腫瘍学の精密医療市場 サイズ - 分析 グローバルオノロジー精密医薬品市場は、 2024年のUSD 130億 そして到達する予定 2031年364億米ドル 、混合の年次成長率で育つ 2024年~2031年(CAGR) 8.9% 精密腫瘍学は、患者の特定の遺伝子、環境、ライフスタイルに合わせた治療および診断に焦点を当てています。 患者の遺伝子構造を分析し、利用可能な標的療法と一致させます。

市場は、世界的ながんの蔓延と腫瘍学におけるパーソナライズド薬の増大による大幅な成長を目撃する見込みです。 さらに、ゲノムの進歩と仲間の診断テストの可用性は、医師が個々の患者の腫瘍生物学の深い理解に基づいてカスタマイズされた治療計画を提供するのに役立ちます。 分子レベルでがんを理解するための継続的な研究は、さらに精密腫瘍学の実践の採用を推進します。

調査期間 2024 - 2031 推定の基準年 2023 CAGR 8.8% 市場集中度 High 主要プレーヤー アストラゼネカ, ノベルティ, パフィイザー, ブリストル・マイアーズ・スクイブ, ロチェ その他

*免責事項:主要プレーヤーは順不同で記載されています。

*出典:Coherent Market Insights

カスタマイズされたレポートを購入しますか?

