Inboard Engines Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Inboard Engines Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Inboard Engines Market is segmented By Product (Diesel, Gasoline, Electric, Others), By Power (Low, Medium, High), By Ignition (Electric, Manual), By Engine (IC Engine, Two-stroke, Four-stroke, Electric Engine), By Geography (North America, Latin America, Asia Pacific, Europe, Middle East, and Africa). The report offers the value (in USD billion) for the above-mentioned segments.

Inboard Engines Market is segmented By Product (Diesel, Gasoline, Electric, Others), By Power (Low, ...

Inboard Engines Market Size - Analysis

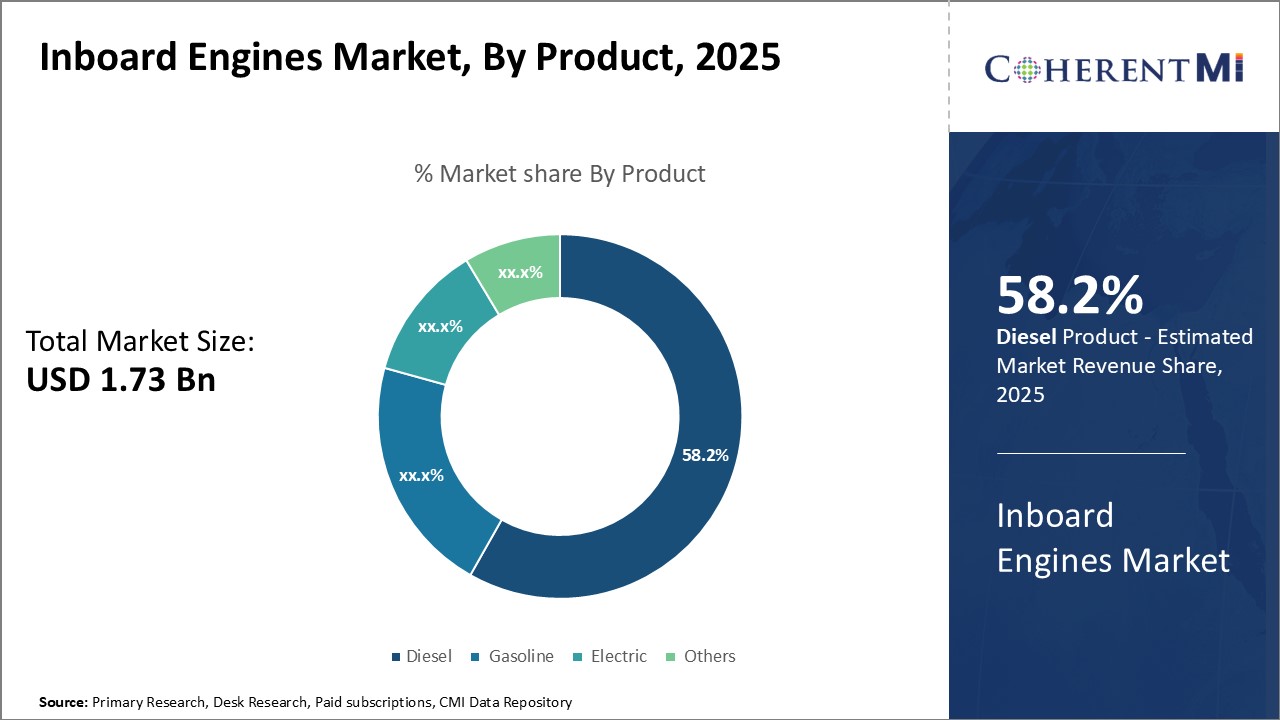

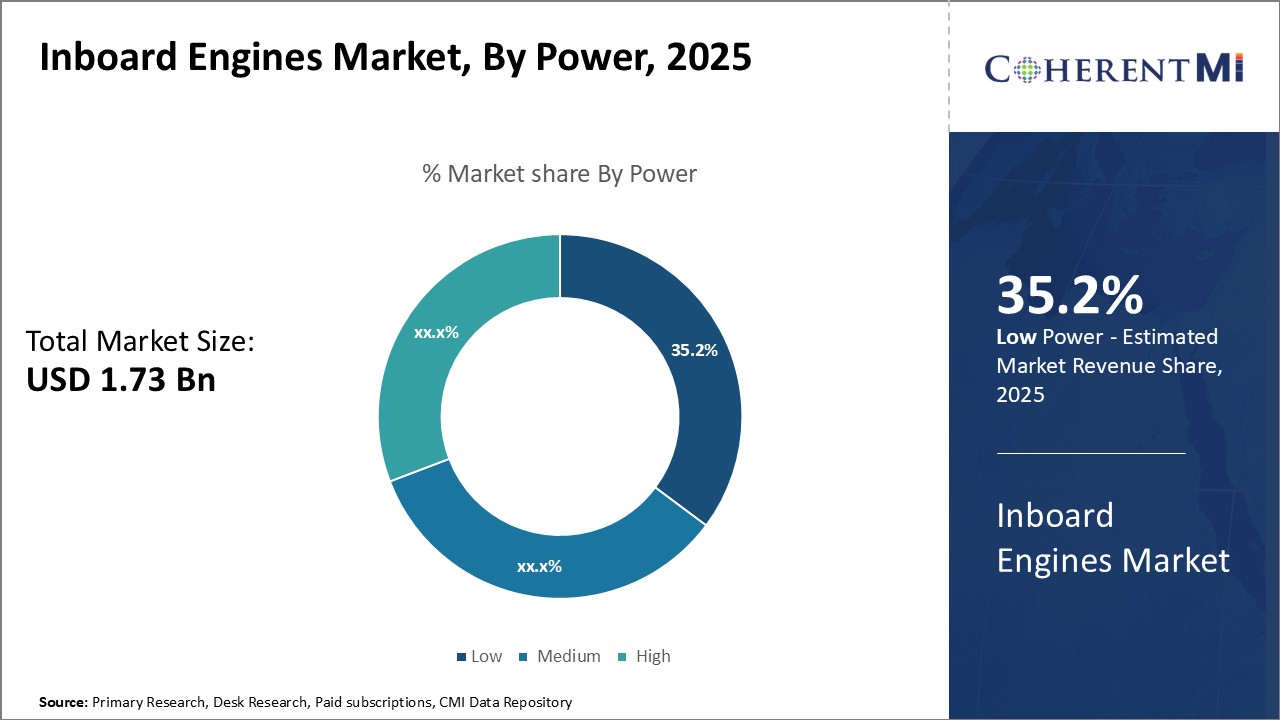

The Global Inboard Engines Market is estimated to be valued at USD 1.73 Bn in 2025 and is expected to reach USD 2.71 Bn by 2032, growing at a compound annual growth rate (CAGR) of 6.6% from 2025 to 2032. The rising marine tourism and water sports industry along with increasing disposable income is driving the demand for inboard engines globally. Development of fuel-efficient and low emission engines by manufacturers continues to support the market growth over the forecast period.

The market is witnessing rising demand for electric and hybrid inboard engines driven by stringent environmental regulations regarding emissions. Manufacturers are investing in developing advanced lithium-ion battery technologies to increase the performance and operational capabilities of electric inboard engines. Additionally, the adoption of connected engine technologies integrated with IoT and advanced analytics is emerging as a key trend in the market.

