米国の熱可塑性エラストマー市場 サイズ - 分析

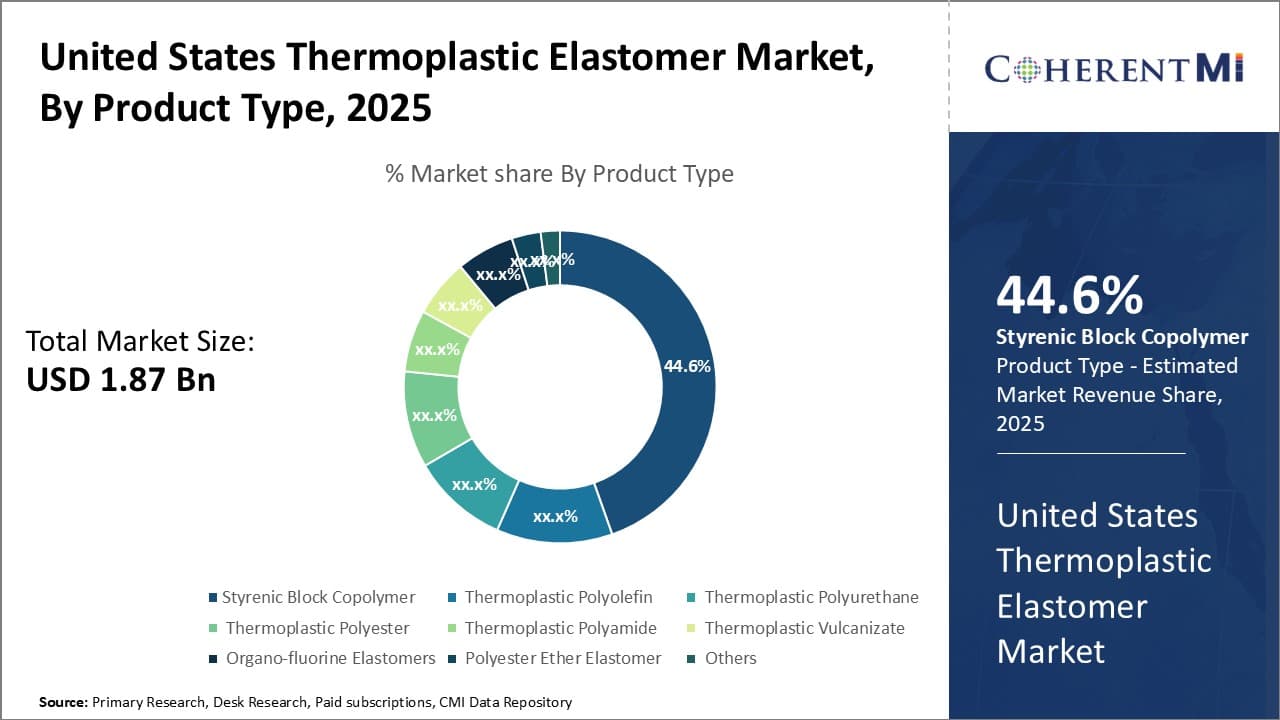

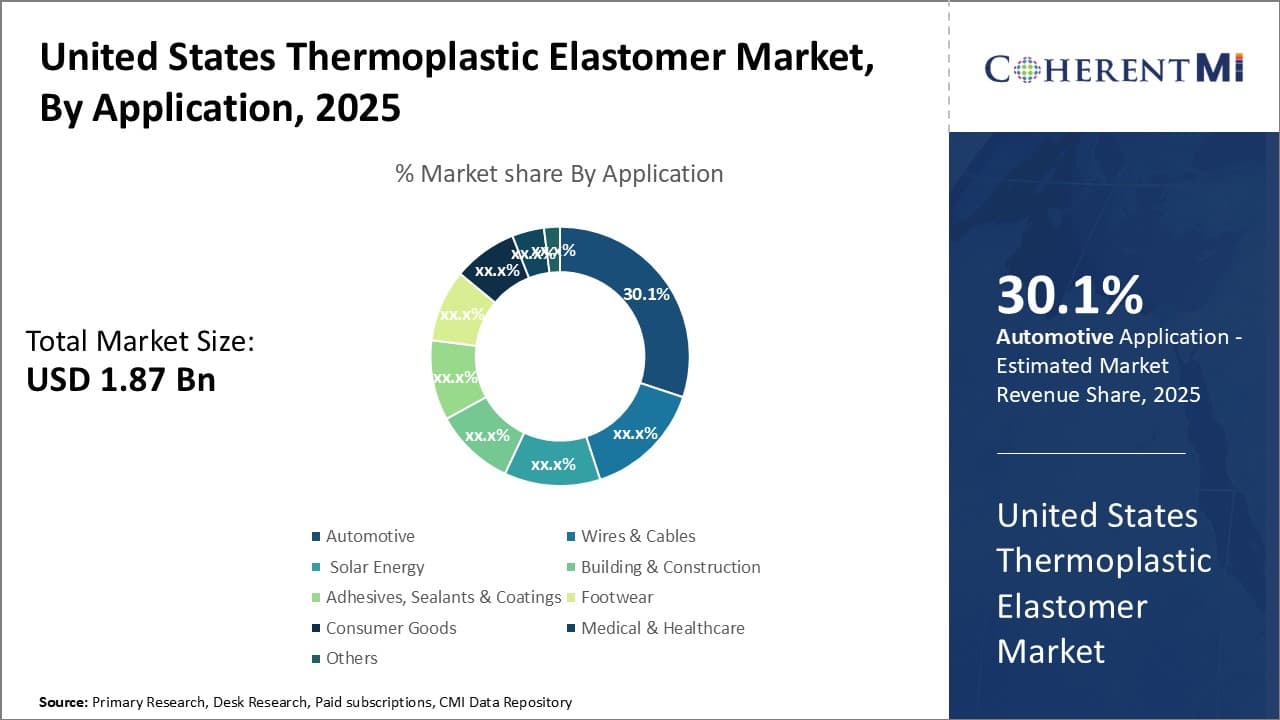

米国熱可塑性エラストマー市場が評価されると推定される 2025年のUSD 1.87 Bn そして到達する予定 2032年までのUSD 2.76 Bn, 成長 2025年から2032年までの5.7%のCAGR。

熱可塑性エラストマーはこの市場の成長を運転している自動車、医学および構造の企業で広い適用を見つけます。 自動車業界からの需要が高まっています。

市場規模(米ドル) Bn

CAGR5.7%

| 調査期間 | 2025-2032 |

| 推定の基準年 | 2024 |

| CAGR | 5.7% |

| 市場集中度 | Medium |

| 主要プレーヤー | ジラードゴム株式会社, エアロゴム株式会社, ダンネージエンジニアリング, アライアンスゴムカンパニー, アルパインエラストマー製品, LLC その他 |

お知らせください!

