Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market is segmented By Diagnosis Method (linical Assessment, Imaging Techniques, Laboratory Tests), By Severity-Based Diagnosis (GOLD 1–4 Classification, Groups A–D Classification), By Molecule Type (Monoclonal Antibody , Peptides, Polymer, Small molecule, Gene therapy), By Product (Mono, Combination, Mono/Combination), By Geography (North America, Latin America, Asia Pacific, Europe, Middle East, and Africa). The report offers the value (in USD billion) for the above-mentioned.

Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market is segmented By Diagnosis Method (lini...

The chronic obstructive pulmonary disease (COPD) diagnosis market is estimated to be valued at USD 2.29 billion in 2025 and is expected to reach USD 3.24 billion by 2032, growing at a compound annual growth rate (CAGR) of 5.1% from 2025 to 2032. Market growth can be attributed to the growing geriatric population which are more susceptible to COPD, increasing pollution levels leading to higher incidence of COPD, and availability of more accurate diagnostic tests to detect early stages of COPD.

Market Size in USD Bn

CAGR5.1%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

5.1%

Market Concentration

Medium

Major Players

GlaxoSmithKline (GSK), AstraZeneca, Boehringer Ingelheim, Novartis, Teva Pharmaceuticals and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

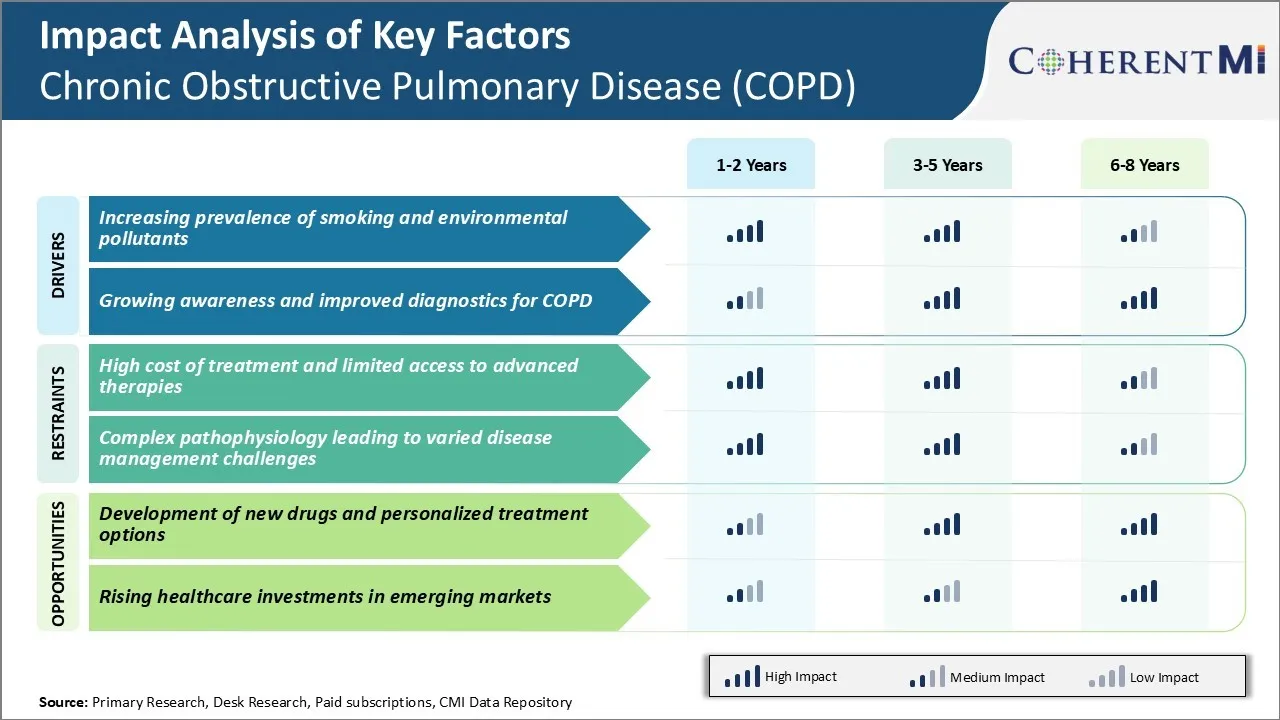

Market Driver - Increasing Prevalence of Smoking and Environmental Pollutants

The increasing prevalence of smoking across the world has significantly contributed to the rising cases of COPD. As per various studies conducted across countries, smoking is identified as the primary cause of COPD worldwide. Both active as well as passive smoking increases the risk of developing COPD. Although governments are implementing strict regulations against smoking in public areas, the cultural acceptance of smoking in social gatherings continues to expose non-smokers to second-hand smoke.

Additionally, prolonged exposure to toxic fumes and pollutants through industrial, vehicle emissions and biomass burning for cooking also increases the risk for COPD, especially in developing nations. The high levels of air pollution in urban areas have negatively impacted lung health. The toxic mix of gases and particulate matter in polluted air causes chronic inflammation in lungs, which coupled with smoking habits have aggravated the cases of COPD.

Unless urgent efforts are made to curb smoking and reduce environmental pollution, the incidence of COPD is expected to continue rising in the coming years. This will correspondingly drive greater demand for COPD diagnosis tests to identify cases at early stages so as to better manage the condition.

Market Driver – Growing Awareness and Improved Diagnostics for COPD

Over the past few years, awareness about COPD as a serious medical condition distinct from other lung disorders has increased substantially among both public and healthcare providers. Various international health organizations and foundations have taken initiatives to educate people on the symptoms, risk factors and importance of early diagnosis of COPD through public awareness campaigns. This has encouraged more at-risk individuals and general public to seek medical advice for respiratory problems.

