Shared Vehicles Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Shared Vehicles Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Shared Vehicles Market is segmented By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles), By Application (Body Structure, Suspension, Power Train, Others), By Steel Type (High-Strength Steel (HSS), Advanced High-Strength Steel (AHSS), Ultra High-Strength Steel (UHSS), Mild Steel), By Geography (North America, Latin America, Asia Pacific, Europe, Middle East, and Africa). The report offers the value (in USD billion) for the above-mentioned.

Shared Vehicles Market is segmented By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, ...

Shared Vehicles Market Size - Analysis

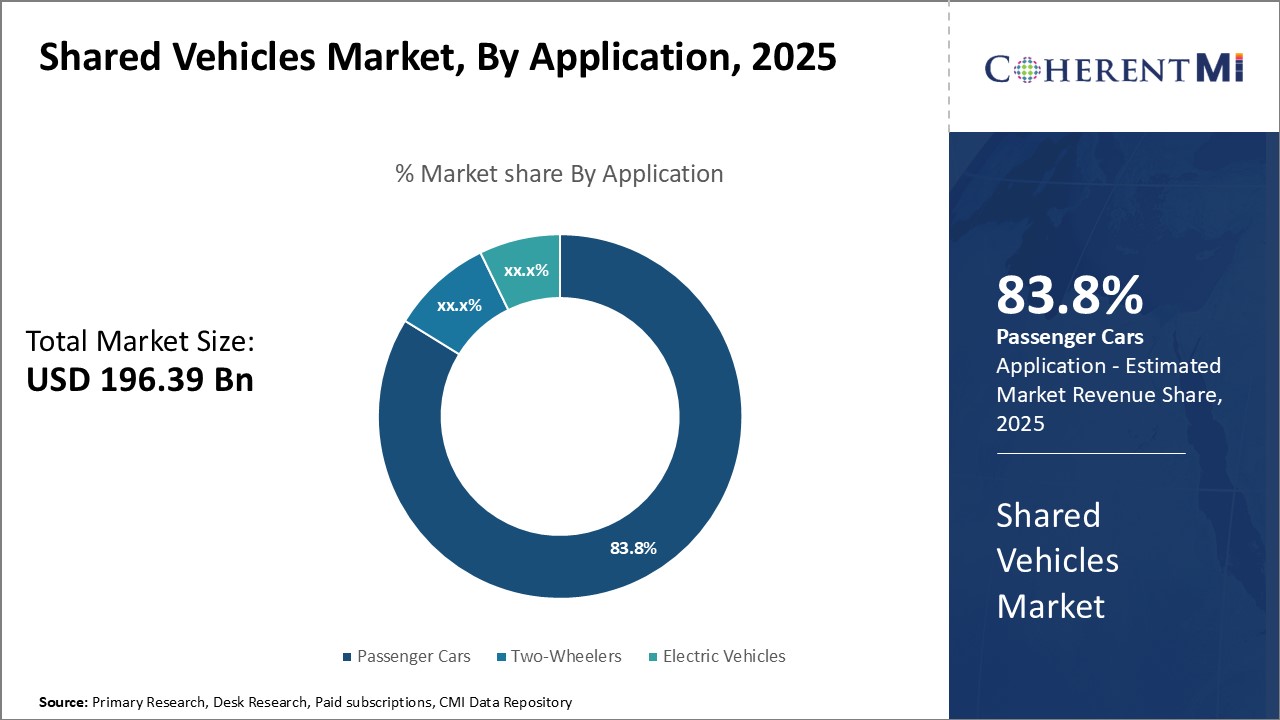

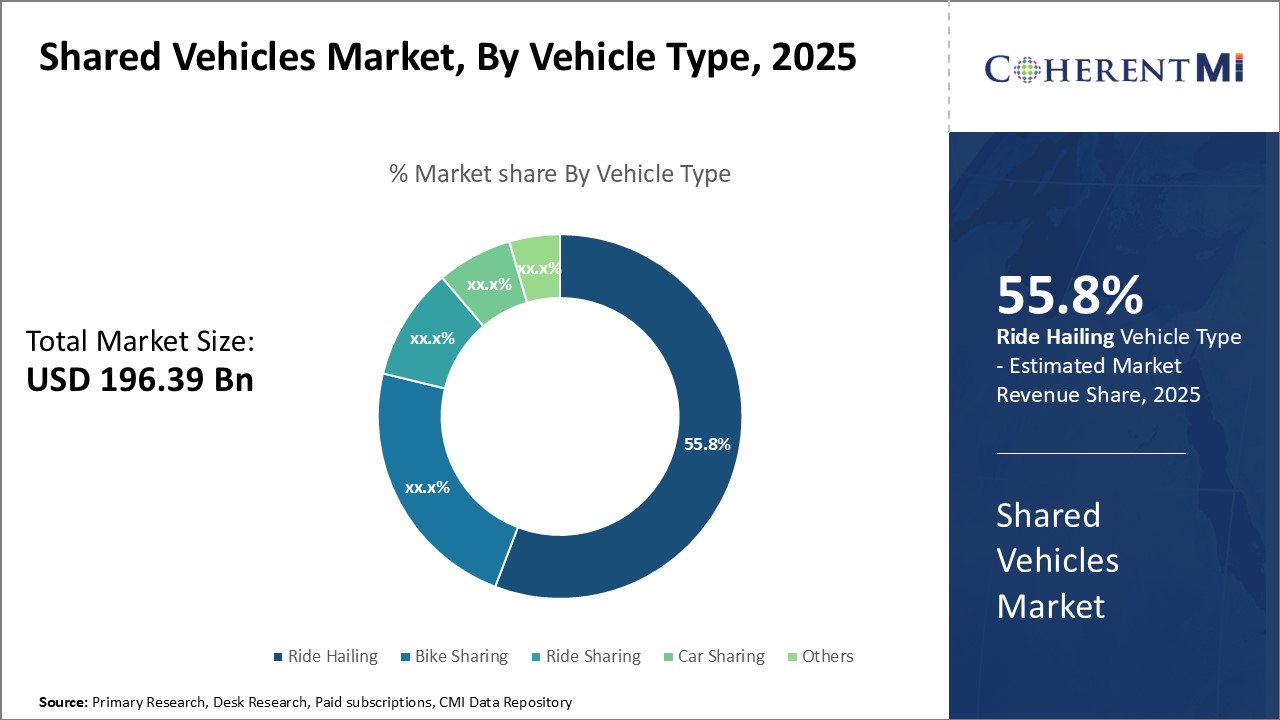

The shared vehicles market is estimated to be valued at USD 196.39 Bn in 2025 and is expected to reach USD 519.23 Bn by 2032, growing at a compound annual growth rate (CAGR) of 14.9% from 2025 to 2032. The shared vehicles market is expected to witness significant growth with rising fuel costs and concerns around emissions.

Market Size in USD Bn

CAGR14.9%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

14.9%

Market Concentration

Medium

Major Players

Daimler AG, SIXT SE, Avis Budget Group Inc., Hertz Global Holdings, Inc., Europcar Mobility Group SA and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