米国の熱可塑性エラストマー市場 トレンド

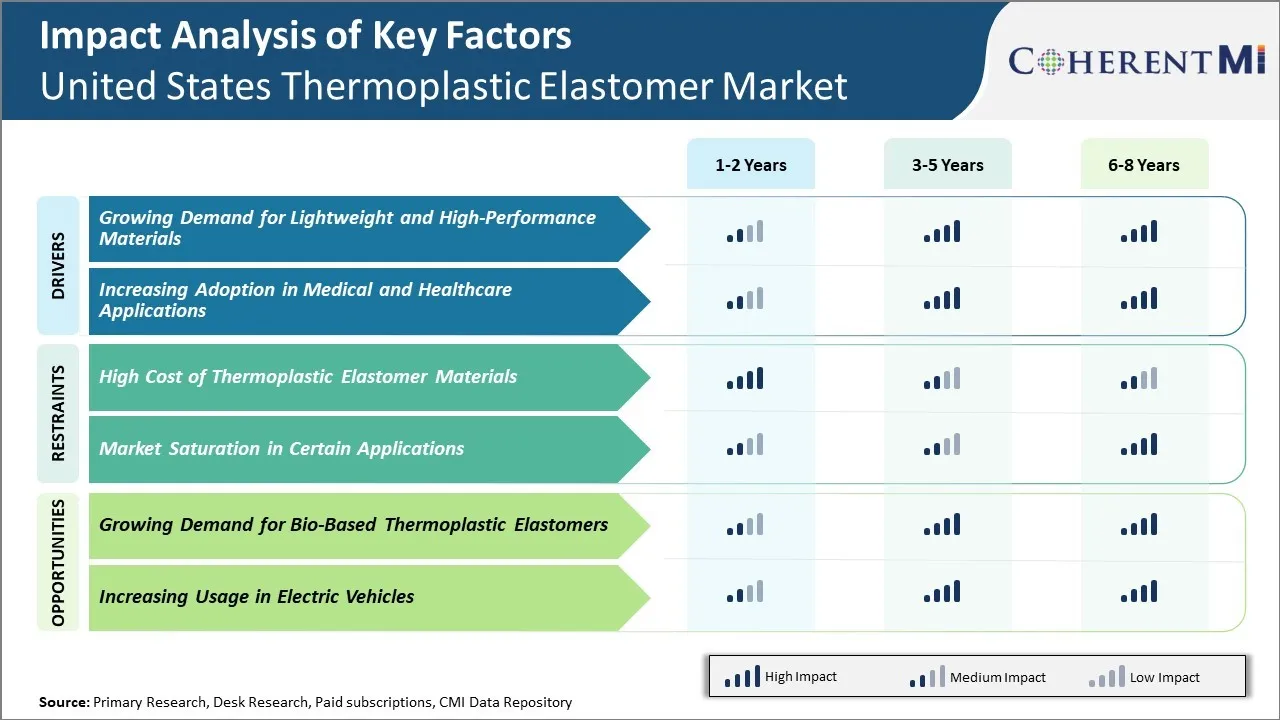

市場ドライバ - 軽量で高性能な材料の需要を成長させる

自動車、建設、航空宇宙などのさまざまな産業における軽量で高性能な材料の需要は、米国の熱可塑性エラストマー市場の成長を牽引する主要な要因の一つです。 熱可塑性エラストマーは、柔軟性、耐衝撃性、強度を必要とする用途に理想的な材料を作る熱可塑性およびエラストマーの性質を持っています。

従来の材料と比較されて、熱可塑性エラストマーは重量の大いにより軽く、等しくか改善された機械性能を提供します。 例えば、熱可塑性ポリウレタンエラストマーは、標準ゴム材料よりも25%軽量です。 自動車業界は、燃費を向上した軽自動車の開発に着目し、厳しい排出基準を満たしています。 交通統計局によると、2020-2021年~2021年にかけて軽量車両材料の採用が増加し、米国の新車の平均燃費を6%削減しました。 軽量材料のこの上昇焦点はバンパー、ドア シールおよびグリルのようなさまざまな自動車部品の製造の熱可塑性エラストマーの使用を運転しています。

市場ドライバー – 医療およびヘルスケアアプリケーションにおける採用の増加

米国における医療およびヘルスケア業界は、過去数年間で途上国で途上国で途上国で成長が見られ、その後の軌跡を継続することが期待されています。 熱可塑性エラストマーは、柔軟性、耐久性、生体適合性などの望ましい特性のために、さまざまな医療機器やアプリケーションでますます活用されています。 高い変化のflexural持久力のような特性は適用範囲が広い管、カテーテルおよび傷の心配プロダクトのような反復的な屈曲か圧縮を要求する適用のために適したTPEを作ります。 また、熱溶着性により、効率性やコストの削減を実現します。

疾病管理予防センターの統計によると、手術器具、使い捨て機器、インプラントを2019年に約65万人のアメリカ人が関与する医療処置を受けています。 単一使用の医療用品および装置のためのこの要求は換気装置、酸素マスクおよび他の呼吸器装置のための高められた必要性が付いているCOVID-19のパンデミックの間に更にsurged。 熱可塑性エラストマーは、他の材料よりもその加工の利点のために、これらの時系列製品を製造する際に重要な役割を果たしました。

市場課題 – 熱可塑性エラストマー材料の高コスト

熱可塑性エラストマー材料の高コストは、米国の熱可塑性エラストマー市場の成長のための主要な抑制要因の一つです。 熱可塑性エラストマーは熱可塑性およびエラストマーの特性がある設計されていたポリマーです。 従来のサーモセットのゴム上の生産の再生性、設計柔軟性、耐久性および容易さのような利点があります。 しかし、熱可塑性エラストマーは、複雑な分子構造と生産プロセスが関与しているため、通常の熱可塑性と比較して生産するために高価です。

