Torque Vectoring Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Torque Vectoring Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Torque Vectoring Market is segmented By Propulsion (All-Wheel Drive (AWD)/Four-Wheel Drive (4WD), Front-Wheel Drive (FWD), Rear-Wheel Drive (RWD)), By Technology (Active Torque Vectoring Systems, Passive Torque Vectoring Systems), By Vehicle Type (Passenger Car, Light Commercial Vehicles, Heavy Commercial Vehicles), By Clutch Actuation (Electronic Clutch, Hydraulic Clutch), By Geography (North America, Latin America, Asia Pacific, Europe, Middle East, and Africa). The report offers the value (in USD billion) for the above-mentioned.

Torque Vectoring Market is segmented By Propulsion (All-Wheel Drive (AWD)/Four-Wheel Drive (4WD), Fr...

Torque Vectoring Market Size - Analysis

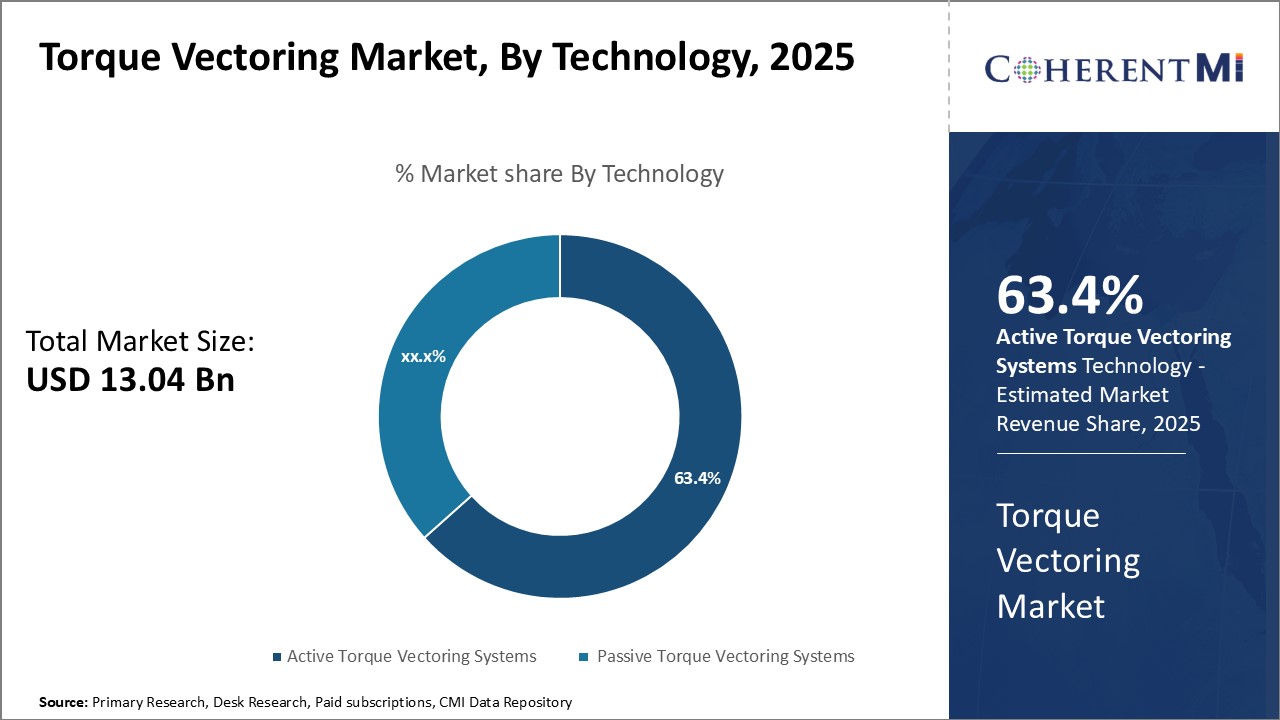

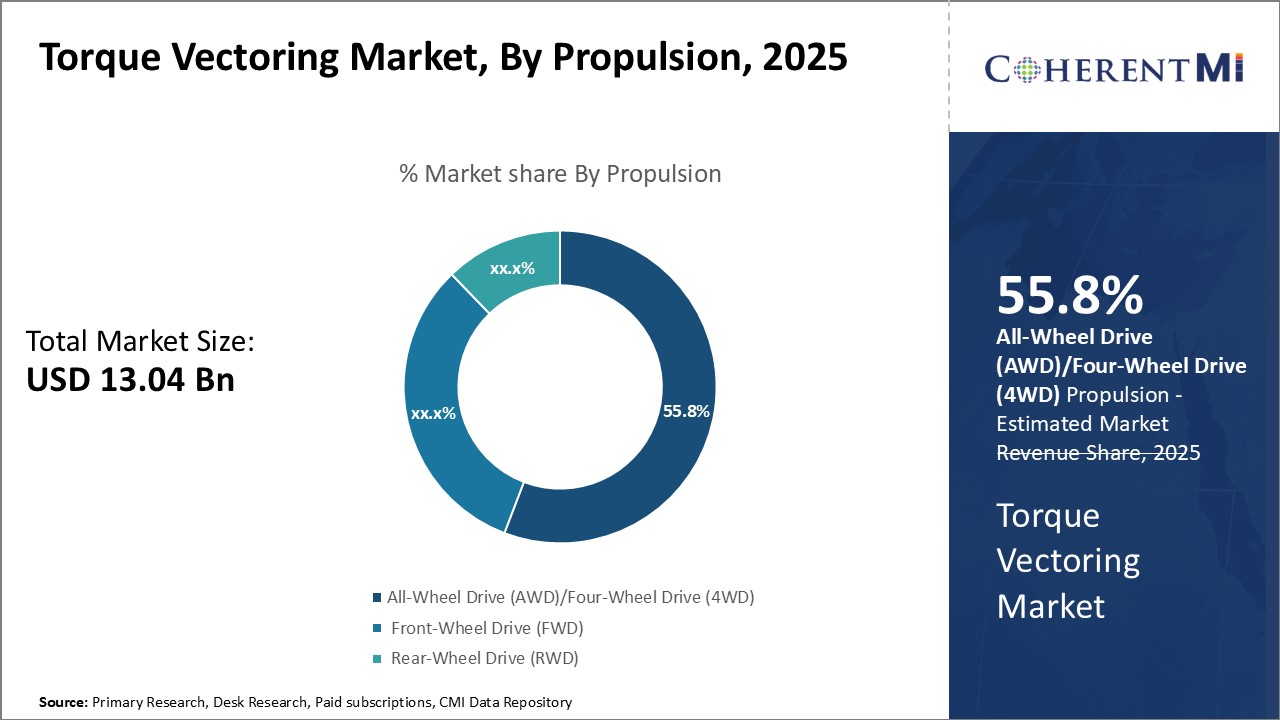

The torque vectoring market is estimated to be valued at USD 13.04 Bn in 2025 and is expected to reach USD 32.43 Bn by 2032, growing at a compound annual growth rate (CAGR) of 13.9% from 2025 to 2032. The torque vectoring market is witnessing positive trends driven by strict emission regulations mandating more fuel-efficient and lower emission vehicles.

Market Size in USD Bn

CAGR13.9%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

13.9%

Market Concentration

High

Major Players

GKN Automotive Limited, BorgWarner Inc., ZF Friedrichshafen AG, JTEKT Corporation, American Axle & Manufacturing Holdings, Inc. and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