On the other hand, diagnostic capabilities for COPD have also enhanced significantly with the development of advanced tools. Spirometry test is now widely used as the gold standard test to detect airway obstruction and confirm COPD diagnosis by measuring lung function.

Moreover, other diagnostic exams like chest X-rays, CT scans and blood tests have become more effective in evaluating the severity of COPD and related complications. Wider availability of diagnostic services and mobile medical vehicles have additionally improved accessibility in rural regions.

The improved diagnostic approach helps clinicians to accurately identify COPD at initial stages and accordingly prescribe most suitable treatment plans. As greater number of patients undergo spirometry and other tests annually on the recommendation of doctors, it will augment the demand for COPD diagnostics market.

Market Challenge - High Cost of Treatment and Limited Access to Advanced Therapies

COPD diagnosis and treatment carries a high economic burden globally. The cost of medications, frequent hospitalizations, oxygen therapy and other supportive treatments pushes the overall cost of managing COPD to elevated levels. This financial toll acts as a significant barrier for many patients suffering from more severe forms of the disease.

Furthermore, access to newer and more advanced therapies remains limited even in developed markets due to their typically high price points. Lung volume reduction surgery, bronchial thermoplasty and lung transplantation are some examples of such specialized treatment procedures that are often out of reach for average patients.

The high costs also limit investments into research and development of newer treatment approaches. Overall, the lack of affordability and accessibility of advanced care options severely impacts disease management and clinical outcomes for COPD patients worldwide.

Market Opportunity - Development of New Drugs and Personalized Treatment Options

The COPD diagnosis and treatment landscape remains ripe with opportunities for innovation. With rising disease prevalence projected in the coming decades, major pharmaceutical players and startups continue investing heavily into developing novel drugs with new mechanisms of action.

Some promising new classes of drugs in clinical trials include PDE4 inhibitors, bronchodilators with mucus clearance properties and biologics targeting inflammation. There is also a shift towards more personalized therapies tailored to a patient's disease phenotype, genotype or biomarker profile. Advancements in wearable sensors, imaging techniques and molecular diagnostics are enabling better patient stratification and selection of optimized treatment regimen.

This move towards precision medicine holds potential to drive higher success rates, better tolerability and ultimately improved health outcomes for COPD sufferers.

