医疗抽吸设备市场 规模与份额分析 - 成长趋势与预测 (2024 - 2031)

医疗抽吸设备市场按产品类型(AC-Powered Suction设备,电池-powered Suction设备,手动抽吸设备)按应用(呼吸,外科,胃,伤口排水等)划分,按终端用户(医院,救护车外科中心,诊所,家庭护理设置,紧急医疗服务)划分,按可移植性(便携式抽吸设备,站台抽吸设备)划分,按地理(北....

医疗抽吸设备市场 规模

市场规模(美元) Bn

复合年增长率5.2%

| 研究期 | 2024 - 2031 |

| 估计基准年 | 2023 |

| 复合年增长率 | 5.2% |

| 市场集中度 | High |

| 主要参与者 | 奥林匹斯, 莱达尔医疗, 梅德拉集团, 精密医学公司, ATMOS MedizinTechni GmbH & Co. KG公司 以及其他 |

请告诉我们!

医疗抽吸设备市场 分析

全球医疗抽吸设备市场估计价值 2024年1.41亿 预计将达到 到2031年达到2.03亿美元 以复合年增长率增长 (CAGR)从2024年到2031年占5.2%.

医疗吸附器械市场预计将在预测期间出现正增长。 关键因素,如各种慢性病的发病率上升以及在全球进行的外科手术数量增加,将推动对医疗吸附设备的需求。 此外,不断的技术进步,导致产品开发,满足各种最终用户的需要,包括家庭护理和紧急医疗服务,将进一步帮助扩大市场。 新兴国家采用便携式和无线设备进行吸附和不断增长的医疗旅游,也为该部门的市场参与者提供了巨大的增长机会。 然而,在预测年份,相关费用高昂可能对市场增长产生某种程度的不利影响。

医疗抽吸设备市场 趋势

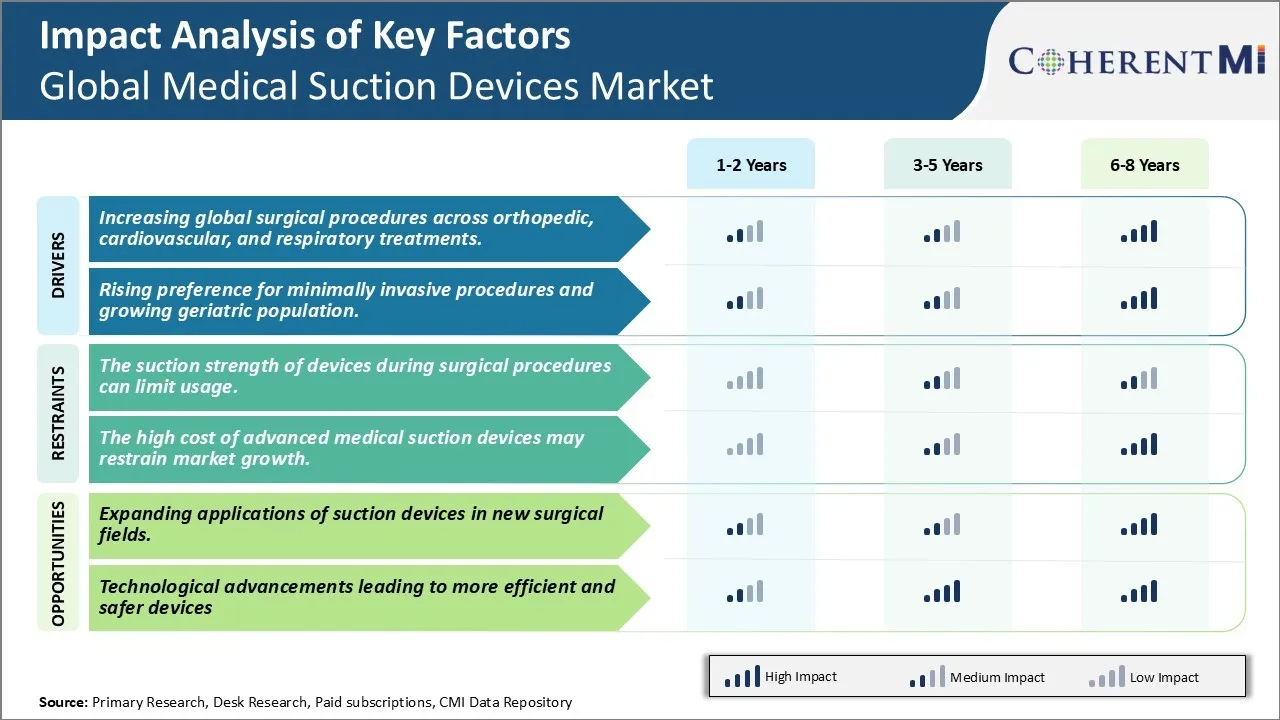

市场驱动器 -- -- 增加全方位整形、心血管和呼吸道治疗手术。

根据统计数字,过去几年来,全球手术数量大幅增加。 这种增加的外科手术趋势可归因于各种因素,如慢性病发病率增加、人口老龄化、外科技术和方法的进步以及发展中经济体的保健支出水平增加。