Torque Vectoring Market Trends

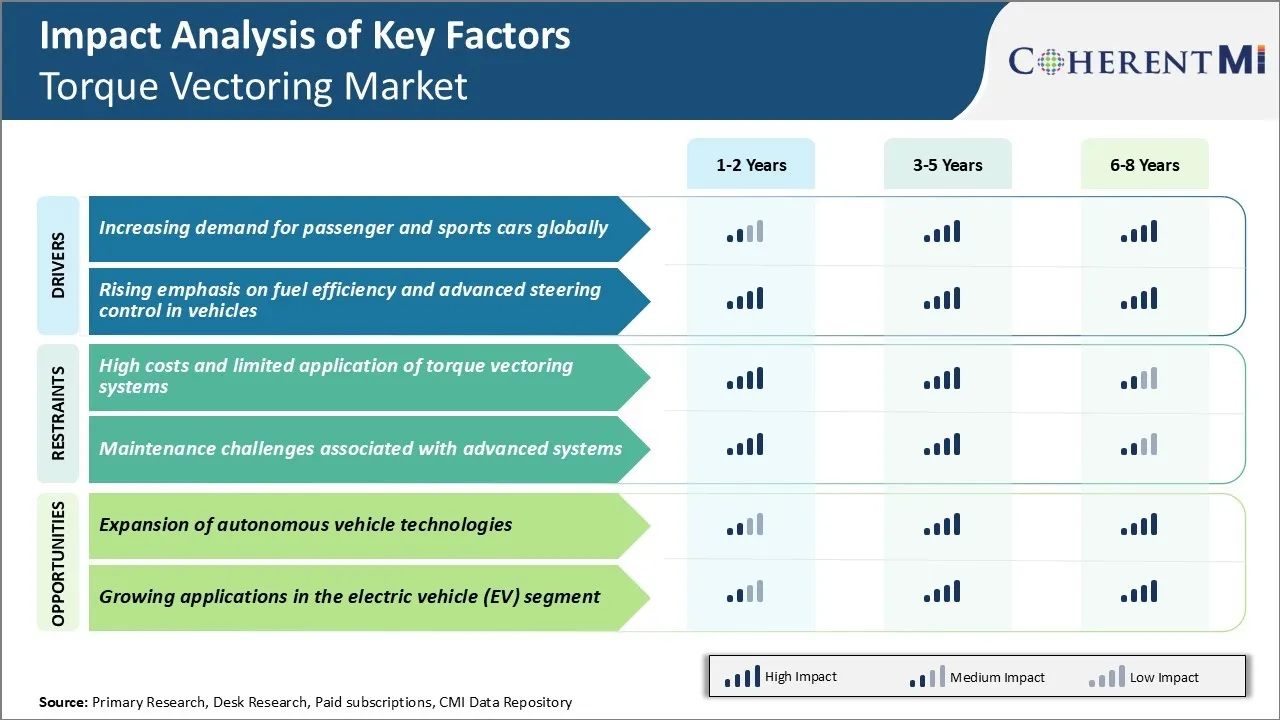

Market Driver - Increasing Demand for Passenger and Sports Cars Globally

The global automotive industry has seen tremendous growth in the production and sales of passenger cars as well as sports utility vehicles in the last decade. Sports vehicles and high-performance variants within mainstream brands have also become hugely popular globally.

However, delivering dynamic driving characteristics expected by customers from such sophisticated premium cars comes with its engineering challenges. Simply boosting engine power is not a viable long-term solution considering rising environmental regulations. This is where torque vectoring systems offer compelling benefits to auto companies.

Leading manufacturers now use advanced torque vectoring as a factor to differentiate their products in the torque vectoring market. As the passenger car boom continues unabated in major markets combined with buyers demanding superior handling athletically-styled vehicles, the uptake of torque vectoring hardware can only be expected to accelerate in the coming years.

Automakers and parts suppliers have intensified their efforts to engineer powertrains and supporting technologies that enhance fuel savings without compromising the driving experience customers want. For automakers to meet these dual challenges of efficiency gains and advanced driver assistance, innovative system-level solutions are crucial.

By intelligently channeling drive torque where it is needed the most, electronic torque vectoring enhances cornering ability, stability and straight-line traction from lower-powered 'downsized' engines. Simultaneously, state-of-the-art steering, braking and traction management improves vehicle handling under various conditions, aiding driver assistance functions such as automatic emergency braking and lane-keeping.

As the benefits of integrating sophisticated torque vectoring technology become more apparent, stricter carbon regulations and new safety mandates will further catalyze its adoption across all major global vehicle segments over the next decade. The upsides for both automakers and vehicle owners in terms of competitive differentiation, efficiency, driving pleasure and passenger protection are undeniable.

Market Challenge - High Costs and Limited Application of Torque Vectoring Systems

One of the key challenges faced by the torque vectoring market is the high costs associated with the development and implementation of these systems. Torque vectoring enables individual control of torque to each wheel, allowing for enhanced vehicle dynamics and safety.

However, to achieve this level of precision torque control requires sophisticated differentials, coupling mechanisms, and electronics. Developing these precision components and integrating them into the drivetrain increases costs substantially. Additionally, the onboard computing power and sensors required to process real-time torque data adds to the expenses.

