澳大利亚医药调料市场 规模与份额分析 - 成长趋势与预测 (2024 - 2031)

澳大利亚医药调料市场按材料划分(无烟钢、钛、硝基醇(NiTi)、其他)、应用(Catheters & Cannulas、药物输送系统、牙医设备、机器人外科和其他)。 本报告为上述各部分提供了价值(百万美元)。....

澳大利亚医药调料市场 规模

市场规模(美元) Mn

复合年增长率8.60%

| 研究期 | 2024 - 2031 |

| 估计基准年 | 2023 |

| 复合年增长率 | 8.60% |

| 市场集中度 | Medium |

| 主要参与者 | 亚伯特, Dexcom股份有限公司., 美敦力学, 腾讯科技股份有限公司., F. 霍夫曼-拉罗什有限公司 以及其他 |

请告诉我们!

澳大利亚医药调料市场 分析

澳大利亚医药调料市场估计价值 599.47美元 Mn in 2024 (英语). 预计将达到 1,068.02美元 到2031年时以复合年增长率增长 (CAGR)从2024年到2031年占8.6%.

澳大利亚的老龄化人口和不断增加的保健开支正促使人们需要使用医管的先进医疗器械。

澳大利亚医药调料市场 趋势

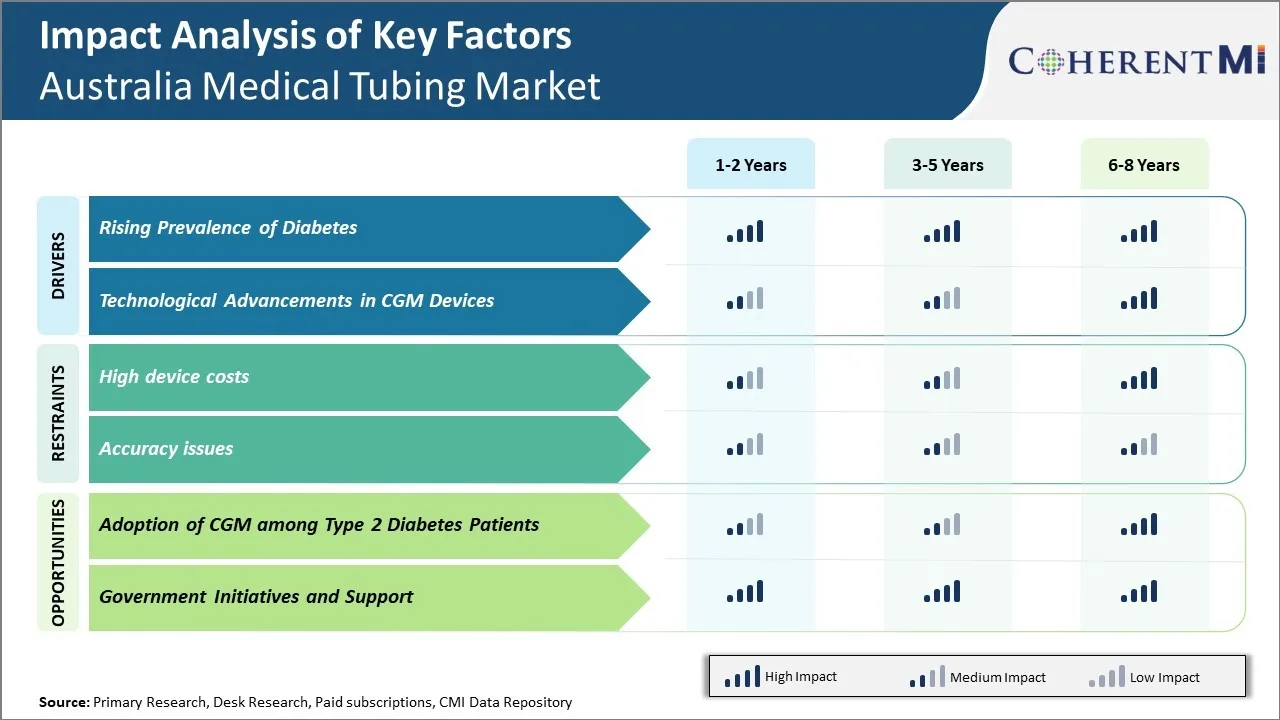

市场驱动力-糖尿病发病率上升

糖尿病发病率的上升是澳大利亚医药管状市场增长的一个主要动力。 根据澳大利亚统计局的资料,全国约有120万澳大利亚人患有糖尿病,这在过去几年中大大增加。 所有年龄组的1型和2型糖尿病发病率也在稳步上升。

糖尿病需要通过定期监测葡萄糖水平和胰岛素服用来进行终身的医疗管理. 这导致对胰岛素泵、导管和其他医疗应用中使用的医疗器械和管道等部件的大量需求。 根据澳大利亚卫生和福利研究所在2020年公布的数据,使用胰岛素泵的澳大利亚人数量在过去5年中翻了一番,现在使用的泵超过70,000个. 胰岛素泵使用导管和由窄直径管组成的复杂网络,持续在皮肤下输送胰岛素. 同样,经常需要透析的慢性肾脏疾病日益普遍,导致越来越多地使用导管、透析机和管子进行流体交换和血液净化。

市场驱动器-CGM设备的技术进步

连续葡萄糖监测装置的技术进步极大地推动了澳大利亚医药管状市场的成长。 CGM装置在糖尿病管理中变得很受欢迎,因为它们通过刚插在皮肤下的小柔性管子提醒患者高低血糖水平. 这种管子与葡萄糖感应器相连,以不进行指刺测试而持续监测水平. CGM通过发送数据给显示器或智能手机的发射机提供葡萄糖读数的实时更新.