Shared Vehicles Market Trends

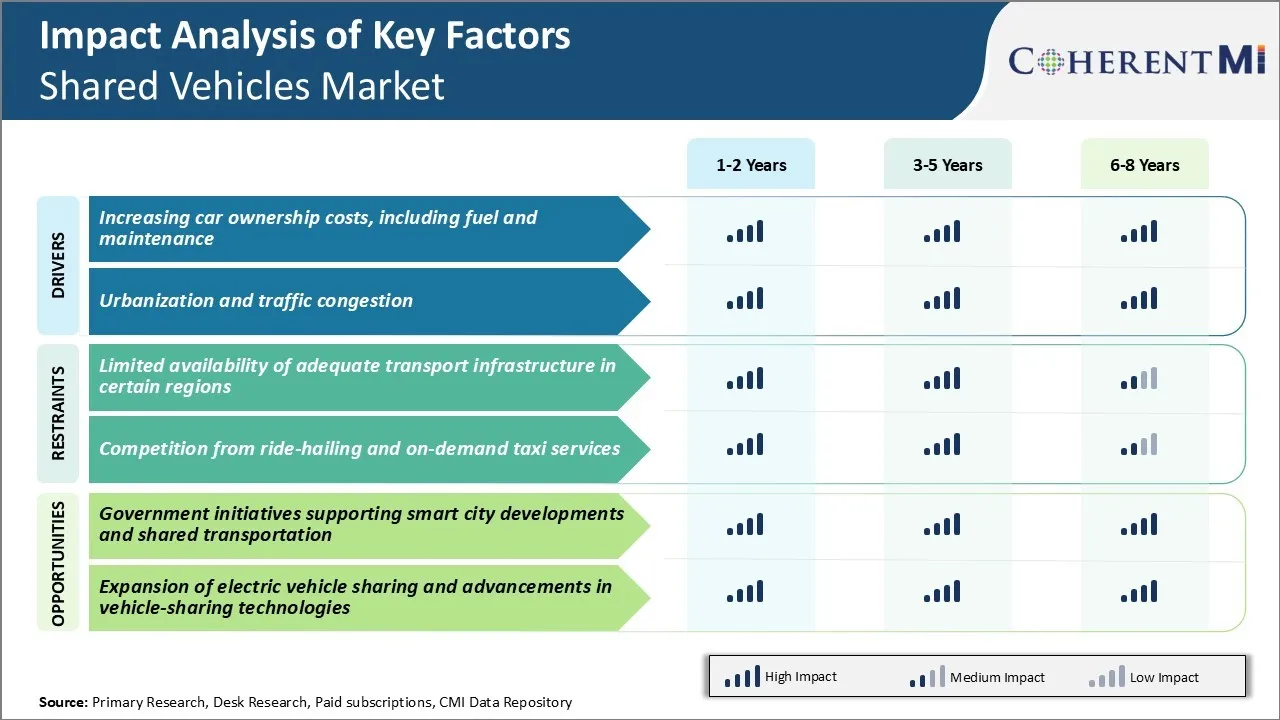

Market Driver - Increasing Car Ownership Costs, Including Fuel and Maintenance

The cost of car ownership has been steadily rising over the past decade. Shared vehicles provide one such alternative. By enabling easy access to vehicles without the long-term commitment of ownership, users can avoid taking on large repair bills or dealing with rising fuel costs. Individual trips that may not otherwise be feasible or affordable can be completed via a cost-effective shared option.

For families in particular, the ability to share one vehicle among household members and only pay for actual time of use can significantly reduce annual car-related spending and free up disposable income for other priorities.

Shared mobility space will continue expanding its customer base as economically-minded consumers increasingly view individual car purchases as an unnecessary burden. With new digital platforms constantly improving user experience and expanding service coverage areas, these models are poised to fulfill transportation needs. Need for keeping ownership costs in check for a growing segment of the population will continue to grow shared vehicles market.

Market Driver - Urbanization and Congestion

Rapid urbanization trends have led to population density levels not seen before in major cities worldwide. As more people flock to urban centers for employment and lifestyle opportunities, municipal infrastructure struggles to keep pace. A direct result is worsening road congestion that reduces mobility and drags down productivity.

By enabling higher vehicle occupancy and optimizing utilization of each vehicle on the road, services like ride-hailing take commuters off crowded trains and buses as well as reducing the number of single-occupant vehicles contributing to congestion. Studies have shown ride-sharing, bike rentals, and carpooling access near transit hubs can lower dependency on personal cars for short inner-city trips.

With digitally optimized fleets and dynamic pricing, shared vehicles also redistribute traffic more evenly throughout the day instead of everyone trying to use their own car simultaneously during rush hour. For dense and fast-growing cities, implementing shared mobility at scale provides a way to both sustain high economic activity levels while keeping roads fluid for the movement of people and goods.