今すぐカスタマイズ

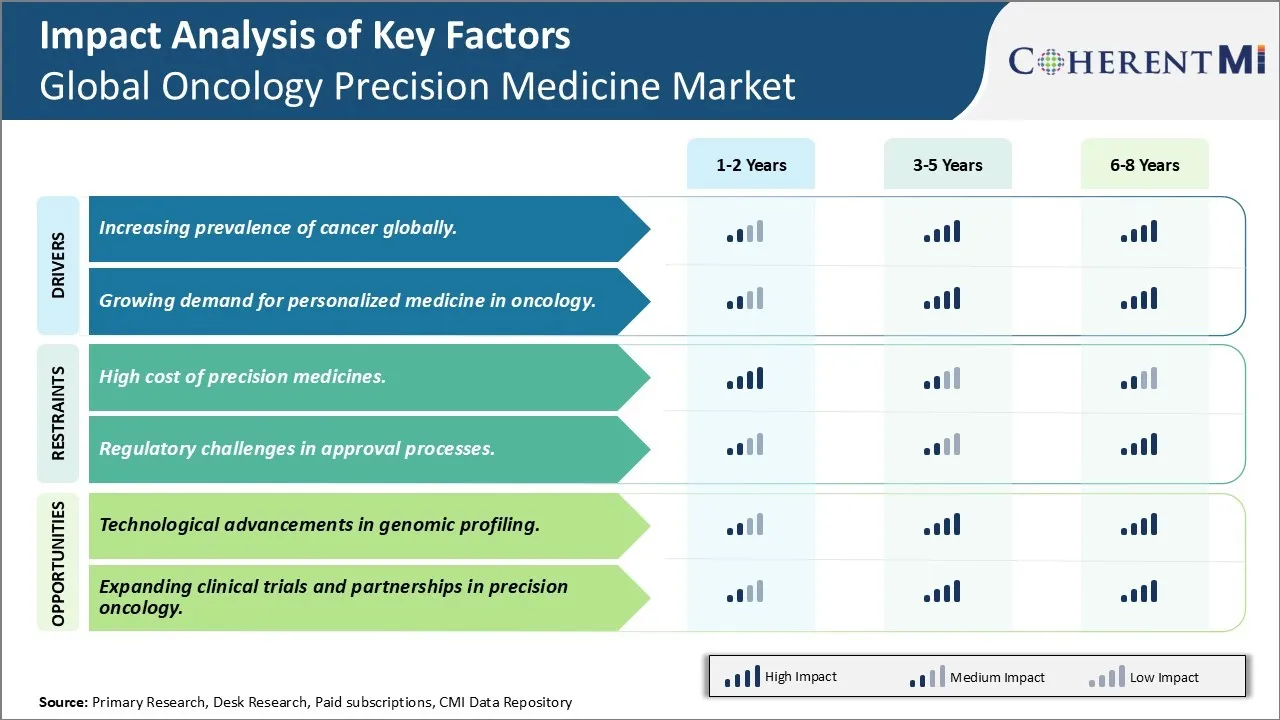

腫瘍学の精密医療市場 トレンド 市場ドライバー - がんのグローバル化を推進

がんの蔓延は世界中に急速に増加しています。 数年前、がんは発展途上国の病気と見なされていましたが、今では世界中で大きな公衆衛生問題として出現しました。 成長する寿命の期待のような要因, ライフスタイルや栄養習慣を変更することは、新しいがん症例の年々の安定した増加につながりました. がん死亡率は、より良い診断と治療のために、多くの高所得国で減少または維持されているが、発展途上国の負担は密接である。 WHOによると、がんの発生率は、グローバルに10年以上前から70%以上上昇すると予想されます。 この警急上昇は、がん患者を正確に診断し、効果的に治療するための新しい方法を見つける限り、医療システムとリソースを圧倒するように設定されています。 プレシジョンオノロジーは、患者さんの腫瘍に対する治療を仕立てることで、このプレスチャレンジに取り組むことを目指しています。 各がん症例に存在する独自の遺伝子変異とバイオマーカーを分析する強力な分子検査技術を活用します。 この詳細な分子プロファイリングに基づいて、医師は、その特定の癌に対して最善を尽くす標的薬、免疫療法または他の治療を選ぶことができます。 これは、従来のワンサイズフィットオール治療アプローチと比較して、より高い有効性とより良い結果をもたらします。 グローバルながん症例は、特に限られた資源で障がいのある国を発展させることで、今後数年もの間、適切な治療を可能にし、精密腫瘍学が希望を届けます。 幅広い採用により、がんケアのスパイラルコストを抑え、人々の生活を大幅に向上させることができます。 従って、急激に上昇するがんの発生率は、精密薬が満たす臨床的および経済的課題の両方を占めます。

オンコロジーにおけるパーソナライズド医療の需要の拡大

患者さんだけでなく、医療コミュニティも、パーソナライズされたがんケアの重要性を認識しています。 従来の治療戦略は、しばしばがん患者間で広く変化する根本的な腫瘍生物学を考慮することができません。 これは治療の矛盾、薬剤の抵抗および処置の失敗か再燃の高い率につながります。 精密医療は、各がんの分子指紋を細かくマッピングすることで、この欠点を解決します。 医師は、患者独自の疾患特性に合わせて最適な治療の組み合わせを選択するのに役立ちます。 患者さんの不適切な治療の毒性を緩和しながら、その結果が大幅に向上します。 精密腫瘍学のいくつかの最近の臨床成功は、患者の期待を高めました。 がん生存者は、ゲノムの洞察が将来的に他の人に提供できるパーソナライズされたケアのための同じ機会を望む。

同時に、腫瘍学者は治療の決定を指導する精密ツールの臨床ユーティリティを認めます。 包括的なゲノムプロファイリングは、実用的な突然変異を識別するのに役立ちます 証拠に基づく治療計画. また、潜在的な薬物標的および抵抗機構が応答措置を計画するために直面して明らかにします。 よりバイオマーカー主導の試験は、ゲノムの変化と薬物応答間の強い相関を確立するにつれて、精密医療は新しいケア基準として有意につながります。 受給者は、より高い応答速度、拡張生存の利点、コスト効率性の可能性の形でもその価値を認識します。 これらの利点により、分子腫瘍の分析とがん管理の標的療法に対する要求は、ステークホルダーグループ全体で加速されます。 研究者だけでなく、バイオ医薬品企業は、この成長の必要性を満たすために、精密技術と治療オプションの改善に継続的に取り組んでいます。