As a result, torque vectoring systems end up being premium features available only in higher-end luxury and performance vehicles. Their application remains limited as mass market automakers are hesitant to adopt these costly technologies in mainstream vehicles. For the torque vectoring market to witness broader adoption, costs will need to come down significantly.

Market Opportunity - Expansion of Autonomous Vehicle Technologies

One of the major opportunities for the torque vectoring market is the expected expansion of autonomous vehicle technologies in the coming years. As self-driving capabilities continue to progress, vehicle dynamics and stability will become even more crucial for safely maneuvering autonomous vehicles without human input.

With more automakers aggressively working towards developing fully autonomous vehicles, the demand for safety and maneuvering enhancing technologies like torque vectoring is expected to rise. As autonomous vehicle technologies achieve wider adoption over the next decade, it can drive the torque vectoring market towards substantial growth.

Automakers may see torque vectoring as a key differentiator in offering superior safety and experience in self-driving vehicles. This emerging application can help accelerate the adoption of torque vectoring systems across more vehicle segments.

Key winning strategies adopted by key players of Torque Vectoring Market

BorgWarner's Dual Clutch Technology: Automakers like Audi, Porsche and Lamborghini implemented this technology, which improved vehicle dynamics and handling significantly. It helped these premium brands position themselves as leaders in performance and technology.

GKN's Twinster System: Automakers like Jaguar first implemented this on the XFR sedan in 2013. Independent rear wheel torque control enhanced traction, agility and stability even more than conventional all-wheel drive systems. It helped GKN secure partnerships with multiple OEMs and gain an early mover advantage in the emerging torque vectoring space.

ZF's Active Torque Vectoring: Automakers like Volkswagen, BMW, and Mercedes integrated this technology across their SUV lineups over 2016-18. ZF's focus on scalability, efficiency and packaging helped make torque vectoring an affordable option even for high-volume mainstream models, thereby expanding the torque vectoring market significantly.

Segmental Analysis of Torque Vectoring Market

Insights, By Propulsion: Enhanced Safety and Traction Leads to Dominance of AWD/4WD Systems

In terms of propulsion, all-wheel drive (AWD)/four-wheel drive (4WD) contributes 55.8% share of the torque vectoring market owning to its ability to provide optimal traction and safety. AWD/4WD systems distribute torque to all wheels simultaneously for improved acceleration, control and handling regardless of road conditions.

The even distribution of power to all wheels also increases stability at high speeds and while cornering. Automakers have recognized that many consumers are willing to pay more for the peace of mind that AWD/4WD offers in adverse weather. Crossover SUVs and luxury vehicles have especially benefitted from customer demand for advanced safety and enhanced driving dynamics.

Going forward, as standardization of advanced driver assistance systems increases expectations for vehicle response and maneuverability, the popularity of AWD/4WD configurations is expected to continue growing.

Insights, By Technology: Technology Leadership Drives Adoption of Active Torque Vectoring

In terms of technology, active torque vectoring systems contributes 63.4% share of the torque vectoring market due to its superior performance capabilities compared to passive torque vectoring systems. Active systems independently variably brake individual wheels using sensors and controllers to assess road conditions, acceleration and deceleration in real-time.

This allows for optimized torque distribution not just from front to rear, but also side to side for unprecedented agility, responsiveness and stability. Active systems strengthen overall vehicle dynamics to an extent not possible through suspension tuning or conventional differentials alone.

As a result, automakers can significantly boost handling, safety and driver enjoyment through advanced torque vectoring technology. The increasingly intuitive and seamless integration of active systems is driving rapid upgrades by both luxury performance brands as well as mass market electric vehicles seeking efficient dynamics.

Insights, By Vehicle Type: Passenger Vehicles Lead Adoption on Back of Enhanced Comfort and Safety

In terms of vehicle type, passenger cars contribute the highest share of the torque vectoring market due to the large volumes and growing emphasis on passenger comfort, infotainment and safety features. Torque vectoring technology also enhances passenger car dynamics to reduce fatigue on long trips while offering an elevated feeling of safety, stability, and predictable handling.

This resonates strongly with family buyers prioritizing ease of use and passenger well-being over commercial considerations like payload or duty cycles. Meanwhile, premium brands have successfully marketed torque vectoring as a key differentiator, justifying price premiums.

