemotherapy.

Clinical trials: Companies conduct late phase clinical trials to seek regulatory approvals. In 2021, Eli Lilly reported positive results from a Phase 3 trial of sintilimab plus pemetrexed/platinum chemo for pre-treated LMS. If approved, it will be a new first-line option. Similarly, trials are evaluating the potential of immunotherapies like pembrolizumab.

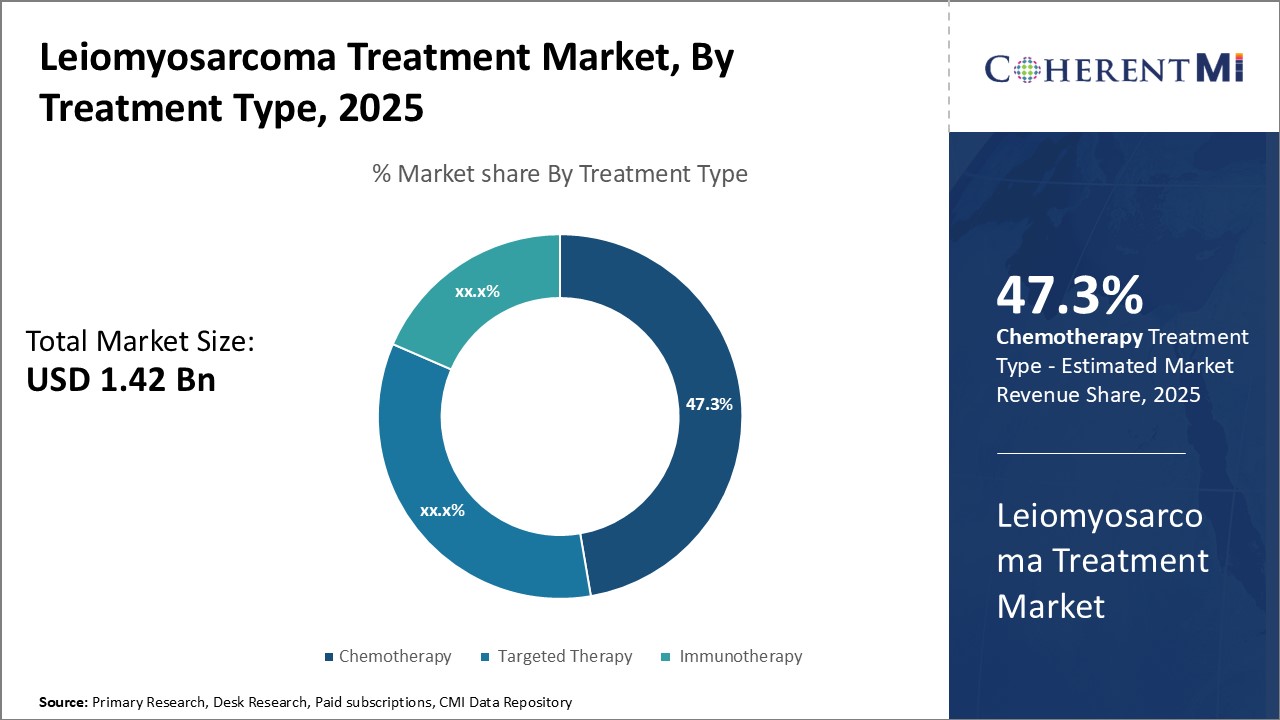

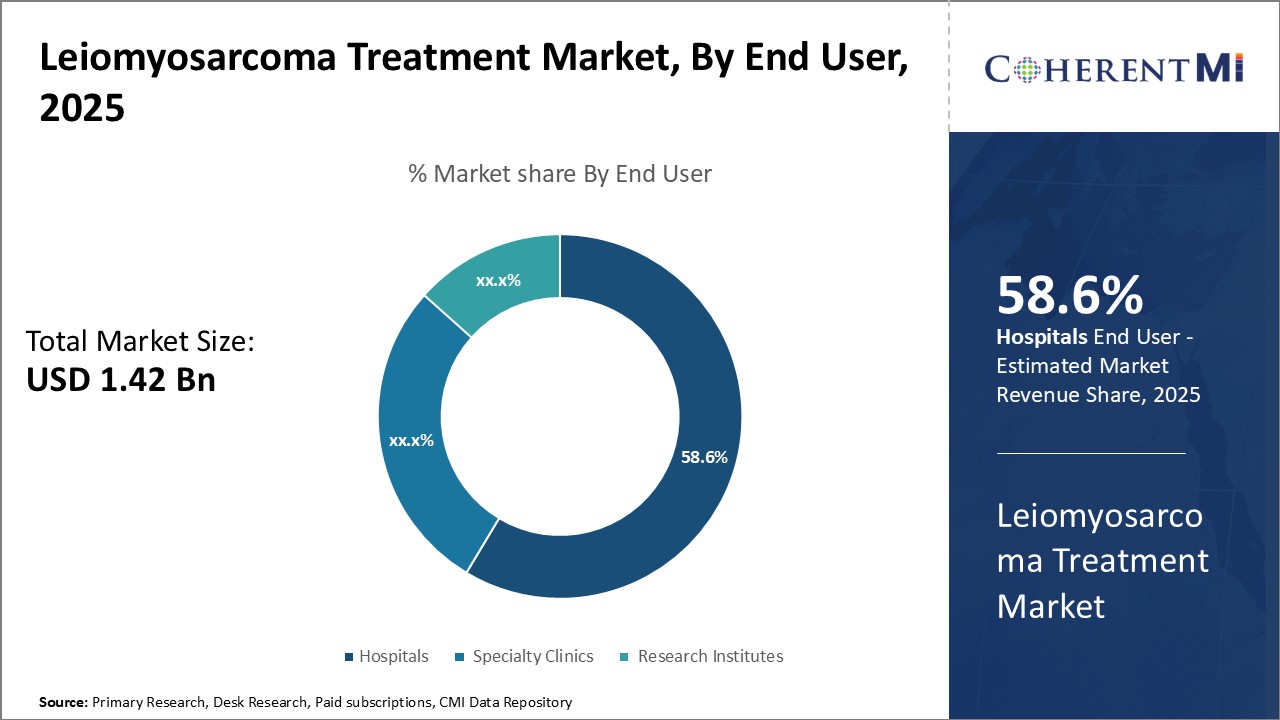

Segmental Analysis of Leiomyosarcoma Treatment Market

Insights, By Treatment Type: Established Efficacy Drives Dominance of Chemotherapy

Insights, By Treatment Type: Established Efficacy Drives Dominance of ChemotherapyWithin the treatment type segment of the leiomyosarcoma treatment market, chemotherapy accounts for the largest share. Doxorubicin in particular has long been the standard first-line treatment for leiomyosarcoma since it was shown to offer a response rate of 26% when used as a single agent in early clinical trials. Decades of clinical use have demonstrated doxorubicin's ability to slow tumor growth and prolong survival, making it the preferred option for both newly diagnosed and recurrent/metastatic cases.

Given chemotherapy's established performance supported by a wealth of long-term outcome data, oncologists routinely recommend regimens containing doxorubicin or gemcitabine as the foundation of initial leiomyosarcoma treatment. Until newer modalities unequivocally prove they can match or exceed chemotherapy's results, it will remain the mainstay first-line approach driving the segment's market share leadership.

Within the end user segment for leiomyosarcoma treatment, hospitals account for the largest share due to their institutional expertise in managing rare cancers. Leiomyosarcoma is a uncommon soft tissue sarcoma, so individual oncologists or clinics may only encounter a few cases per year. Hospitals with specialized sarcoma centers see much higher patient volumes and are best positioned to stay abreast of the latest treatment protocols.