市場課題 - 精密医薬品の高コスト

世界の腫瘍学の精密医薬品市場で直面する主要な課題の一つは、精密医薬品に関連した高いコストです。 精密医薬品の開発には、がんの分子機構と標的療法が特定の変異にどのように影響を及ぼすかを理解するための広範な研究と臨床試験が必要です。 この研究開発プロセスは、製薬会社が行うのに非常に高価です。 開発されると、精密医薬品は、医薬品メーカーの投資を回復するために、患者や賃金から高い価格を要求します。 新しく開発された遺伝子治療とパーソナライズされた薬のコストは、治療コースごとに数百万ドルの頻度で実行されます。 患者様にとって重要な財務負担だけでなく、医療システムの持続可能性にもチャレンジしています。 手頃な価格の問題は、特に低・中所得国における精密療法の取込みと普及を制限する可能性があります。 製薬会社や規制機関は、これらの命を救う治療をより手頃な価格で、世界中のすべてのがん患者にアクセスできるように協力する必要があります。

ゲノムプロファイリングにおける市場機会分析の進歩

ゲノムプロファイリングおよび分子診断技術の成長する技術進歩は成長するために全体的な腫瘍学の精密薬の市場のための重要な機会を示します。 早期ゲノムプロファイリング必須腫瘍生検サンプルしかし、新しい非侵襲的または液体生検技術は、単純な血の引きから循環腫瘍DNAを分析することによって早期の癌検出を可能にする。 ゲノム試験のアクセシビリティが向上しました。 ゲノムシークエンシングコストをAIとビッグデータ分析で継続的に削減し、包括的ながんゲノムデータベースの開発を支援しています。 精密オンコロジー企業は、このようなゲノムインサイトと臨床試験データを活用し、追加のターゲットミューテーションとバイオマーカーシグネチャを識別することができます。 より正確なゲノムプロファイリングは、適切な患者グループに適切な治療を提供するのに役立ちます。 ゲノムデータをがんケア経路に統合することで、パーソナライズされたケアアプローチへのパラダイムシフトを加速します。 精密医薬品メーカーの有利な見込み客をご紹介します。

治療オプション分析 腫瘍学の精密医療市場 肺がんは、一般的に4つの主要なステージに分類されます - 第一次腫瘍およびリンパ節の関与の大きさと普及に基づいて、IVを段階的にする段階 - 。 段階によって治療オプションが異なります。

ステージI非小細胞肺がん(NSCC)の場合、がんを除去する手術は通常、第一次治療オプションです。 手術を受けられない患者にとって、スタトアブル放射線療法(SABR)は、立体体放射線療法(SBRT)とも呼ばれます。 SABRは、わずか1〜5セッションで直接放射線の非常に正確で高用量を実現します。

段階IIおよびIIIA NSCLCのために、標準的な第一線の処置は通常化学療法および放射線療法の組合せです。 シスプラチンやカルボプラチンなどの薬を使用したプラチナベースのダブルト化学療法は、一般的に使用される。 手術後だけで化学療法の代わりに並列化学化も段階II-IIIAの完全切除NSCLCのための標準的な処置です。

段階IIIBの高度か転移性NSCLCのために、プラチナ二重化学療法は標準的な第一線の処置を残します。 使用される一般的なレジメンは、pemetrexed、gemcitabine、paclitaxelまたはdocetaxelのカルボプラチンまたはシスプラチンです。 EGFR変異またはALKの転移を持つ患者のために、gefitinib、erlotinibまたはcrizotinibのようなALK阻害剤のような第一線EGFR TKIはそれぞれ化学療法上の改善された結果を提供します。

IV NSCLC、緩和化学療法、放射線療法、標的療法または免疫療法は、腫瘍の分子プロファイルに基づいて、すべての標準的な治療法の選択肢です。

主要プレーヤーが採用した主な勝利戦略 腫瘍学の精密医療市場 - コラボレーションとパートナーシップ : リード選手は、パーソナライズされた医薬品を開発し、商品化するために、数多くのコラボレーションを鍛造しています。 たとえば、2015年、ロチェは財団医学と提携し、ロチェのがん薬のポートフォリオに関するコンパニオン診断を開発しています。 これにより、Rocheは、患者を最も利益をもたらす可能性が高い特定するために、コンパニオン診断と一緒に標的療法を提供することができます。 そのようなパートナーシップは、企業が製品の提供と市場のリーチを拡大するのを助けました。