融入这些新设备的尖端感应和无线技术需要用硅酮和聚氨酯等生物兼容材料制成的小型医疗管。 管子保护微妙的感应线,并允许舒适的下皮插入. 它通过防止插入地点的组织炎症,确保长期感应稳定性和连续的葡萄糖读数. 制造商正注重管尺寸和表面改造,以提高传感器寿命和用户方便度。 这种CGM设备设计的不断创新直接影响到澳大利亚对专业医用管的需求.

市场挑战-高设备成本

设备成本高昂,大大限制了澳大利亚医药管状市场的增长。 澳大利亚的医疗器械公司必须承担研究、开发和生产专门医疗器械和部件,包括医疗管材的高昂费用。 开发具有最新技术的创新医疗器械需要巨大的投资,从而增加生产成本。 此外,遵守TGA(治疗性物品管理局)关于批准和市场监测的严格管理规范也增加了总成本。

公司必须把增加的费用转嫁给医院和保健设施,对设备和管道产品定价更高。 这使得治疗和手术费用对普通人和公共保健系统来说极为昂贵。 根据澳大利亚卫生和福利研究所(AIHW)最近的报告,大约65%的澳大利亚人认为2020年的家庭预算负担不起医疗费用。 医疗器械的自付费用大幅增加,使人们无法接受必要的医疗手术。

市场机会-在2型糖尿病患者中采用CGM

澳大利亚在2型糖尿病患者中采用持续的葡萄糖监测(CGM)系统,为医疗管状市场的增长提供了重大机会。 CGM通过测量皮下的葡萄糖水平,用管子插入一个小传感器来工作. 这使得患者能够全天和全夜密切监测其血糖. 根据国际糖尿病基金会的资料,2型糖尿病的澳大利亚患者人数近年来大幅增加,预计将继续稳步增加。 随着该疾病发病率的上升,更多的患者和医生正在认识到CGM在帮助实现更强有力的葡萄糖控制以防止相关健康问题方面的益处.

CGM更全面地描述了食物、药物、活动和其他生活方式因素如何影响一个人的血糖水平。 这一详细信息使执业医师能够更好地为患者制定治疗计划和建议。 它还使患者能够自行进行调整,使水平保持在目标范围内.

竞争概览 澳大利亚医药调料市场

在澳洲医药调料市场运营的主要角色包括阿博特,德克斯康公司,梅德罗尼奇,森塞尼克斯股份有限公司,F. Hoffmann-La Roche有限公司,GLUCOVATION,INC.,内马乌拉医药股份有限公司,GlySens,GlucoModicum,和Signos股份有限公司.

澳大利亚医药调料市场 领导者

- 亚伯特

- Dexcom股份有限公司.

- 美敦力学

- 腾讯科技股份有限公司.

- F. 霍夫曼-拉罗什有限公司

澳大利亚医药调料市场 - 竞争对手

澳大利亚医药调料市场

(主要参与者主导)

(竞争激烈,参与者众多。)

澳大利亚医药调料市场 细分

- 按材料分类

- 无污钢

- 钛

- 尼蒂诺尔( Niti)

- 其他人员

- 通过应用程序

- catheters( Cannulas) (Cannulas) 系统

- 药品提供系统

- 牙医设备

- 机器人手术

- 其他人员

您想要了解购买选项吗?本报告的各个部分?

常见问题 :

哪些关键因素阻碍着澳大利亚医药调料市场的发展?

设备成本和准确性问题很高,是阻碍澳大利亚医药调料市场增长的主要因素。

是什么主要因素 驱动澳大利亚医疗调图市场增长?

糖尿病发病率的上升和CGM设备的技术进步是推动澳大利亚医药调料市场增长的主要因素。

澳洲医药调料市场的主要原料是什么?

主要材料段为无污钢.

在澳洲医药调料市场运营的主要角色是哪些?.

Abbott, Dexcom, Inc., Medtronic, Senseonics, Inc., F. Hoffmann-La Roche Ltd., GLUCOVATION, INC., Nemaura Medical Inc., GlySens, GlucoModicum, 和 Signos, Inc.)是主要角色.

澳洲医药调料市场CAGR将是什么?.

澳大利亚医药调料市场CAGR预计2024-2031年占8.6%.