Market Size in USD Bn

CAGR6.6%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

6.6%

Market Concentration

Low

Major Players

Caterpillar Inc., Cummins Inc., Volvo Penta, Yanmar Co., Ltd., Mercury Marine and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

Inboard Engines Market Trends

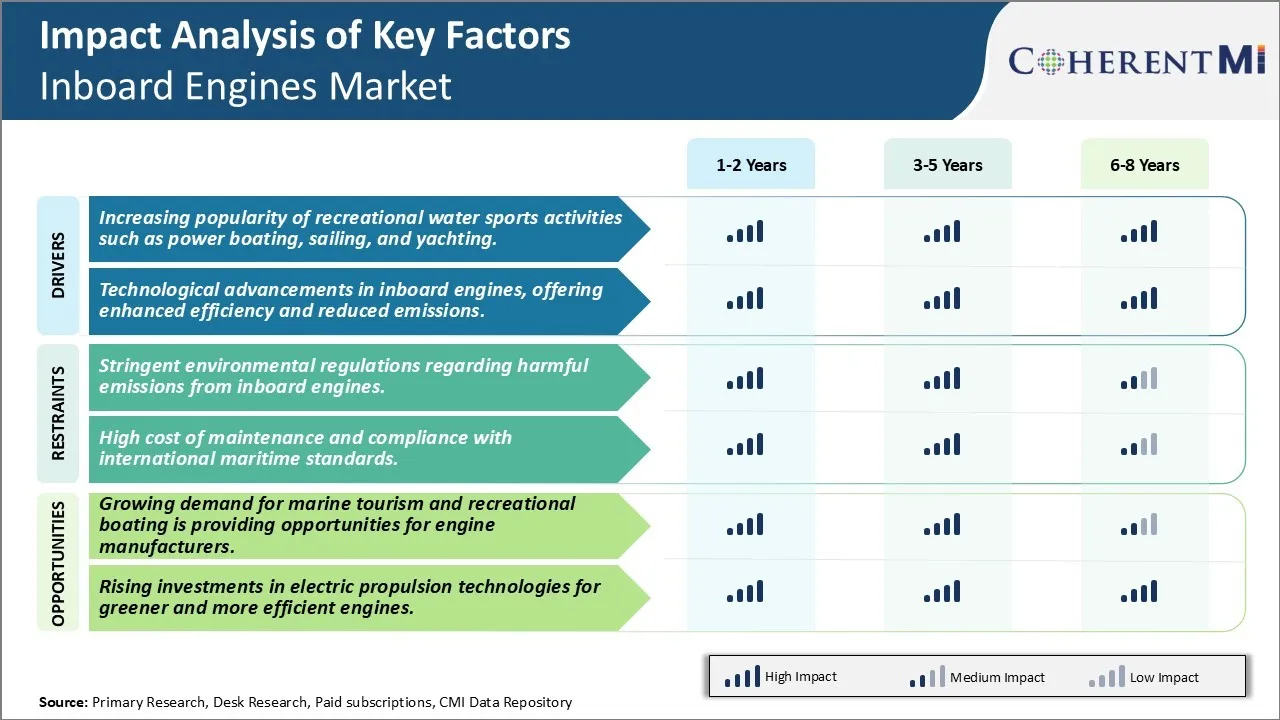

Market Driver - Increasing Popularity of Recreational Water Sports Activities Such as Power Boating, Sailing, And Yachting

The popularity of recreational water sports activities has been steadily growing over the past few years. More and more people across regions are taking interest in activities like power boating, sailing, and yachting. Power boating allows speed enthusiasts to experience the thrill of zooming over waters whilst soaking in breathtaking scenic coastlines or lakesides. It is a great way for friends and families to spend quality time together outdoors. Sailing provides the unique joy of navigating sails and feeling one with the winds while enjoying nature's bounty. For those seeking luxury and comfort, yachting has become the means to enjoy onboard amenities like a galley, cabins and Jacuzzi in a rejuvenating ambience surrounded by beautiful water bodies.

As recreational appeal rises, boat and yacht manufacturers are witnessing growing demand. Customers prefer modern and high-performance boats fitted with powerful yet quiet and smooth inboard engines. Many coastal regions have also developed boating infrastructure like marinas and boat repair shops which cater to the requirements of boat owners. Local governments recognize water sports’ potential to boost tourism and are promoting activities through water sport festivals and competitive sailing/powerboat events. With greater affordability due to steady economic growth and expanding middle class segments, more individuals now consider boating, sailing or yachting as worthy leisure pursuits and investments. The number of boats and yachts on waters consequently keeps mounting year-on-year. This upward trend in recreational water sports engagement directly fuels the need for inboard engines to power the expanding boat/yacht fleet.