- バイオマーカー開発の焦点 : : : プレーヤーは、がんの患者を安定させ、治療の決定を導くのに役立つ新しいバイオマーカーを特定し、検証することに大きく投資しました。 たとえば、2010-2015年の間に、AstraZenecaは、バイオマーカーの研究に入った主要な部分である腫瘍学R&Dに6億ドル以上投資しました。 バイオマーカー主導の試験は、特定のバイオマーカー定義の患者集団におけるタグリッソやImfinziゲイン承認などの薬を助け、より標的された使用につながる。

- 補完技術の獲得 : 企業は、その精度の腫瘍学ポートフォリオを強化するための戦略的買収を行いました。 たとえば、2021年にバイオカーティスは、その分子検査能力を強化するためにQualitative Diagnosticsを取得しました。 2018年より、ロチェが財団薬を買収し、コンパニオン診断事業を強化。 このような買収により、プレイヤーがより包括的な精密医療ソリューションを提供できるようになりました。

- 臨床試験の革新: プレイヤーは、革新的なバスケット、傘、その他の新規トライアル設計を実施し、標的療法をバイオマーカー定義グループに加速します。 たとえば、2011-2015年の間に、MerckのKEYNOTE試験は50腫瘍タイプでpembrolizumabを評価し、頭頸部がんの新しい承認を識別しました。 ノベルの試験は、市場への精密治療を明示したのを助けました。