矫形外科手术出现强劲上升,其原因包括:肥胖症日益严重,导致矫形障碍;道路事故和伤害增加;包括膝盖和臀部替换在内的联合重置外科手术不断升级。 据估计,每年在全球进行超过400万次膝盖和臀部替换手术。 随着植入技术的改进、外科技术的改进和价格的提高,预计今后几年的体积将大幅增长。 抽吸装置在尽量减少失血以及在整形手术期间保持清晰的外科手术场方面发挥着至关重要的作用.

同样,心血管外科手术也因心血管疾病发病率上升以及越来越多地采用最低侵入性心脏手术而大大增加。 疾病核查数据已成为全世界发病率和死亡率的主要原因之一。 根据最近的报告,每年有1 700多万人死于CDs,占全球死亡总人数的近三分之一。 这进一步促使需要各种干预心脏程序,从而刺激了心血管部分对吸积装置的需求。

随着时间的推移,即使是呼吸道手术也出现了显著的增长率。 近年来,慢性呼吸道疾病,包括COPD、哮喘和肺癌,增加了多种。 这可归因于污染水平迅速上升,直到最近吸烟率上升,以及人口老化。 呼吸道疾病持续增加,可获得和负担得起的护理不断增多,对全球呼吸道手术数量产生了积极影响。 肺癌手术,气管切除等各种关键呼吸程序需要吸管装置来清除过多的液体,提供清晰的外科手术途径,并尽量减少风险.

对最低侵入性手术的偏好与日俱增,老年人口不断增加

随着先进技术和临床证据的积累,在过去几年中,尽量减少侵入性程序已成为各种手术的护理标准。 由于创伤减少、并发症减少、恢复时间缩短、疼痛和疤痕最小等好处,外科医生和病人都倾向于这些先进的手术。 越来越多的人使用最低侵入性技术来进行膝盖手术和机器人心脏手术等手术。 此外,由于日托或短期住院手术的方便性和可负担性,全世界也越来越倾向于这些手术。 抽吸装置在这种最小侵入性程序期间,在最大限度地减少出血和保持清晰视野方面发挥着重要作用。

与此同时,全球预期寿命的提高使全世界的老龄人口大幅增加。 根据联合国报告,预计在2015年至2050年期间,全球60岁及以上人口将从12%增至22%,翻一番。 老年人口更容易患上慢性病和受伤。 随着年龄的增长,身体的生理功能开始下降,增加了医疗干预的必要性。 此外,老年人可能已经服长期药物,需要不时进行手术或活检。 最近的进展使得甚至复杂的手术能够安全地对老年病人进行。 然而,必须遵守额外的预防措施和具体的文书要求。 因此,正在接受各种外科手术的老年人人数不断增加,预计在未来数年中将提高全球对安全和有效的吸附装置的需求。

市场挑战(Market Challenge) - 手术过程中设备的吸积强度可以限制使用.

手术过程中装置的吸积强度可以限制使用. 全球医疗吸积器械市场面临的主要挑战之一是这些器械在手术过程中提供的吸积强度不一致。 吸积强度需要根据手术不同阶段的要求加以控制和调整。 然而,许多现有设备在根据需要提供可变但一致的吸力方面有局限性。 在需要高度精确的复杂手术中,这一点变得更加困难。 任何吸积强度的不均匀,都可能扰乱外科医生的工作流程,影响手术结果. 设备制造商需要注重创新,设计可编程抽吸泵和系统,按照外科工作流程的实时要求提供可调整但恒定的抽吸。 这将有助于解决目前的局限性,并允许在不同类型的手术中更广泛地应用吸积装置。