Prescribers preferences of Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market

COPD treatment follows a stepwise approach based on the severity and symptoms of the disease. For mild COPD, short-acting bronchodilators as needed are usually prescribed. Common medications used are short-acting beta2-agonists (SABAs) like salbutamol (Ventolin) and ipratropium bromide (Atrovent).

As COPD progresses to moderate stages, maintenance therapy with long-acting bronchodilators is added. Common options include long-acting muscarinic antagonists (LAMAs) such as tiotropium (Spiriva) and long-acting beta2-agonists (LABAs) like salmeterol (Serevent) and formoterol (Foradil, Symbicort). These can be used alone or in combinations like tiotropium/olodaterol (Stiolto Respimat) or formoterol/beclomethasone (Fostair).

For severe COPD, LAMA/LABA combinations are preferred for maintenance along with as-needed SABAs. Alternatively, physicians may prescribe the triple combination of LAMA/LABA/inhaled corticosteroid (ICS) in a single inhaler device. Brands available are Anoro Ellipta, Trelegy Ellipta and Trimbow. This stage also requires use of pulmonary rehabilitation, long-term oxygen therapy and potentially lung transplantation assessment.

Key factors influencing prescribers are safety, efficacy demonstrated in clinical trials, ease of use of devices, and cost-effectiveness. Brand recognition also plays a role, especially for newly launched products. Prescriber education helps raise awareness about latest treatment guidelines and build confidence in prescribing appropriate medications at each COPD severity level.

COPD treatment focuses on controlling symptoms, preventing flare-ups, and improving quality of life. Management involves a stepwise approach based on disease severity.

For mild COPD, long-acting bronchodilators as maintenance therapy are recommended. Common options include Spiriva (tiotropium) and Stiolto Respimat (olodaterol/tiotropium). These single-inhaler combinations provide 24-hour bronchodilation with once-daily dosing for better adherence.

Moderate COPD adds an inhaled corticosteroid (ICS) to reduce flare-ups. Common combinations are Dulera (mometasone/formoterol) and Breo Ellipta (fluticasone/vilanterol). ICS is preferred over increasing bronchodilator doses to reduce side effects.

For severe COPD, dual bronchodilation is preferred via triple therapies combining an ICS, long-acting beta-agonist (LABA), and long-acting muscarinic antagonist (LAMA). Trelegy Ellipta (fluticasone/umeclidinium/vilanterol) and Trimbow (beclomethasone/glycopyrronium/formoterol) meet Global Initiative for Chronic Obstructive Lung Disease (GOLD) guidelines by addressing multiple airway issues.

In very severe COPD, non-pharmacological therapies like pulmonary rehabilitation and oxygen therapy supplement drug regimens. For symptomatic patients who remain breathless or have recurring flare-ups despite other treatments, roflumilast (Daliresp) or theophylline may provide modest additional benefits.

Key winning strategies adopted by key players of Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market

Product Innovation: Developing innovative products for accurate COPD diagnosis has been a winning strategy. In 2020, Philips launched the Lumify portable ultrasound with IntelliSpace Lung Analysis, which uses AI to help physicians diagnose and monitor COPD. It analyzes lung scans and provides quantitative metrics of disease severity.

Strategic Partnerships: Partnerships with pharma/biotech firms help gain early access to new drugs and diagnostic tests in development. In 2019, Koninklijke Philips partnered with Boehringer Ingelheim and Lung Therapeutics to develop an AI-powered digital solution integrated with medications to better manage COPD patients. Such partnerships provide competitive advantage by offering more comprehensive care.

Geographic Expansion: Expanding into high-growth emerging markets increases customer base. For example, ResMed entered China in 2015 - a massive undiagnosed COPD market. It partnered with local hospitals to deploy diagnostic devices and educate physicians on International Guidelines. By 2018, ResMed captured 15% of the Chinese market due to early mover advantage in a largely untapped region.

Mergers & Acquisitions: Acquisitions complement product portfolios and strengthen regional presence. In 2021, Heineken entered the at-home spirometry market through the acquisition of Propeller Health, strengthening its position in digital solutions for COPD diagnosis and management. Such acquisitions consolidate market share through an increased total addressable market.