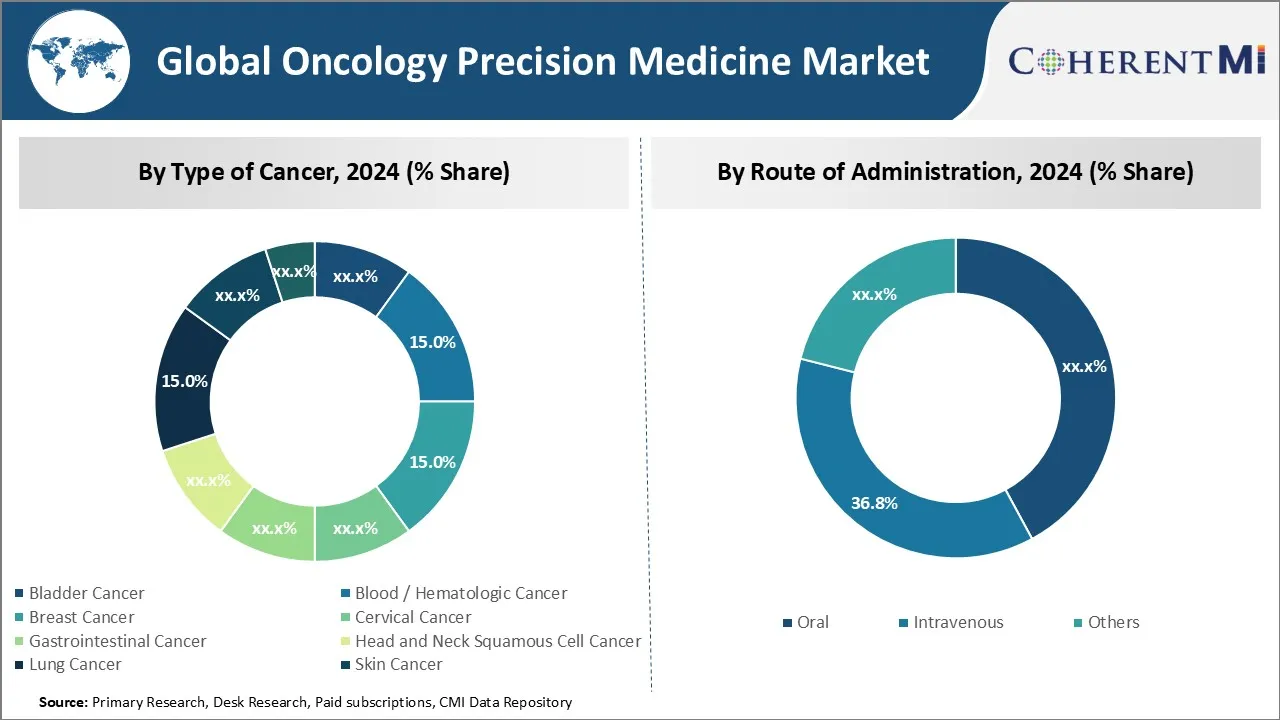

セグメント分析 腫瘍学の精密医療市場 がんの種類 - リスクファクターの有望性を上昇させることで膀胱がんセグメントの成長を促進

がんの種類によって、Bradder Cancerは、関連するリスク要因の上昇の優先順位に陥る市場の最も高いシェアに貢献します。 尿膀胱がんは異常な細胞が尿中膀胱で制御不能に成長したときに起こります。 膀胱がんのより高い発生率を運転している主要なリスク要因のいくつかは、タバコの消費の増加、労働化学的暴露、老化人口および膀胱感染症の歴史を含みます。

Tobacco の使用は、新症例の 50% を超える喫煙会計で膀胱がんの第一次リスク要因です。 喫煙率が高い国では、より大きな膀胱がんの負担を報告しています。 喫煙率をグローバルに削減する限られた進歩により、タバコにリンクされている膀胱がん症例が大幅に上昇する予定です。

また、芳香族アミンのような職業や環境化学物質への長期暴露、多環性芳香族炭化水素は、膀胱軟化剤と呼ばれています。 ゴム、革、繊維、塗料業界に携わる労働者は、リスクが高い。 新興市場での厳しい安全基準の急速な産業化と欠如は、長年にわたり化学的暴露が進んでいます。

老化の人口構造は別の顕著な運転者です。 膀胱がんリスクは、診断の年齢と中世の年齢を増加させることで73年です。 世界的な寿命の期待が高まり、前向きな人口統計は、より容認性が高い領域に向かってシフトしています。

尿路感染症や石の歴史は、膀胱がんのより高いオッズにも関連しています。 糖尿病と肥満の蔓延を増大させ、その両方が尿道の問題に陥り、膀胱がんのセグメントの成長に間接的に貢献しました。

病気の潜在的性質を考えると、高度な膀胱腫瘍は、しばしば化学療法、免疫療法および手術を含む複数の治療ラインを必要とします。 従って上昇の忍耐強い容積は膀胱癌のサブタイプおよび段階のために合わせられる精密薬の解決のための高められた要求に翻訳します。 これは、膀胱がんセグメントを推進する大きな要因です。

管理の経路によって - 経口ルートは、管理の消去のために支配します

行政の経路の中で、オーラルセグメンツは、世界的な腫瘍学の精密医薬品市場で最大のシェアを保持しています。 これは主に静脈内代替物に相対的な経口薬のための高められた忍耐強いアクセシビリティに起因します。

経口療法は、病院の訪問や熟練した健康の専門家を必要としない侵襲的な投薬を提供しています。 自宅での自己管理を可能にし、コンプライアンスと利便性を大幅に向上させます。 限られた医療インフラを持つ高齢化の人口と発展途上国における重要性が高まっています。

さらに、経口薬は、病院のリソースを必要とする長期の操業対頻繁な注入でより効果的です。 患者のポケットコストは、より良いアクセシビリティと手頃な価格につながる経口薬で低下しています。

医薬品会社だけでなく、経口製剤の観点から、注射薬と比較して、より高い利益率と優先償還方針を提示します。 製造、流通、保管は、経口錠剤の複雑さも少なくなっています。 これは、商業的に魅力的な経口精度腫瘍学ソリューションへの投資を行います。

経口経路は、標的療法や精密がんの治療の角質を形成する免疫療法などの慢性療法に適しています。 経口投与からの薬物の持続的な可用性は、断続的な不利な配達よりも優れたこれらのレジメンの目標と一致しています。

これらの患者、医療システム、および業界関連の利点を考えると、新しい精密医薬品製品の発売の大部分は、経口経路を介して市場優位性を時間をかけて燃やしています。 経口バイオアベイラビリティを改善し、経口投与をさらに強化する新たな製剤の出現。

分子タイプ別 - 安価 小さい分子の採用を運転して下さい

分子タイプでは、バイオロジックと比較して、その相対的なコスト効率性を追及する世界的な腫瘍学の精密薬セクターにおける最高のシェアのための小分子のアカウント。

化学的に合成される小型分子標的療法は高価なバイオ処理の条件なしでより低い生産費を楽しみます。 これは、世界中のストレッチされた医療予算のためのより競争力のある価格とより手頃な価格を可能にします。