As technology costs decline and capabilities improve, mass market brands are also accelerating adoption rates to strengthen appeal against imported competition. Over time, these factors will see torque vectoring become standard much like ABS or stability control across all vehicle classes.

Additional Insights of Torque Vectoring Market

Integration in Electric Sports Cars: Manufacturers are increasingly incorporating torque vectoring in electric sports cars to improve acceleration, handling, and overall driving experience. This trend is expected to continue as EV technology advances in the torque vectoring market.

Collaborations Between Automakers and Tech Firms: There is a growing number of partnerships aimed at developing advanced torque vectoring systems, combining automotive expertise with cutting-edge technology.

Regional Growth Patterns: The Asia Pacific region is anticipated to witness the highest growth rate in the global torque vectoring market due to rapid industrialization, increasing disposable income, and a surge in demand for high-end vehicles.

Electric Vehicle Segment Surge: The torque vectoring market within the electric vehicle segment is projected to grow at a substantial CAGR, reflecting the global shift towards sustainable transportation.

Competitive overview of Torque Vectoring Market

The major players operating in the torque vectoring market include GKN Automotive Limited, BorgWarner Inc., ZF Friedrichshafen AG, JTEKT Corporation, American Axle & Manufacturing Holdings, Inc., Dana Incorporated, Continental AG, Bosch Ltd, Jtekt Corporation, GKN Automotive Limited, American Axle & Manufacturing, Inc., Univance Corporation, and Eaton Corporation.

Torque Vectoring Market Leaders

GKN Automotive Limited

BorgWarner Inc.

ZF Friedrichshafen AG

JTEKT Corporation

American Axle & Manufacturing Holdings, Inc.

*Disclaimer: Major players are listed in no particular order.

Torque Vectoring Market - Competitive Rivalry

Torque Vectoring Market

Market Consolidated (Dominated by major players)

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Torque Vectoring Market

In May 2024, BorgWarner introduced its electric Torque Vectoring and Disconnect (eTVD) system for battery electric vehicles (BEVs). This system is designed to intelligently control wheel torque, enhancing vehicle stability and dynamic performance.

In May 2024, Lamborghini introduced the Urus SE, the first plug-in hybrid version of their Super SUV. This model features an innovative electric torque vectoring system that enhances performance and adaptability across various driving conditions.

In June 2023, BorgWarner agreed to acquire the Electric Hybrid Systems (EHS) business segment of Eldor Corporation for €75 million, with the transaction expected to close in the third quarter of 2023. This acquisition aimed to enhance BorgWarner's capabilities in engineering compact and efficient 400V and 800V on-board chargers, as well as innovative high-frequency DC/DC converter technology.

Torque Vectoring Market Report - Table of Contents

RESEARCH OBJECTIVES AND ASSUMPTIONS

Research Objectives

Assumptions

Abbreviations

MARKET PURVIEW

Report Description

Market Definition and Scope

Executive Summary

Torque Vectoring Market, By Propulsion

Torque Vectoring Market, By Technology

Torque Vectoring Market, By Vehicle Type

Torque Vectoring Market, By Clutch Actuation

Coherent Opportunity Map (COM)

MARKET DYNAMICS, REGULATIONS, AND TRENDS ANALYSIS

Market Dynamics

Impact Analysis

Key Highlights

Regulatory Scenario

Product Launches/Approvals

PEST Analysis

PORTER’s Analysis

Merger and Acquisition Scenario

Global Torque Vectoring Market, By Propulsion, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

All-Wheel Drive (AWD)/Four-Wheel Drive (4WD)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Front-Wheel Drive (FWD)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Rear-Wheel Drive (RWD)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Torque Vectoring Market, By Technology, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Active Torque Vectoring Systems

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Passive Torque Vectoring Systems

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Torque Vectoring Market, By Vehicle Type, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Passenger Car

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Light Commercial Vehicles

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Heavy Commercial Vehicles

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Torque Vectoring Market, By Clutch Actuation, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Electronic Clutch

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Hydraulic Clutch

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Torque Vectoring Market, By Region, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Propulsion, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Technology, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicle Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Clutch Actuation, 2020-2032, Value (USD Bn)

U.S.