Segmental Analysis of Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market

Insights, By Diagnosis Method: Convenience and Accuracy Drive Clinical Assessment Segment

In terms of diagnosis method, clinical assessment segment contributes the highest share of the chronic obstructive pulmonary disease (COPD) diagnosis market owning to its convenience and high accuracy in COPD diagnosis. Clinical assessment involves a doctor examining the patient's medical history, performing a physical examination and respiration tests like checking pulse oximetry. This method is the most economical and accessible approach for initial COPD screening and diagnosing the severity at an early stage.

Clinical assessment allows doctors to listen to the sounds of breathing with a stethoscope and observe physical symptoms like breathlessness. Chest auscultation during clinical assessment is a quick and inexpensive way to detect abnormal breathing patterns caused by COPD. Doctors can also feel the chest for abnormally increased work of breathing. Clinical assessment enables doctors to look for tell-tale signs of COPD like finger clubbing, barrel chest and use of auxiliary muscles during respiration.

The non-invasive nature along with the ability to perform serial tests for monitoring disease progression has cemented clinical assessment's role as a reliable and preferred diagnostic method for COPD. Its high success rate in correctly identifying patients suitable for advanced tests further drives its maximum usage over other diagnostic approaches.

Insights, By Severity-based Diagnosis: Standardized Classification Drives GOLD Segment

In terms of severity-based diagnosis, GOLD 1–4 classification contributes the highest share of the chronic obstructive pulmonary disease (COPD) diagnosis market owing to its widespread global adoption as the standardized system for classifying COPD severity. The GOLD classification is recommended by all major respiratory health organizations and provides an objective scale to grade a COPD patient's severity based on lung function tests.

The GOLD system grades COPD into four easily recognizable stages from mild to very severe (GOLD 1 to 4) based on spirometric assessment of airflow limitation using the forced expiratory volume in 1 second (FEV1) and FEV1/forced vital capacity ratio. The GOLD scoring is purely functional and objective without factoring symptoms, exacerbation history or co-morbidities. This prevents subjective interpretation and maintains consistency. For instance, inhaled corticosteroids may be recommended for patients with GOLD classification of 3 and above. The standardized grouping of patients clinically proved to result in optimal airflow and quality of life benefits from the assigned treatment.

Widespread incorporation of the GOLD classification system with evidence-based treatment pathways in clinical practice guidelines has boosted its utilization over other non-functional severity scoring methods. Its high reliability and reproducibility in COPD management on a global scale explains GOLD staging’s commanding share of the severity-based diagnosis market segment.

Insights, By Molecule Type: Target Specificity Drives Monoclonal Antibody Segment

In terms of molecule type, monoclonal antibody contributes the highest share of the chronic obstructive pulmonary disease (COPD) diagnosis market owing to its unparalleled target specificity and precision in COPD diagnosis and assessment of disease progression. Their unique single antigen specificity allows binding only to the designated target molecule linked to COPD pathology. For instance, monoclonal antibodies are being developed that only recognize inflammatory biomarkers precisely correlating to COPD severity stages. Such biomarker-targeted antibodies facilitate highly selective non-invasive liquid biopsy tests for COPD from blood or urine samples.

The high affinity and selectivity of monoclonal antibody-based assays enable reliable detection of even minute changes in biomarker expression levels associated with subtle disease modifications. This superior sensitivity aids in early detection of COPD, predicting risk of exacerbations, determining treatment effectiveness as well as prognosis through serial biomarker quantification.

Additionally, monoclonal antibodies show negligible cross-reactivity with other molecules, reducing false positives. Engineering antibodies against novel proteomic signatures of COPD endotypes promises optimized personalized treatment selection and monitoring through specific biomarker profiling.

Their uniform batch-to-batch reproducibility assists large-scale clinical adoption and real-world effectiveness with consistent results. These advantages have established monoclonal antibody diagnostics as an ascending segment compared to other non-specific COPD investigational molecules. Continued monoclonal antibody development is expected to transform COPD management.