スチレンブロック共重合体、熱可塑性オレフィンなどの熱可塑性エラストマーの生産に必要な原材料のコストが高まり、さらなる価格を上げます。 米国国際貿易委員会によると、米国のスチレンブロックコポリマーの輸入価格は2020年1月に$ 2.12 / kgから2022年1月に増加しました。 同様に、米国の熱可塑性ポリウレタンの輸入価格は、同じ期間に$ 3.78 / kgから$ 4.23 / kgに成長しました。 プロピレン、エチレン、クロードオイルの価格 - 熱可塑性生産のための主要なフィードストックはまた、COVID-19パンデミックによるサプライチェーンの崩壊による最後の2年間で大きな上昇を目撃しました 熱可塑性エラストマーコスト。

このレポートの詳細については、 無料サンプルコピーをダウンロード

このレポートの詳細については、 無料サンプルコピーをダウンロード

市場機会 - バイオベースの熱可塑性エラストマーの需要を成長させる

米国における熱可塑性エラストマー市場におけるバイオベースの持続可能な材料の需要の高まりは大きなチャンスです。 伝統的に、ほとんどの熱可塑性エラストマーは石油ベースの成分から派生しています。 しかしながら、環境意識の向上と持続可能性の目標、ブランド、消費者が低炭素のフットプリントを下回る選択肢を求めています。

バイオベースの熱可塑性エラストマーは、部分的にまたは完全に植物および農作物ソースから派生し、メーカーはより環境に優しい製品を処方することができます。 トウモロコシ、大豆、糖蜜、セルロースなどのバイオベースの成分をポリマー構造内で利用する新たな配合が誕生しました。 これらは、生産中にいくつかの化石燃料を必要とし、廃棄時に終生の排出量を削減したため、より持続可能なものであることの基準を満たします。 多くのグローバル組織は、バイオ経済および循環型バイオベースの産業の発展を奨励しています。 経済協業開発機構(OECD)による報告書によると、バイオベースの経済は、2030年までに7-8%のグローバル製造出力に貢献できる可能性があります。

自動車、消費財、医療業界は、バイオベースの熱可塑性エラストマーの早期採用者です。 例えば、BASFは内部のトリムや他の自動車部品にコンパイルされたバイオベースのTPUを開発するために、いくつかの自動車メーカーと提携しています。

セグメント分析 米国の熱可塑性エラストマー市場

このレポートの詳細については、 無料サンプルコピーをダウンロード洞察力、製品の種類によって: 多様性とStyrenicブロック共重合の耐久性

このレポートの詳細については、 無料サンプルコピーをダウンロード洞察力、製品の種類によって: 多様性とStyrenicブロック共重合の耐久性

製品の種類に関しては、スチレンブロックコポリマーサブセグメントは、その多様性と耐久性を所有する市場で44.6%の最高のシェアに貢献します。

SBCとして一般に知られているStyrenicブロック共重合体は、米国熱可塑性エラストマー市場における主要な製品タイプとしてそれ自体を確立しました。 SBCは、優れた弾性特性と相まって、メーカーの優れた柔軟性と靭性を提供します。 ソフトアモルファスポリブタジエンまたはポリイソプリンの中間ブロックによって結合された硬質結晶ポリスチレンエンドブロックから成るその形態学は、特徴のユニークな組み合わせを提供します。

SBCは、従来のゴム材料よりも簡単に処理できるため、より高い温度で何度もリサイクル、再成形、再成形が可能です。 この再生性プロパティは、自動車分野での人気の主要なドライバです。 自動車メーカーは、部品統合により製造コストを削減するSBCを好む。 複数のプラスチックおよびゴム製部品は単一のSBCの部品によって、車のアセンブリを簡素化する取り替えることができます。

SBCの要求を支持するもう一つの主要因は、他の熱可塑性エラストマーと比較して、その優れた耐候性とUV抵抗です。 屋外のケーブルおよびワイヤー絶縁材の広範な使用法を可能にします。 また、その弾力性のある機械的特性と革のような美学のためにPVCの代替品として履物産業でトラクションを獲得しています。