より広い保険のカバレッジおよびより大きい忍耐強い人口への転換のより低いリストの価格は精密がんの心配にアクセスします。 小さな分子の固有の経済性は、開発市場と発展途上国を横断して、そのボリューム駆動の採用に積極的に影響を与えます。

さらに、最も小さな分子は口頭で生物学的に利用できるため、以前強調した便利な経口投与の優先順位によくリンクします。 これは、コストとコンプライアンスの観点から注射可能なバイオロジックよりも実用的な利点を倍増します。

大手小分子のジェネリックバージョンも、初期特許が期限切れになると、より手頃な価格のバイオシミラー/ジェネリックのための機会を作成します。 このような後続価格が減少し、小さな分子標的療法の継続的な優位性を促進します。

コールドチェーンの兵站学を要求する注射可能な抗体か他の生物的論理とは違って、小さい分子の丸薬は容易に貯えられ、世界的に運ぶことができます。 地理的なリーチを改善することにより、製薬会社にとってのアドレス指定可能なボリュームを拡大します。

追加の洞察 腫瘍学の精密医療市場 腫瘍学の精密医学の市場はヘルスケア産業の最も有望な区域の1つとして急速に進化しています。 従来のワンサイズのフィットオールアプローチから、よりパーソナライズされた治療計画へのシフトは、ゲノムデータ分析の進歩によって促進され、より効果的で副作用が少ないターゲット療法を可能にします。 腫瘍学における精密医学は、特に癌の分子の低下の理解を高めるために重要な潜在性を保持します。 これは、現在利用可能な145以上のパーソナライズされた医薬品と、早期開発段階で100以上のターゲット療法の開発と商品化に取り組んできました。 市場は、より効果的な治療、がんの上昇の蔓延、およびこの分野における継続的な革新のために、成長している需要によるさらなる拡大につながります。 北米地域は、現在最大の市場ですが、アジア・パシフィックは、臨床試験や政府の取り組みを拡大することにより、最高成長率を期待しています。 主要な市場トレンドを理解するには、サンプルをダウンロードしてくださいレポート。

競合の概要 腫瘍学の精密医療市場 グローバル・オノロジー・プレシジョン・メディック・マーケットでは、アムゲン、バイオNTech、ジャイラド・サイエンス、メルク&Co.、イルミナ、財団医学、ガーガント・ヘルス、カーリス・ライフ・サイエンス、オファクト・ジェネティックス、サーモ・フィッシャー・サイエンス、インビタ、ゲノミック・ヘルス、サイパス、テンパスなどがあります。

腫瘍学の精密医療市場 リーダー アストラゼネカ ノベルティ パフィイザー ブリストル・マイアーズ・スクイブ ロチェ *免責事項:主要プレーヤーは順不同で記載されています。

腫瘍学の精密医療市場 - 競合関係 市場が分散 (多くのプレーヤーが参入し、競争が激しい。)

*出典:Coherent Market Insights 最近の動向 腫瘍学の精密医療市場 2024年2月、Exscientia plc は、エクセアリン酸性白血病(AML)におけるエクセアリン酸性白血病(EXCYTE-2)の観察臨床研究を開始し、エクセアの薬物反応(EVDR)と実際の患者臨床結果の関係を探索しました。 本研究では、第一線のAML患者から血液および骨髄試料を採取し、潜在的拡大から第2線の患者へ、高い非メートルの医療ニーズの領域に対処します。 サンプルは、ExscientiaのクラウドベースのAIを使用して、パートナー研究所が遠隔で実行した分析で、Exscientiaのディープラーニング、単一セル精密医療プラットフォームを使用して処理されます。 2022年6月、GEヘルスケアは、新技術のコラボレーションを通じて、腫瘍学における精密薬の普及を推進しています。 当社の革新的な診断および治療技術は、がんの検出、臨床的および操作上の効率性、および患者の成果を改善することを目的としています。 GE Healthcare U.S.とカナダのカテリン・エストランペス(Catherine Estrampes)は、EMR、イメージング、バイオマーカー、および分子プロファイリングから患者のデータを統合するソリューションの必要性を強調しました。 9月発売 2023 - Exscientiaは、神経炎症および腫瘍学的障害のためのAIを搭載した精密薬の設計のためのMerckとライセンス契約を締結しました。 8月2023日 - IDEAYA バイオサイエンスは、特定の変異を伴うがん患者に焦点を当て、GSK101(IDE705)のFDAのINDクリアランスを発表しました。 2023年4月-タンゴの治療薬はTNG260のためのUSFDAの整理を、STK11水癌を目標としました。 レポートをカスタマイズしますか?