Additional Insights of Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market

The prevalence of COPD is highest among individuals aged 55-64 years in the U.S. due to smoking and environmental factors.

GOLD 2 classification had the most diagnosed cases in the EU4 countries and the UK, indicating moderate airflow limitation.

COPD prevalence in the U.S.: Approximately 18.5 million cases in 2023.

COPD prevalence in Japan: Around 0.9 million cases, with a notable increase expected by 2034.

Competitive overview of Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market

The major players operating in the Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market include GlaxoSmithKline (GSK), AstraZeneca, Boehringer Ingelheim, Novartis, Teva Pharmaceuticals, Pfizer, Merck, Sanofi, Mylan, and Sun Pharmaceutical Industries.

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Chronic Obstructive Pulmonary Disease (COPD) Diagnosis Market

In August 2024, GlaxoSmithKline announced the launch of a new inhaler targeting COPD exacerbations, aiming to reduce the overall burden on healthcare systems. The company highlights its ongoing efforts in developing inhalers for COPD, including the progression of trials for new or improved versions of existing inhalers such as the low-carbon Ventolin inhaler.

In May 2024, AstraZeneca collaborated with a tech company to integrate AI-driven diagnostics for COPD, enhancing early detection and management. Sources also identify AI-driven collaborations involving AstraZeneca, including partnerships with companies like Illumina and Absci.

In February 2024, Boehringer Ingelheim expanded its clinical trials to include a new COPD drug showing promise in reducing exacerbation rates in severe cases. Boehringer Ingelheim's ongoing research in respiratory diseases, including COPD, and various clinical trials in different stages is also getting attention in the chronic obstructive pulmonary disease (COPD) diagnosis market.

Would you like to explore the option of buying individual sections of this report?

About author

Manisha Vibhuteis a consultant with over 5 years of experience in market research and consulting. With a strong understanding of market dynamics, Manisha assists clients in developing effective market access strategies. She helps medical device companies navigate pricing, reimbursement, and regulatory pathways to ensure successful product launches.

Frequently Asked Questions :

How big is the chronic obstructive pulmonary disease (COPD) diagnosis market?

The chronic obstructive pulmonary disease (COPD) diagnosis market is estimated to be valued at USD 2.29 billion in 2025 and is expected to reach USD 3.24 billion by 2032.

What are the key factors hampering the growth of the chronic obstructive pulmonary disease (COPD) diagnosis market?

The high cost of treatment and limited access to advanced therapies and complex pathophysiology leading to varied disease management challenges are the major factors hampering the growth of the chronic obstructive pulmonary disease (COPD) diagnosis market.

What are the major factors driving the chronic obstructive pulmonary disease (COPD) diagnosis market growth?

The increasing prevalence of smoking and environmental pollutants, and growing awareness about improved diagnostics for COPD are the major factors driving the chronic obstructive pulmonary disease (COPD) diagnosis market.

Which is the leading diagnosis method in the chronic obstructive pulmonary disease (COPD) diagnosis market?

The leading diagnosis method segment is clinical assessment.

Which are the major players operating in the chronic obstructive pulmonary disease (COPD) diagnosis market?

GlaxoSmithKline (GSK), AstraZeneca, Boehringer Ingelheim, Novartis, Teva Pharmaceuticals, Pfizer, Merck, Sanofi, Mylan, and Sun Pharmaceutical Industries are the major players.

What will be the CAGR of the chronic obstructive pulmonary disease (COPD) diagnosis market?

The CAGR of the chronic obstructive pulmonary disease (COPD) diagnosis market is projected to be 5.1% from 2025 to 2032.

Missing comfort of reading report in your local language? Find your preferred language :

-diagnosis-market-by-diagnosis-method.png) Insights, By Diagnosis Method: Convenience and Accuracy Drive Clinical Assessment Segment

Insights, By Diagnosis Method: Convenience and Accuracy Drive Clinical Assessment Segment-diagnosis-market-by-severity-based-diagnosis.png)