Canada

Latin America

Introduction

Market Size and Forecast, By Propulsion, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Technology, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicle Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Clutch Actuation, 2020-2032, Value (USD Bn)

Brazil

Argentina

Mexico

Rest of Latin America

Europe

Introduction

Market Size and Forecast, By Propulsion, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Technology, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicle Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Clutch Actuation, 2020-2032, Value (USD Bn)

Germany

U.K.

Spain

France

Italy

Russia

Rest of Europe

Asia Pacific

Introduction

Market Size and Forecast, By Propulsion, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Technology, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicle Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Clutch Actuation, 2020-2032, Value (USD Bn)

China

India

Japan

Australia

South Korea

ASEAN

Rest of Asia Pacific

Middle East

Introduction

Market Size and Forecast, By Propulsion, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Technology, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicle Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Clutch Actuation, 2020-2032, Value (USD Bn)

GCC Countries

Israel

Rest of Middle East

Africa

Introduction

Market Size and Forecast, By Propulsion, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Technology, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Vehicle Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Clutch Actuation, 2020-2032, Value (USD Bn)

South Africa

North Africa

Central Africa

COMPETITIVE LANDSCAPE

GKN Automotive Limited

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

BorgWarner Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

ZF Friedrichshafen AG

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

JTEKT Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

American Axle & Manufacturing Holdings, Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Dana Incorporated

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Continental AG

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Bosch Ltd

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Jtekt Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

GKN Automotive Limited

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

American Axle & Manufacturing, Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Univance Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Eaton Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analyst Recommendations

Wheel of Fortune

Analyst View

Coherent Opportunity Map

References and Research Methodology

References

Research Methodology

About us

Torque Vectoring Market Segmentation

By Propulsion

All-Wheel Drive (AWD)/Four-Wheel Drive (4WD)

Front-Wheel Drive (FWD)

Rear-Wheel Drive (RWD)

By Technology

Active Torque Vectoring Systems

Passive Torque Vectoring Systems

By Vehicle Type

Passenger Car

Light Commercial Vehicles

Heavy Commercial Vehicles

By Clutch Actuation

Electronic Clutch

Hydraulic Clutch

Would you like to explore the option of buying individual sections of this report?

About author

Yash Doshi is a Senior Management Consultant. He has 12+ years of experience in conducting research and handling consulting projects across verticals in APAC, EMEA, and the Americas.

He brings strong acumen in helping chemical companies navigate complex challenges and identify growth opportunities. He has deep expertise across the chemicals value chain, including commodity, specialty and fine chemicals, plastics and polymers, and petrochemicals. Yash is a sought-after speaker at industry conferences and contributes to various publications on topics related commodity, specialty and fine chemicals, plastics and polymers, and petrochemicals.

Frequently Asked Questions :

How big is the torque vectoring market?

The torque vectoring market is estimated to be valued at USD 13.04 Bn in 2025 and is expected to reach USD 32.43 Bn by 2032.

What are the key factors hampering the growth of the torque vectoring market?

High costs and limited application of torque vectoring systems and maintenance challenges associated with advanced systems are the major factors hampering the growth of the torque vectoring market.

What are the major factors driving the torque vectoring market growth?

Increasing demand for passenger and sports cars globally and rising emphasis on fuel efficiency and advanced steering control in vehicles are the major factors driving the torque vectoring market.

Which is the leading propulsion in the torque vectoring market?

The leading propulsion segment is all-wheel drive (AWD)/four-wheel drive (4WD).

Which are the major players operating in the torque vectoring market?

GKN Automotive Limited, BorgWarner Inc., ZF Friedrichshafen AG, JTEKT Corporation, American Axle & Manufacturing Holdings, Inc., Dana Incorporated, Continental AG, Bosch Ltd, Jtekt Corporation, GKN Automotive Limited, American Axle & Manufacturing, Inc., Univance Corporation, Eaton Corporation are the major players.

What will be the CAGR of the Torque vectoring market?

The CAGR of the torque vectoring market is projected to be 13.9% from 2025-2032.

Missing comfort of reading report in your local language? Find your preferred language :

Insights, By Propulsion: Enhanced Safety and Traction Leads to Dominance of AWD/4WD Systems

Insights, By Propulsion: Enhanced Safety and Traction Leads to Dominance of AWD/4WD Systems