While specialty oncology clinics play an increasing outpatient role, most leiomyosarcoma patients - especially those with advanced or recurrent disease - ultimately interface most extensively with hospitals for intensive treatments and management of complications. This institutional dominance in handling even the most difficult cases drives their position as the leading end user category.

Insights, By Diagnosis Method: Immediate Visualization Drives Preference for Imaging Tests In Diagnosis

While biopsy provides the definitive diagnostic confirmation, tissue sampling carries risks of complications from an invasive procedure and may still not capture heterogeneous areas of tumor biology. Imaging allows surgeons to optimally target the biopsy while also mapping out operative approaches beforehand. Follow-up scans also play a key role in monitoring response to neoadjuvant treatments or detecting recurrence, as leiomyosarcoma has an inherent tendency for distant metastases that may not be detected by physical exam alone.

Additional Insights of Leiomyosarcoma Treatment Market

- Incidence Rate: Leiomyosarcoma accounts for approximately 10-20% of soft tissue sarcoma cases globally.

- Survival Rate: The five-year survival rate for localized leiomyosarcoma is around 63%, emphasizing the need for better treatments.

- Clinical Trial Success: A groundbreaking study demonstrated that combining immunotherapy with chemotherapy significantly improved survival rates in advanced leiomyosarcoma patients.

- Regulatory Approvals: Multiple drugs received approval in key markets, providing patients with more treatment options and boosting market growth.