Market Challenge - Limited Availability of Adequate Transport Infrastructure in Certain Regions

One of the key challenges faced by the shared vehicles market is the limited availability of adequate transport infrastructure in certain regions across the world. While major cities in developed markets have fairly well-established roads, public transport systems and supporting infrastructure, the same cannot be said for several developing and underdeveloped areas.

The lack of proper roads, limited road connectivity between locations, absence of dedicated lanes for shared mobility and insufficient parking infrastructure in many smaller cities and towns pose significant hurdles for companies and operators active in this market. Setting up a robust shared mobility network requires reliable infrastructure that can facilitate easy navigation as well as efficient pick-up and drop-off of users.

Infrastructure inadequacies can negatively impact the last mile connectivity and user experience, limiting the scope for market expansion beyond major metropolitan areas. Overcoming these infrastructure roadblocks would require substantial time and capital investments from local administrations.

Market Opportunity - Government Initiatives Supporting Smart City Developments and Shared Transportation

One of the prominent opportunities for the shared vehicles market is the rising focus of many governments on smart city developments and initiatives promoting shared transportation systems. In a bid to alleviate traffic congestion levels, several administrations are pushing smart and sustainable mobility solutions. They are formulating enabling policies, introducing regulations and offering incentives to bring shared mobility models to the forefront.

Global trends indicate a definite shift towards integrated multimodal public transport networks with seamless connectivity provided by on-demand shared mobility services. More and more cities are embracing smart city blueprints to emphasize walkability, connected infrastructure, and shared vehicle alternatives.

This will open the doors for Next Generation Mobility companies to expand their footprint and customized offerings. Supportive regulations and investments in digital technologies by governments are facilitating the shared vehicles market growth across global regions.

Key winning strategies adopted by key players of Shared Vehicles Market

Operators like Uber, Lyft, and Ola have successfully adopted the strategy of operational densification to expand their business footprint. For example, as of 2021, Uber has over 1 million driver partners across India.

Another strategy that has paid rich dividends is strategic partnerships. Zipcar entered into partnerships with universities across the US and Canada to position their vehicles within college campuses.

Having a strong technological platform has also been a core winning strategy. Companies like Mobike focused heavily on developing user-friendly apps for seamless rental. Their app features such as live tracking of nearby bikes and easy unlocking mechanisms enhanced customer experience.

Data analytics is another strategy that market leaders have effectively leveraged. Uber collects troves of customer data that helps them optimize operations. For example, they analyze peak demand times and locations to deploy vehicles efficiently.

Bundling services with other transportation modes has emerged as a popular strategy. In China, Didi provides integrated services across ride-hailing, car-rentals and bikes. Their super-app approach provides a one-stop solution to user needs and creates high entry barriers for competition.

Segmental Analysis of Shared Vehicles Market

Insights, By Data Type: Convenience and Accessibility Drive the Growth of Ride Hailing

In terms of data type, ride hailing contributes 55.8% share of the shared vehicles market owing to the convenience and accessibility it provides to users. Ride hailing services allow users to book a cab within minutes through their mobile apps, without having to wait by the roadside. This on-demand and hassle-free transportation model has made ride hailing very popular among users.

The ability to track cab locations in real-time and view estimated pickup times adds to the transparency and trust in these services. Ride hailing also provides cab services in locations that are not well covered by regular taxis or public transportation.

This fills an important gap and provides first-and last-mile connectivity to users. The popularity of ride hailing services is further driven by the attractive and flexible payment options they provide including cash, cards and wallet payments.

Insights, By Vehicles Type: Changing Mobility Preferences Fuel the Growth of Electric Vehicles

In terms of vehicles type, passenger cars contribute 83.8% share of the shared vehicles market in 2025. Within this segment, Electric Vehicles are gaining considerable traction owing to changing consumer preferences towards sustainable mobility solutions. With rising environmental concerns, many users are looking to switch to electric cars that have zero tailpipe emissions.

Government initiatives like subsidies and tax rebates on electric vehicles along with investments in charging infrastructure have made electric cars more viable propositions. Many leading automakers are also launching attractive electric car models to meet the growing demand.