全球医疗抽吸设备市场的市场机会

扩大吸管装置在新手术场的应用. 全球医疗吸积器械市场由于这些器械在新的外科垂直器械中的应用范围扩大,因此有可能出现巨大的增长机会。 传统上,抽吸泵和设备主要用于普通外科、妇科和牙科外科,用于清理手术现场的液体和分泌物。 然而,随着不断的进步,这些设备现在越来越多地在其他复杂的外科专业中找到应用。 例如,具有高度定制性提示的机械抽吸探测器有助于外科医生在细腻的手术中清晰地看到狭窄的手术场,如腹腔镜和动脉镜。 同样,便携式电池动力抽吸装置也使新的最低侵入性程序成为可能。 设备制造商可以利用这些新出现的机会,推出适合不同外科专业独特需要的专门产品范围。 这将有助于扩大市场推广范围,并有助于在多个治疗领域实现吸积工作流程的标准化。

关键参与者采用的关键制胜策略 医疗抽吸设备市场

产品创新: 采用旨在适应病人不断变化的需求的创新产品已证明是一项有效的战略。 例如,2015年,盟军医疗保健公司推出了ACHIEVE系列便携式吸积装置,其特性如电池寿命指标和易用控制. 这有助于他们获得市场份额。 同样,Medela LLC于2017年推出了其InnovaSate吸附设备,其中以Whisper技术为主,用于超静置. 小说具有提高护理质量和提升品牌声誉的特点。

战略采购: 获得既定品牌有助于公司扩大其投资组合和在各区域的存在。 例如,2019年,奥林匹斯公司收购了提供乳房泵和其他家庭护理解决方案的主角梅德拉. 这巩固了奥林匹斯在母乳喂养和母乳泵市场的存在。 同样,2021年,Invacare收购了第二大医疗器械公司Arjo. 这加强了Invacare的产品组合和全球销售。

关注新兴市场数字 : 发展中经济体可望推动未来的增长,而针对新兴的亚太和拉丁美洲国家则证明有利可图。 例如,自2010年以来,ATMOS MedizinTechnik将投资重点放在中国、印度和巴西。 到2017年,这些区域贡献了35%以上的收入. 同样,Medicop在俄罗斯和其他独联体国家设立子公司,有助于在2012-2017年期间,区域销售量每年增长18%。

这些例子表明,产品创新、战略收购和注重高增长地区如何帮助公司取得竞争优势,并在全球医疗吸附器械行业获得相当大的市场份额。 及时执行正确的战略有助于其领导职位。

分段分析 医疗抽吸设备市场

透视, 按产品类型 - 怎么样? AC功率抽吸设备的效率和可靠性驱动需求

就按产品类型而言,AC-Powered吸附装置由于其一贯的性能和成本效益,在2024年贡献了41.2%的市场份额. 直接从墙门供电,AC动力设备不需要更换电池,使其成为高容量设置的低维护选项理想. 它们具有强大和连续的吸吸能力,可以不间断地迅速清除液体,在紧急情况或复杂程序下至关重要。 随着保健设施努力争取及时治疗和周转时间,AC动力吸附装置满足了根据需要提供可靠吸附的需要。 它们的持久性也使它们成为一种值得长期投资。 由于电池没有随时间而降解,其吸积输出在整个设备寿命期间仍然强劲,与替代品相比,所有权的总成本降低。

透视,通过应用, - 呼吸系统应用从最大抽吸功能中受益

就应用而言,呼吸器在2024年占市场份额最高,为35%,在肺部护理中广泛使用吸积。 从空气中清除液体、分泌物、呕吐物或血液对呼吸、复苏和氧气治疗至关重要。 所提取材料的量和粘度往往很大,需要很高的吸积量,最好由医疗吸积装置提供。 其可移植性还允许在整个呼吸治疗和监测过程中在护理点持续抽吸。 各种呼吸吸附物精确地针对不同的气道,使得彻底而温和的清空成为可能. 由于呼吸状况继续影响大量病人,因此需要专门但灵活的吸附工具,促使这一应用部分的需求稳定。

透视,通过终端用户, - 获得关键护理助推器医院

在By End User方面,由于综合呼吸、手术和ICU病例的集中,医院在2024年占市场份额最高,为45%。 需求是由于紧急情况下需要迅速作出反应和住院病人情况复杂。 在医院基础设施内获得先进的外科手术、诊断和监测设备也需要相应的医疗吸附设备,用于各种应用和专科。 优先使用由设施支持的品牌高质量设备有助于确保病人的安全并遵守机构标准。 由于病人数量巨大,而且许多紧急和关键的护理需要需要吸食,医院是医疗吸食器械制造商大量和一贯的消费基础。