このレポートの詳細については、 無料サンプルコピーをダウンロード

このレポートの詳細については、 無料サンプルコピーをダウンロード

アプリケーションによる洞察: 高度なエラストマーの大規模採用

応用面では、自動車のサブセグメントは、先進のエラストマーの大規模採用に30.1%を占めています。

自動車部門は、米国熱可塑性エラストマー市場の優位性を保持しています。 自動車内装、外装、部品など多岐に渡り、コストダウンで高い性能が求められます。 現代の車は、快適さ、安全、アセンブリの容易さを提供するために、平均して、さまざまなエラストマー材料の20キロ以上が含まれています。

TPEは、EPDMやスチレンゴムなどの熱硬化剤を自動車用途に置き換えることがますますます増加しています。リサイクル、低ツーリングコスト、より迅速な処理サイクル、優れた美的特性などの利点があります。 製造業者は別のゴムおよびプラスチック部品を統一し、軽量の部品に統合するためにTPEsを好みます。 燃料効率と炭素排出量削減のための厳しい要件を満たしています。

SBCsは、ゴムのような弾力性と油、化学物質、温度変動に対する耐性のために、自動車シール、耐候性および防振用途で広範囲にわたる実装を発見しました。 TPUはホース、Oリング、ガスケットおよびシールで流体に対する漏れ防止バリアを提供します。

さらに、ラグジュアリー、快適性、コネクティビティ機能に対する成長を続けるコンシューマーは、カーメーカーがインテリアトリム、ダッシュ、ドアパネル、コンソールで高度なTPEを採用しています。

競合の概要 米国の熱可塑性エラストマー市場

米国の熱可塑性エラストマー市場で運営されている主要なプレーヤーには、Girard Rubber Corp、Aero Rubber Company、Inc、Dunnage Engineering、Alpine Elastomer Products、LLC、CS Hyde Company、Emes Rubco Company、Warco、およびPlazt、およびPlasce。

米国の熱可塑性エラストマー市場 リーダー

- ジラードゴム株式会社

- エアロゴム株式会社

- ダンネージエンジニアリング

- アライアンスゴムカンパニー

- アルパインエラストマー製品, LLC

最近の動向 米国の熱可塑性エラストマー市場

- 2023年8月、Covestro AGは、中国上海のVerbundサイトで新しいエラストマー工場を建設する計画を発表しました。 同社の生産能力を増加させ、地域における熱可塑性エラストマーの需要が高まると予想されます。

- 2020年7月、旭化成株式会社が、Thermyleneファミリーポートフォリオの一環として、プラスチック北米(APNA)と新エンジニアリング樹脂シリーズを発売しました。 熱可塑性エラストマー製品の広い範囲を顧客に提供するこの拡張目的。

- 2021年1月、ハンツマン株式会社が北米専門化学メーカーであるGabriel Performance Products社を買収。 この買収は、Technylなどの革新的で有名な製品でBASFのポリアミド機能を拡張しました。

米国の熱可塑性エラストマー市場 セグメンテーション

- 製品タイプ別

- Styrenicブロックコポリマー

- 熱可塑性ポリオレフィン

- 熱可塑性 ポリウレタン

- 熱可塑性ポリエステル

- 熱可塑性ポリアミド

- 熱可塑性加硫

- Organo-fluorine エラストマー

- ポリエステル エーテルのエラストマー

- その他

- 用途別

- 自動車産業

- ワイヤーおよびケーブル

- 太陽エネルギー(太陽光発電用途)

- 建築・建設

- 接着剤、シーリング剤及びコーティング

- フットウェア

- 消費者製品

- 医療・ヘルスケア

- その他

購入オプションを検討しますか?このレポートの個々のセクション?

Vidyesh Swar は、市場調査とビジネス コンサルティングの多様なバックグラウンドを持つ熟練したコンサルタントです。6 年以上の経験を持つ Vidyesh は、カスタマイズされた調査ソリューションのための市場予測、サプライヤー ランドスケープ分析、市場シェア評価の熟練度で高い評価を得ています。業界に関する深い知識と分析スキルを駆使して、貴重な洞察と戦略的な推奨事項を提供し、クライアントが情報に基づいた決定を下し、複雑なビジネス ランドスケープを乗り切れるように支援します。