The lower operating costs of electric vehicles compared to petrol/diesel vehicles is another major factor driving their adoption. As battery technologies advance further, range anxiety issues will reduce, fueling faster electric vehicle acceptance.

Insights, By Business Model: Peer-to-peer Model Encourages Vehicle Sharing

In terms of business model, B2C (business-to-consumer) contributes the highest share in the shared vehicles market currently. However, the P2P (Peer-to-Peer) model is emerging as an innovative sharing approach. The P2P model connects individual vehicle owners directly with users looking for temporary access. This allows for higher asset utilization as under-used personal vehicles can be rented out to others when not in private use.

P2P platforms ensure proper identity verification, reviews/ratings, insurance coverage and handling of transactions digitally. The flexible access facilitated by the P2P model encourages users to switch from private vehicle ownership. With rising preference for access over ownership among millennials, the P2P segment has strong growth potential in the shared vehicles market.

Additional Insights of Shared Vehicles Market

Case Study: In cities like Amsterdam and Copenhagen, bike-sharing programs have significantly reduced traffic congestion and pollution.

Event Impact: During major events like the Olympics, host cities have seen a surge in shared vehicle usage due to increased transportation demand.

Asia Pacific Growth: The region is witnessing rapid adoption of shared mobility services in the global shared vehicles market due to high urban population density.

Electric Vehicle Integration: Companies are increasingly adding electric vehicles to their fleets to meet environmental goals.

The shared mobility market is increasingly addressing urban issues like congestion and environmental concerns through innovative modes like peer-to-peer vehicle sharing and electric scooter rentals.

Competitive overview of Shared Vehicles Market

The major players operating in the shared vehicles market include Daimler AG, SIXT SE, Avis Budget Group Inc., Hertz Global Holdings, Inc., Europcar Mobility Group SA, DiDi Chuxing, Uber Technologies Inc, Lyft Inc, Grab Holdings Inc., BlaBlaCar, Zipcar Inc., Getaround Inc., Turo Inc., ANI Technologies Private Limited (Ola Cabs), and Car2Go (Share Now).

Shared Vehicles Market Leaders

Daimler AG

SIXT SE

Avis Budget Group Inc.

Hertz Global Holdings, Inc.

Europcar Mobility Group SA

*Disclaimer: Major players are listed in no particular order.

Shared Vehicles Market - Competitive Rivalry

Shared Vehicles Market

Market Consolidated (Dominated by major players)

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Shared Vehicles Market

In August 2024, Uber announced a multiyear strategic partnership with Cruise to deploy autonomous vehicles on the Uber platform, with plans to launch in 2025.

In August 2023, Lyft expanded its electric bike-sharing program to additional cities, promoting sustainable urban transportation. Lyft introduced Bay Wheels bike share stations in Golden Gate Park, San Francisco. Lyft celebrated the opening of the 1,000th Divvy station as part of a citywide expansion that added 400 new stations in Chicago.

Shared Vehicles Market Report - Table of Contents

RESEARCH OBJECTIVES AND ASSUMPTIONS

Research Objectives

Assumptions

Abbreviations

MARKET PURVIEW

Report Description

Market Definition and Scope

Executive Summary

Shared Vehicles Market, By Data Type

Shared Vehicles Market, By Vehicles Type

Shared Vehicles Market, By Business Model

Coherent Opportunity Map (COM)

MARKET DYNAMICS, REGULATIONS, AND TRENDS ANALYSIS

Market Dynamics

Impact Analysis

Key Highlights

Regulatory Scenario

Product Launches/Approvals

PEST Analysis

PORTER’s Analysis

Merger and Acquisition Scenario

Global Shared Vehicles Market, By Data Type, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Ride Hailing

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Bike Sharing

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Ride Sharing

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Car Sharing

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Others

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Shared Vehicles Market, By Vehicles Type, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Passenger Cars

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Two-Wheelers

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Electric Vehicles

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Shared Vehicles Market, By Business Model, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

B2C (Business-to-Consumer)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

P2P (Peer-to-Peer)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Shared Vehicles Market, By Region, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Data Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicles Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Business Model, 2020-2032, Value (USD Bn)

U.S.