附加见解 医疗抽吸设备市场

- 医疗抽吸器械市场正在稳步增长,其动力是手术程序增加和入侵性最小的手术增加。 北美在市场上占主导地位,其中很大一部分归因于本区域先进的保健基础设施和老年人口的增加。 技术进步,如集成更有效的吸积机制和更好的材料,有可能为市场扩张创造新的机会。 然而,诸如先进设备成本高和关键程序期间吸积力有限等挑战可能会制约市场。

竞争概览 医疗抽吸设备市场

在全球医疗吸附器械市场运营的主要角色包括Laerdal Medical,Precise Medical, Inc., Medela AG, Olympus Corporation, Amsino International Inc., 盟军保健产品, Atmos Medizintechnik, Drive DeVilbiss Health Care, MG Electric (Colchester) Ltd., Asahi Kasei Corporation(Zoll Medical Corporation),Integra Biosciences AG, Labconco Corporation, Flexicare(Group) Limited,Stryker Corporation和Smith Medical.

医疗抽吸设备市场 领导者

- 奥林匹斯

- 莱达尔医疗

- 梅德拉集团

- 精密医学公司

- ATMOS MedizinTechni GmbH & Co. KG公司

医疗抽吸设备市场 - 竞争对手

医疗抽吸设备市场

(主要参与者主导)

(竞争激烈,参与者众多。)

最新发展 医疗抽吸设备市场

- 2024年4月(农历) Flexicare(集团)有限公司作为全球领先的创新医疗器械提供者,收购了联合保健产品。 这项收购旨在通过纳入应急产品、医疗气体系统、吸气调节器和呼吸器、运输通风器、二氧化碳吸收器和家庭保健产品等新领域,加强Flexicare的产品组合。 扩建后将利用Gomco,Lif-O-Gen,Chemetron,Timeter,Vacutron,Schuco,B&F Medical,Carbolime,以及LithoLyme等名牌品牌。

- 2023年3月(农历三月)国际安西诺公司 与Premier Inc达成了吸附和流体管理产品协议。 这项协议使总理成员能够获得事先商定的特别定价以及吸积和流体管理产品的条件。

- 2023年4月,Defibtech LLC推出了自动CPR设备ARM XR,其中包括用于在心肺复苏期间改善胸壁扩张的吸积杯活塞设计,增强心脏紧急情况下的患者结果.

- 2021年8月,波士顿科学公司获得了FDA的EXALTTM许可. 型号为B的单用途铜镜,为ICU和OR程序设计,提供优异的吸积和精确的成像.

- 2021年5月 (英语). 奥林匹斯获得FDA许可使用其航空道移动望远镜,在上下航道管理程序期间提供吸附和连续的空气供应.

医疗抽吸设备市场 细分

- 按产品类型

- AC 功率抽音设备

- 电池功率抽吸设备

- 手动抽吸设备

- 通过应用程序

- 呼吸器

- 手术

- 胃脏

- 排水

- 其他(牙科、兽医等)

- 按终端用户

- 医院

- 门诊中心

- 诊所

- 家庭护理设置

- 紧急医疗服务

- 按可移动性

- 便携式抽吸设备

- 固定抽吸设备

您想要了解购买选项吗?本报告的各个部分?

常见问题 :

哪些关键因素阻碍全球医疗抽吸设备市场的发展?

手术过程中装置的吸积强度可以限制使用. 先进的医疗吸附装置成本高昂,可能限制市场增长。 是阻碍全球医疗抽吸设备市场增长的主要因素。

驱动全球医疗抽吸设备市场增长的主要因素是什么?

全球整形、心血管和呼吸道治疗手术程序日益增多。 以及越来越偏爱最低侵入性手术 和不断增长的老年人口。 是推动全球医疗抽吸设备市场的主要因素。

哪个是全球医疗抽吸设备市场的主要产品类型?

主要的产品类型部分是AC-Powered吸附装置.

在全球医疗抽吸设备市场运营的主要角色是哪些?

Laerdal Medical, Precise Medical, Inc., Medela AG, Olympus Corporation, Amsino International Inc., 盟军保健产品 Atmos Mediziintechnik, Drive DeVilbis Health Care, MG Electrics (Colchester) Ltd., Asahi Kasei Corporation (Zoll Mediciney Corporation), Integra Bioscience AG, Labconco Corporation, Flexicare (Group) Limited, Stryker Corporation, Smith Medical是主要角色.

全球医疗吸附设备市场的CAGR将是什么?.

全球医疗抽吸设备市场的CAGR预计从2024-2031年达到5.2%.