腫瘍学の精密医療市場 レポート - 目次 OBJECTIVESとASSUMPTIONSを探す マーケットプレイス レポートの説明

エグゼクティブ・サマリー

世界の腫瘍学の精密薬の市場、タイプの癌によって 世界の腫瘍学の精密薬の市場、管理のルートによって 世界の腫瘍学の精密薬の市場、分子のタイプによって 世界の腫瘍学の精密薬の市場、 ドラッグクラス コヒーレントの機会マップ (COM) マーケットダイナミクス、地域、トレンド分析 マーケット・ダイナミクス 衝撃解析 主なハイライト 規制シナリオ プロダクト進水/承認 PEST分析 PORTERの分析 合併・買収シナリオ 世界の腫瘍学の精密薬の市場、タイプの癌によって、2024-2031、(USD Bn) 導入事例

市場シェア分析、2024年、2031年 Y-o-Y成長分析、2019 - 2031 セグメントトレンド 膀胱癌

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 血液・肝がん

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 肝がん

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 子宮頸がん

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 消化管癌

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 頭頸部がん

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 肺癌

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 皮膚癌

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) その他

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) グローバル腫瘍学の精密薬市場、管理のルートによって、2024-2031、(USD Bn) 導入事例

市場シェア分析、2024年、2031年 Y-o-Y成長分析、2019 - 2031 セグメントトレンド オーラル

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) イントラベニアス

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) その他

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 世界の腫瘍学の精密薬の市場、分子のタイプによって、2024-2031、(USD Bn) 導入事例

市場シェア分析、2024年、2031年 Y-o-Y成長分析、2019 - 2031 セグメントトレンド 小さな分子

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) バイオロジック

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 世界の腫瘍学の精密薬の市場、薬剤のクラスによって、2024-2031、(USD Bn) 導入事例

市場シェア分析、2024年、2031年 Y-o-Y成長分析、2019 - 2031 セグメントトレンド キナーゼ阻害剤

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 酵素阻害剤

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) 免疫チェックポイント阻害剤

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) その他

導入事例 市場規模と予測、Y-o-Y成長、2019-2031、(USD Bn) グローバル腫瘍学精密医薬品市場、地域別、2019年 - 2031年、値(USD Bn) 導入事例

市場シェア(%) 分析, 2024,2027 & 2031, 値 (USD Bn) 市場Y-o-Y成長分析 (%)、2019 - 2031、値(USD Bn) 地域動向 北アメリカ

導入事例 市場規模と予測, がんの種類別, 2019 - 2031, 値 (USD Bn) 市場規模と予測, 管理のルートで , 2019 - 2031, 値 (USD Bn) 市場規模と予測, モールカルの種類によって , 2019 - 2031, 値 (USD Bn) 市場規模と予測、製薬クラス、2019 - 2031、値(USD Bn)による

ラテンアメリカ

導入事例 市場規模と予測, がんの種類別, 2019 - 2031, 値 (USD Bn) 市場規模と予測, 管理のルートで , 2019 - 2031, 値 (USD Bn) 市場規模と予測, モールカルの種類によって , 2019 - 2031, 値 (USD Bn) 市場規模と予測、製薬クラス、2019 - 2031、値(USD Bn)による

ヨーロッパ

導入事例 市場規模と予測, がんの種類別, 2019 - 2031, 値 (USD Bn) 市場規模と予測, 管理のルートで , 2019 - 2031, 値 (USD Bn) 市場規模と予測, モールカルの種類によって , 2019 - 2031, 値 (USD Bn) 市場規模と予測、製薬クラス、2019 - 2031、値(USD Bn)による