Market Driver - Technological Advancements in Inboard Engines to Boost Market Growth

Inboard engine manufacturers have constantly strived to innovate and address evolving customer needs and regulatory requirements. Advancements in technology have allowed development of highly efficient yet eco-friendly inboard engines. Engine designers have diligently worked on optimizing combustion, thermal management and friction reduction within engines. The use of electronic fuel injection, direct injection systems and efficient cooling designs have significantly increased fuel efficiency of inboard engines. Computer-controlled monitoring of various engine parameters further aids in extracting maximum performance while maintaining low emissions and vibrations.

Engine makers have also transitioned to cleaner burning fuels. The introduction of diesel-powered inboard engines provided an eco-friendly alternative to traditional gasoline engines owing to diesel’s higher-octane rating and combustion efficiency. Latest engine varieties meet stringent EPA standards on carbon emissions and are capable of achieving 50% more miles to the gallon than older engines. Further extending this quest, manufacturers have progressively forayed into natural gas and hybrid propulsion systems. The ongoing R&D for battery-operated electric inboard engines is paving way for near-zero local emissions on water. The tangible environmental benefits of novel technologies are appealing to an increasingly sustainability-conscious global audience. Continuous innovations in material, design and alternative fuel technologies by inboard engine brands aim to deliver enhanced vessel experience alongside reduced total cost of ownership for extended periods.

One of the major challenges currently faced by the inboard engines market is stringent environmental regulations imposed by various regulatory bodies around the world regarding harmful emissions. In recent years, environmental concerns regarding air and water pollution caused by emissions from gasoline and diesel inboard engines used in boats and ships have been increasing significantly. Various gases such as carbon monoxide, nitrogen oxides, particulate matter and other greenhouse gases emitted from these engines are considered harmful for both air and water quality.

To curb emissions, regulatory authorities in many countries and regions have implemented increasingly stringent emission norms and regulations for inboard engines. For example, the EPA (Environmental Protection Agency) in the US has mandated significant cuts in permissible emission levels of particulate matter, hydrocarbons and nitrogen oxides under its EPA Tier standards. Similar tough emission regulations have been put forth by other bodies such as the EU and the International Maritime Organization (IMO). Complying with these regulations has proved to be challenging for many engine manufacturers due to technology limitations and high compliance costs. The frequent changes in emission norms have also increased R&D expenditures for companies.

Market Opportunity: Growing Demand for Marine Tourism and Recreational Boating is Providing Opportunities for Engine Manufacturers

One major opportunity in the inboard engines market is presented by the rising global popularity of marine tourism and recreational boating activities. In recent years, marine tourism involving activities such as sailing, yachting, cruise travels and ferry rides has witnessed strong growth in several developed and emerging economies. This has coincided with rising discretionary incomes and spending power of people in these markets. Additionally, recreational boating has gained widespread acceptance as a popular water sport and leisure activity. The growing enthusiasm for boating is visible from increasing sales of a variety of recreational boats including motorboats and yachts across the world.

The surge in marine touring and boating is translating into strong demand for marine engines required to power these boats and vessels. Both gasoline-powered and diesel engine manufacturers are benefiting from this trend. The demand encompasses a wide range of inboard engine types catering to different boat sizes and applications. Engine OEMs now have substantial opportunities to expand their product lines, improve product features and aggressively target emerging markets experiencing a boom in waterborne activities. Aftermarket and service revenues are also set to rise owing to the large and growing global fleet of inboard engine-operated boats and ships.

Key winning strategies adopted by key players of Inboard Engines Market

Strategic Alliances: Companies are partnering with boat manufacturers, marine component suppliers, and even electric vehicle (EV) manufacturers to co-develop next-generation engines or integrate advanced components that enhance performance.

Technological Collaborations: Some inboard engine manufacturers collaborate with technology firms to enhance engine management systems, software controls, and connectivity solutions (e.g., IoT for real-time engine monitoring).