Competitive overview of Leiomyosarcoma Treatment Market

The major players operating in the Leiomyosarcoma Treatment Market include Pfizer Inc., Novartis AG, Eli Lilly and Company, Bristol-Myers Squibb Company, Merck & Co., Inc., GlaxoSmithKline plc, Johnson & Johnson, Sanofi S.A., AstraZeneca plc, and AbbVie Inc.

Leiomyosarcoma Treatment Market Leaders

- Pfizer Inc.

- Novartis AG

- Eli Lilly and Company

- Bristol-Myers Squibb Company

- Merck & Co., Inc.

Leiomyosarcoma Treatment Market - Competitive Rivalry

Leiomyosarcoma Treatment Market

(Dominated by major players)

(Highly competitive with lots of players.)

Recent Developments in Leiomyosarcoma Treatment Market

- In July 2023, Pfizer Inc. announced a strategic collaboration with a biotech firm to develop a new targeted therapy for leiomyosarcoma, aiming to improve efficacy and reduce side effects. Pfizer also announced a partnership with Flagship Pioneering to invest $100 million in developing a pipeline of 10 single-asset programs targeting unmet medical needs. This collaboration aims to explore innovative medicines across various disease areas, leveraging Flagship's biotech platforms and Pfizer's development capabilities.

- In May 2023, Novartis AG launched a clinical trial for a novel immunotherapy drug, potentially offering a new line of treatment for patients unresponsive to conventional therapies.

- In March 2023, Eli Lilly and Company received FDA fast-track designation for their experimental drug targeting advanced leiomyosarcoma, expediting the review process.

- January 2023: Bristol-Myers Squibb Company expanded its oncology portfolio by acquiring a startup focused on sarcoma research, enhancing its position in the leiomyosarcoma market. Furthermore, key acquisitions by Bristol-Myers Squibb in 2023 included Mirati Therapeutics, RayzeBio, and Karuna Therapeutics, which were primarily aimed at strengthening their position in oncology and neuroscience. These acquisitions added several assets to their portfolio, particularly in areas like lung cancer and radiopharmaceutical therapeutics.

Leiomyosarcoma Treatment Market Segmentation

- By Treatment Type

- Chemotherapy

- Doxorubicin

- Gemcitabine

- Ifosfamide

- Targeted Therapy

- Pazopanib

- Trabectedin

- Immunotherapy

- Pembrolizumab

- Nivolumab

- Chemotherapy

- By End User

- Hospitals

- Specialty Clinics

- Research Institutes

- By Diagnosis Method

- Imaging Tests

- MRI

- CT Scan

- PET Scan

- Biopsy Techniques

- Needle Biopsy

- Surgical Biopsy

- Imaging Tests

Would you like to explore the option of buying individual sections of this report?

Ghanshyam Shrivastava - With over 20 years of experience in the management consulting and research, Ghanshyam Shrivastava serves as a Principal Consultant, bringing extensive expertise in biologics and biosimilars. His primary expertise lies in areas such as market entry and expansion strategy, competitive intelligence, and strategic transformation across diversified portfolio of various drugs used for different therapeutic category and APIs. He excels at identifying key challenges faced by clients and providing robust solutions to enhance their strategic decision-making capabilities. His comprehensive understanding of the market ensures valuable contributions to research reports and business decisions.

Ghanshyam is a sought-after speaker at industry conferences and contributes to various publications on pharma industry.

Frequently Asked Questions :

How big is the leiomyosarcoma treatment market?

The leiomyosarcoma treatment market is estimated to be valued at USD 1.42 billion in 2025 and is expected to reach USD 2.63 billion by 2032.

What are the key factors hampering the growth of the leiomyosarcoma treatment market?

The expensive medications and therapies limit accessibility and lack of knowledge about leiomyosarcoma hampers early diagnosis are the major factor hampering the growth of the leiomyosarcoma treatment market.

What are the major factors driving the leiomyosarcoma treatment market growth?

The rising cases globally due to genetic factors and environmental exposure and development of novel therapies enhancing patient survival rates are the major factor driving the leiomyosarcoma treatment market.

Which is the leading treatment type in the leiomyosarcoma treatment market?

The leading treatment type segment is chemotherapy.

Which are the major players operating in the leiomyosarcoma treatment market?

Pfizer Inc., Novartis AG, Eli Lilly and Company, Bristol-Myers Squibb Company, Merck & Co., Inc., GlaxoSmithKline plc, Johnson & Johnson, Sanofi S.A., AstraZeneca plc, and AbbVie Inc. are the major players.

What will be the CAGR of the leiomyosarcoma treatment market?

The CAGR of the leiomyosarcoma treatment market is projected to be 9.2% from 2025-2032.