ドイツ アメリカ スペイン フランス イタリア ロシア ヨーロッパの残り アジアパシフィック

導入事例 市場規模と予測, がんの種類別, 2019 - 2031, 値 (USD Bn) 市場規模と予測, 管理のルートで , 2019 - 2031, 値 (USD Bn) 市場規模と予測, モールカルの種類によって , 2019 - 2031, 値 (USD Bn) 市場規模と予測、製薬クラス、2019 - 2031、値(USD Bn)による

中国・中国 インド ジャパンジャパン オーストラリア 韓国 アセアン アジアパシフィック 中東

導入事例 市場規模と予測, がんの種類別, 2019 - 2031, 値 (USD Bn) 市場規模と予測, 管理のルートで , 2019 - 2031, 値 (USD Bn) 市場規模と予測, モールカルの種類によって , 2019 - 2031, 値 (USD Bn) 市場規模と予測、製薬クラス、2019 - 2031、値(USD Bn)による

アフリカ

導入事例 市場規模と予測, がんの種類別, 2019 - 2031, 値 (USD Bn) 市場規模と予測, 管理のルートで , 2019 - 2031, 値 (USD Bn) 市場規模と予測, モールカルの種類によって , 2019 - 2031, 値 (USD Bn) 市場規模と予測、製薬クラス、2019 - 2031、値(USD Bn)による

競争力のある土地 アミューゲン

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 バイオNTech

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 ジャイラド科学

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 メルク&Co.

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 アルミナ

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 基礎医学

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 ガードラント健康

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 カリスライフサイエンス

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 正確な科学

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 Myriad 遺伝学

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 サーモフィッシャー科学

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 インビタ

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 ゲノムヘルス

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 シラプス

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 テンパス

企業ハイライト 製品ポートフォリオ 主な開発 財務・業績 戦略 アナリストの提言 フォーチュンホイール アナリストビュー コヒーレントの機会マップ 参考文献と研究方法論 腫瘍学の精密医療市場 セグメンテーション がんの種類別 膀胱癌 血液・肝がん 肝がん 子宮頸がん 消化管癌 頭頸部がん 肺癌 皮膚癌 その他 行政のルートで 分子の種類別 ドラッグクラス キナーゼ阻害剤 酵素阻害剤 免疫チェックポイント阻害剤 その他 購入オプションを検討しますか?このレポートの個々のセクション?

価格の内訳を取得します

About author Abhijeet Kale は、バイオテクノロジーおよび臨床診断分野で 5 年間の専門経験を持つ、結果重視の経営コンサルタントです。科学研究とビジネス戦略の豊富な経験を持つ Abhijeet は、組織が潜在的な収益源を特定し、ひいてはクライアントの市場参入戦略を支援します。彼は、FDA および EMA の要件を満たすための堅牢な戦略をクライアントが開発できるよう支援します。

よくある質問 : グローバル・オノロジー・プレシジョン・メディック・マーケットの成長を妨げる重要な要因は何ですか?

精密医薬品の高コスト。 承認プロセスにおける規制課題 グローバルな腫瘍学の精密医薬品市場の成長を妨げる主要な要因です。

グローバル・オノコロジー・プレシジョン・メディー・マーケットの成長を牽引する大きな要因は何ですか?

がんのグローバル化が進んでいます。 腫瘍学におけるパーソナライズド医薬品の需要の増加 グローバル・オノコロジー・プレシジョン・メディー市場を牽引する主要な要因です。

グローバル腫瘍学精密医薬品市場における主要ながんの種類は?

グローバル・オノロジー・プレシジョン・メディス・マーケットで運営する主要な選手はどれですか?

Amgen, BioNTech, Gilead Sciences, Merck & Co., Illumina, Foundation Medicine, Guardant Health, Caris Life Sciences, Exact Sciences, Myriad Genetics, Thermo Fisher Scientific, Invitae, Genomic Health, Syapse, Tempus は主要なプレーヤーです。

グローバルオノコロジーの精密医薬品市場のCAGRとは?

2024年から2031年にかけて、グローバルオノロジー・プレシジョン・メディック・マーケットのCAGRが8.9%となる見込みです。