Hybrid and Electric Propulsion Systems: With the growing focus on sustainability and reducing carbon emissions, companies are investing heavily in developing hybrid and fully electric inboard engines. These technologies aim to meet future emission regulations and appeal to environmentally conscious consumers.

Advanced Engine Control Systems: Integrating smart technologies like electronic fuel injection (EFI), digital throttle control, and GPS-based performance optimization to improve engine efficiency, reduce fuel consumption, and provide better control to operators.

Compliance with Environmental Regulations: Many inboard engine manufacturers are focusing on producing engines that comply with stringent emission standards like the U.S. Environmental Protection Agency (EPA) Tier 3 and European Union (EU) Stage V regulations. This involves reducing engine noise, vibration, and emissions.

Focus on Alternative Fuels: There’s growing interest in engines that can operate on alternative fuels like biofuels or LNG (liquefied natural gas) to further reduce the environmental impact of marine engines.

Segmental Analysis of Inboard Engines Market

Insights, By Product, Fuel Efficiency Drives Diesel's Dominance in the Forecast Period

By Product, diesel engines are expected to contribute 58.2% market share in 2025 due to their reputation for superior fuel efficiency compared to gasoline engines. Diesel fuel contains more energy than an equivalent amount of gasoline, allowing diesel engines to extract more work from each unit of fuel consumed. This translates directly to lower operating costs over the lifetime of the engine. For commercial operators and recreational enthusiasts alike, reducing fuel expenditures is a key factor when selecting an inboard engine.

Diesel engines also benefit from simple and robust construction that requires less frequent and less expensive maintenance than gasoline engines. Their heavier duty designs stand up well to continuous running in demanding commercial applications. Recreational boat owners appreciate diesel's strong torque output for tasks like towing water toys or pulling up to docks in crowded marinas. Reliability is paramount when safety depends on the engine.

Although diesel engines carry a higher initial purchase price versus gasoline, total lifetime costs are lower due to fuel savings and less maintenance. This ROI calculation is persuasive for commercial operators running their boats daily. Recent efficiency gains have closed the price gap for recreational users as well, broadening diesel's appeal beyond workboats into luxury yachts and houseboats. Stringent emissions regulations are driving diesel technology toward even cleaner burning fuels and aftertreatment systems to expand the user base further. Overall superior efficiency and reliability compared to alternatives drive diesel's market leading position.

Insights, By Power, Compact Design Attracts Recreational Boat Owners to Low Power Engines

In terms of power, the Low power segment is expected to account for 35.2% market share in 2025. This is largely due to demand from recreational boat owners seeking compact engines that maximize usable space aboard smaller watercraft. Low power engines produce less than 100 horsepower, allowing installation into shallow bilges and cramped engine compartments. Their smaller footprints leave more room onboard for comfortable seating, storage, and amenities like retractable bimini tops.

Low power engines also suit casual boaters seeking relaxed pleasure rides rather than top speed. Their reduced weight compared to higher power options means less stress on hull structures and trailer components when the boat is out of the water. Installation and maintenance costs tend to be lower as well for these lighter duty designs. Safety is an additional factor, as less powerful engines pose less risk of accidental acceleration if controls are unintentionally engaged during boarding or docking maneuvers.

Overall, compact sizing and weight along with suitability for low-key recreational use drives the outsized market presence of low power inboard engines. Their flexibility opens boating to owners of small craft who desire the benefits of inboard propulsion without compromising valuable onboard space or budgets. Ease of operation further broadens the potential buyer base.

Insights, By Ignition Type, Integrated Design Increases Electric Ignition's Share

When segmented by ignition type, electric ignition commands the leading market share due to its seamless integration within engine control systems. Advancing electronics have placed sophisticated engine management capabilities directly into electric ignitions via programmable engine control modules (ECMs). These intelligent systems optimize ignition timing, analyze sensor feedback, and make real-time adjustments to maintain optimal power, efficiency and emissions performance under all operating conditions.