Canada

Latin America

Introduction

Market Size and Forecast, By Data Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicles Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Business Model, 2020-2032, Value (USD Bn)

Brazil

Argentina

Mexico

Rest of Latin America

Europe

Introduction

Market Size and Forecast, By Data Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicles Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Business Model, 2020-2032, Value (USD Bn)

Germany

U.K.

Spain

France

Italy

Russia

Rest of Europe

Asia Pacific

Introduction

Market Size and Forecast, By Data Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicles Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Business Model, 2020-2032, Value (USD Bn)

China

India

Japan

Australia

South Korea

ASEAN

Rest of Asia Pacific

Middle East

Introduction

Market Size and Forecast, By Data Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicles Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Business Model, 2020-2032, Value (USD Bn)

GCC Countries

Israel

Rest of Middle East

Africa

Introduction

Market Size and Forecast, By Data Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicles Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Business Model, 2020-2032, Value (USD Bn)

South Africa

North Africa

Central Africa

COMPETITIVE LANDSCAPE

Daimler AG

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

SIXT SE

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Avis Budget Group Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Hertz Global Holdings, Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Europcar Mobility Group SA

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

DiDi Chuxing

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Uber Technologies Inc

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Lyft Inc

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Grab Holdings Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

BlaBlaCar

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Zipcar Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Getaround Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Turo Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

ANI Technologies Private Limited (Ola Cabs)

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Car2Go (Share Now)

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analyst Recommendations

Wheel of Fortune

Analyst View

Coherent Opportunity Map

References and Research Methodology

References

Research Methodology

About us

Shared Vehicles Market Segmentation

By Data Type

Ride Hailing

Bike Sharing

Ride Sharing

Car Sharing

Others

By Vehicles Type

Passenger Cars

Two-Wheelers

Electric Vehicles

By Business Model

B2C (Business-to-Consumer)

P2P (Peer-to-Peer)

Would you like to explore the option of buying individual sections of this report?

About author

Ameya Thakkar is a seasoned management consultant with 9+ years of experience optimizing operations and driving growth for companies in the automotive and transportation sector. As a senior consultant at CMI, Ameya has led strategic initiatives that have delivered over $50M in cost savings and revenue gains for clients. Ameya specializes in supply chain optimization, process re-engineering, and identification of deep revenue pockets. He has deep expertise in the automotive industry, having worked with major OEMs and suppliers on complex challenges such as supplier analysis, demand analysis, competitive analysis, and Industry 4.0 implementation.

Frequently Asked Questions :

How big is the shared vehicles market?

The shared vehicles market is estimated to be valued at USD 196.39 Bn in 2025 and is expected to reach USD 519.23 Bn by 2032.

What are the key factors hampering the growth of the shared vehicles market?

Limited availability of adequate transport infrastructure in certain regions and competition from ride-hailing and on-demand taxi services are the major factors hampering the growth of the shared vehicles market.

What are the major factors driving the shared vehicles market growth?

Increasing car ownership costs, including fuel, and maintenance and urbanization and traffic congestion are the major factors driving the shared vehicles market.

Which is the leading Data Type in the shared vehicles market?

The leading data type segment is ride hailing.

Which are the major players operating in the shared vehicles market?

Daimler AG, SIXT SE, Avis Budget Group Inc., Hertz Global Holdings, Inc., Europcar Mobility Group SA, DiDi Chuxing, Uber Technologies Inc, Lyft Inc, Grab Holdings Inc., BlaBlaCar, Zipcar Inc., Getaround Inc., Turo Inc., ANI Technologies Private Limited (Ola Cabs), and Car2Go (Share Now) are the major players.

What will be the CAGR of the shared vehicles market?

The CAGR of the shared vehicles market is projected to be 14.9% from 2025-2032.

Missing comfort of reading report in your local language? Find your preferred language :

Insights, By Data Type: Convenience and Accessibility Drive the Growth of Ride Hailing

Insights, By Data Type: Convenience and Accessibility Drive the Growth of Ride Hailing