Integrated ignitions simplify installation versus manual setups as spark parameters are factory pre-programmed by engine manufacturers. No field adjustments are required to start or run the engine. Troubleshooting is also eased through direct monitoring and diagnostic codes accessible via onboard diagnostics ports. Sensors can detect impending issues for timely repairs before costly failures occur.

Environmentally, electric ignitions emit no open sparks that could ignite fuel vapors as engines and onboard fuel tanks heat up in hot weather. Spark quenching further reduces emissions through precise spark termination. Reliability is another advantage thanks to ECM management preventing misfires even under load. Overall, electric ignition's seamless integration into engine control architecture streamlines installation and maintenance while optimizing performance safety and environmental impact. This drives market dominance over manual setups now nearing obsolescence in commercial and recreational inboard applications alike.

Additional Insights of Inboard Engines Market

The global inboard engines market is projected to grow steadily over the next decade due to advancements in engine technology, increasing demand for water sports, and the rising trend of marine tourism. Diesel engines continue to dominate the market due to their high-power output and long lifespan, although electric engines are gaining traction for their eco-friendliness and quieter operation. Companies like Volvo Penta and Cummins are leading the charge in innovation, focusing on developing engines that meet stricter emission regulations while offering superior performance. The market is expected to witness substantial growth in Asia Pacific and North America, where maritime industries are expanding. However, environmental concerns and legal requirements for emission controls could challenge market growth. Still, the market presents significant opportunities for manufacturers, particularly with the rising demand for electric propulsion systems and the increase in recreational boating activities globally.

Competitive overview of Inboard Engines Market

The major players operating in the Inboard Engines Market include Caterpillar Inc., Cummins Inc., Volvo Penta, Yanmar Co., Ltd., Mercury Marine, Ilmor Engineering, Inc., MAN Energy Solutions, MTU Friedrichshafen GmbH, Indmar Marine Engine, Suzuki Motor Corporation, Nanni Industries, PCM (Pleasurecraft Marine Engine Co.), Scania AB and Yamaha Motor Co., Ltd.

Inboard Engines Market Leaders

Caterpillar Inc.

Cummins Inc.

Volvo Penta

Yanmar Co., Ltd.

Mercury Marine

*Disclaimer: Major players are listed in no particular order.

Inboard Engines Market - Competitive Rivalry

Inboard Engines Market

Market Consolidated (Dominated by major players)

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Inboard Engines Market

In November 2023, Evoy released a new electric inboard engine, enhancing the market for electric propulsion systems in the marine sector. The engine promises quieter operations and reduced emissions, making it a favorable choice for recreational boaters.

In February 2023, Volvo Penta teamed up with Southport Boats to release a new version of the Southport 30 FE with Volvo Penta’s pleasure landing system, offering enhanced control and versatility.

In August 2022, Cummins Inc. completed the acquisition of Meritor, advancing the development of energy-efficient propulsion systems. This acquisition is expected to broaden Cummins’ product offerings in the marine industry.

Inboard Engines Market Report - Table of Contents

RESEARCH OBJECTIVES AND ASSUMPTIONS

Research Objectives

Assumptions

Abbreviations

MARKET PURVIEW

Report Description

Market Definition and Scope

Executive Summary

Inboard Engines Market, By Product

Inboard Engines Market, By Power

Inboard Engines Market, By Ignition

Inboard Engines Market, By Engine

Coherent Opportunity Map (COM)

MARKET DYNAMICS, REGULATIONS, AND TRENDS ANALYSIS

Market Dynamics

Impact Analysis

Key Highlights

Regulatory Scenario

Product Launches/Approvals

PEST Analysis

PORTER’s Analysis

Merger and Acquisition Scenario

Global Inboard Engines Market, By Product, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Global Inboard Engines Market, By Power, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Global Inboard Engines Market, By Ignition, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Global Inboard Engines Market, By Engine, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Global Inboard Engines Market, By Region, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Product, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Power, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Ignition, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Engine, 2020-2032, Value (USD Bn)

U.S.

Canada

Latin America

Introduction

Market Size and Forecast, By Product, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Power, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Ignition, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Engine, 2020-2032, Value (USD Bn)

Brazil

Argentina

Mexico

Rest of Latin America

Europe

Introduction

Market Size and Forecast, By Product, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Power, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Ignition, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Engine, 2020-2032, Value (USD Bn)

Germany

U.K.

Spain

France

Italy

Russia

Rest of Europe

Asia Pacific

Introduction

Market Size and Forecast, By Product, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Power, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Ignition, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Engine, 2020-2032, Value (USD Bn)

China

India

Japan

Australia

South Korea

ASEAN

Rest of Asia Pacific

Middle East

Introduction

Market Size and Forecast, By Product, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Power, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Ignition, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Engine, 2020-2032, Value (USD Bn)

GCC Countries

Israel

Rest of Middle East

Africa

Introduction

Market Size and Forecast, By Product, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Power, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Ignition, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Engine, 2020-2032, Value (USD Bn)

South Africa

North Africa

Central Africa

COMPETITIVE LANDSCAPE

Caterpillar Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Cummins Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Volvo Penta

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Yanmar Co., Ltd.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Mercury Marine

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Ilmor Engineering, Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

MAN Energy Solutions

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

MTU Friedrichshafen GmbH

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Indmar Marine Engine

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Suzuki Motor Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Nanni Industries

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

PCM (Pleasurecraft Marine Engine Co.)

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Scania AB

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Yamaha Motor Co., Ltd.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analyst Recommendations

Wheel of Fortune

Analyst View

Coherent Opportunity Map

References and Research Methodology

References

Research Methodology

About us

Inboard Engines Market Segmentation

By Product

Diesel

Gasoline

Electric

Others

By Power

Low

Medium

High

By Ignition

Electric

Manual

By Engine

IC Engine

Two-stroke

Four-stroke

Electric Engine

Would you like to explore the option of buying individual sections of this report?

About author

Suraj Bhanudas Jagtap is a seasoned Senior Management Consultant with over 7 years of experience. He has served Fortune 500 companies and startups, helping clients with cross broader expansion and market entry access strategies. He has played significant role in offering strategic viewpoints and actionable insights for various client’s projects including demand analysis, and competitive analysis, identifying right channel partner among others.

Frequently Asked Questions :

How Big is the Inboard Engines Market?

The Global Inboard Engines Market is estimated to be valued at USD 1.73 Bn in 2025 and is expected to reach USD 2.71 Bn by 2032.

What will be the CAGR of the Inboard Engines Market?

The CAGR of the Inboard Engines Market is projected to be 6.4% from 2024-2031.

What are the major factors driving the Inboard Engines Market growth?

The increasing popularity of recreational water sports activities such as power boating, sailing, and yachting, and technological advancements in inboard engines, offering enhanced efficiency and reduced emissions are the major factors driving the Inboard Engines Market.

What are the key factors hampering the growth of the Inboard Engines Market?

The stringent environmental regulations regarding harmful emissions from inboard engines and the high cost of maintenance and compliance with international maritime standards, are the major factors hampering the growth of the Inboard Engines Market.

Which is the leading Product in the Inboard Engines Market?

Diesel is the leading Product segment.

Which are the major players operating in the Inboard Engines Market?

Caterpillar Inc., Cummins Inc., Volvo Penta, Yanmar Co., Ltd., Mercury Marine, Ilmor Engineering, Inc., MAN Energy Solutions, MTU Friedrichshafen GmbH, Indmar Marine Engine, Suzuki Motor Corporation, Nanni Industries, PCM (Pleasurecraft Marine Engine Co.), Scania AB, Yamaha Motor Co., Ltd. are the major players.

Missing comfort of reading report in your local language? Find your preferred language :

Insights, By Power, Compact Design Attracts Recreational Boat Owners to Low Power Engines

Insights, By Power, Compact Design Attracts Recreational Boat Owners to Low Power Engines