美国热塑性弹性体市场 规模与份额分析 - 成长趋势与预测 (2024 - 2031)

美国热塑塑性塑胶市场按产品类型划分(钢筋混凝土聚合物、热塑性聚烯烃、热塑性聚氨酯、热塑性聚氨酯、热塑性聚氨酯、有机氟塑胶、聚酯以太塑性聚酯、其他),按应用(电动、电线和电缆、太阳能、建筑和建筑、阿德希西夫、西兰特和科林、脚套、消费品、医疗和保健等)。 本报告为上述部分提供了价值(10亿美元)....

美国热塑性弹性体市场 规模

市场规模(美元) Bn

复合年增长率5.5%

| 研究期 | 2024 - 2031 |

| 估计基准年 | 2023 |

| 复合年增长率 | 5.5% |

| 市场集中度 | Medium |

| 主要参与者 | 吉拉德橡胶公司, 航空橡胶公司, 邓纳奇工程, 橡胶公司联盟, 高山弹性产品,有限责任公司 以及其他 |

请告诉我们!

美国热塑性弹性体市场 分析

美国热塑性弹性市场估计价值为: 2024年1.77 Bn美元 预计将达到 2.21 Bn 至2031年,生长在一个 从2024年到2031年,CAGR为5.5%.

热塑性弹性体广泛应用于汽车、医疗和建筑业,这些行业正在推动这一市场的增长。 汽车工业不断增长的需求预计将成为关键的增长动力。

美国热塑性弹性体市场 趋势

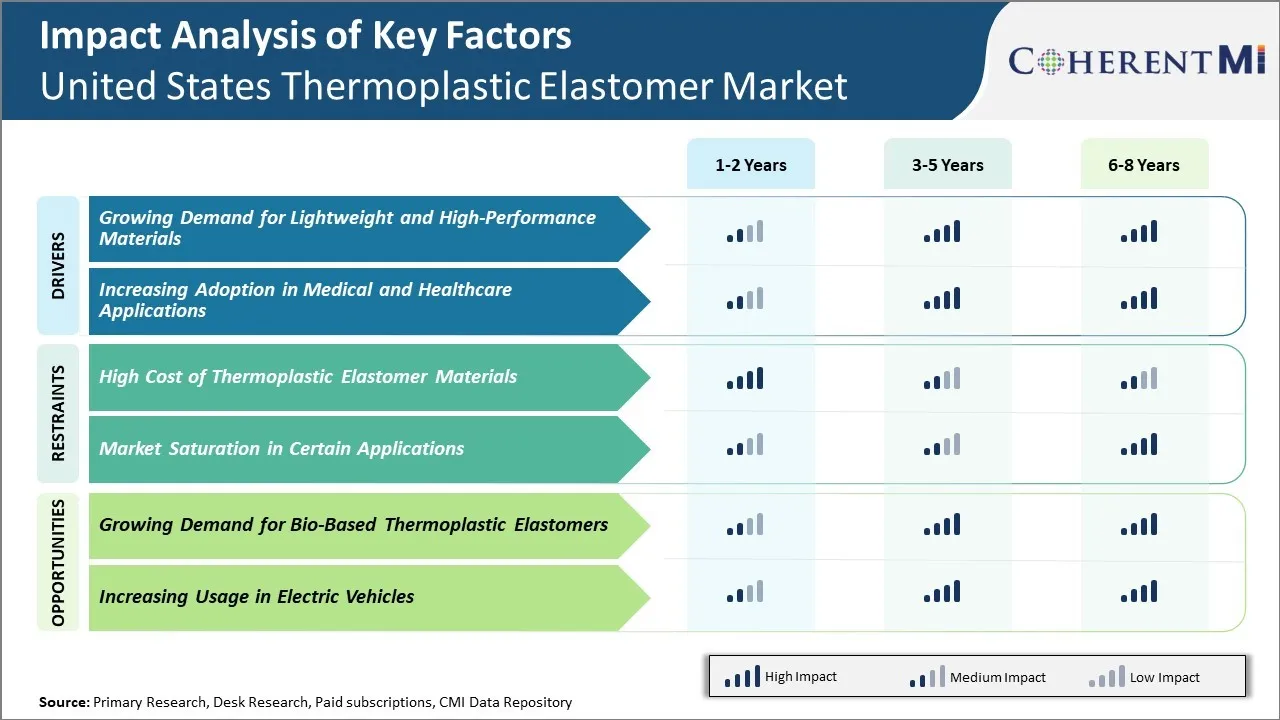

市场驱动力-对轻量级和高性能材料的需求不断增长

汽车、建筑和航空航天等不同行业对轻量级和高性能材料的需求日益增加,是推动美国热塑性弹性体市场增长的主要因素之一。 热塑性弹性体具有热塑性和弹性体的特性,使热塑性弹性体成为需要灵活性、抗撞击性和强度的应用的理想材料。

与常规材料相比,热塑性弹性体的重量要轻得多,同时提供等效或改进的机械性能. 例如,热塑性聚氨酯弹性体比标准橡胶材料轻25%. 汽车工业一直注重发展燃料经济性较强的轻型车辆,以达到严格的排放规范. 根据交通统计局的数据,在2020-2021年间,轻重量车辆材料的采用量增加了12%以上,这有助于改善美国新车辆平均燃料经济度6%。 这种对轻量级材料的日益重视,正在推动各种汽车组件如保险杠、门封和烤架的制造中使用热塑性弹性体。

市场驱动力 -- -- 增加医疗和保健应用的采用

美国的医药和保健行业在过去几年里有了巨大的增长,预计将继续沿着上升的轨道发展。 由于弹性、耐久性和生物兼容性等适宜特性,各种医疗装置和应用越来越多地使用热塑性弹性体。 高交替弹性耐力等属性使TPE适合需要弹性或压缩的重复应用,如弹性管、导管和伤口护理产品. 它们的热焊性还能提高制造效率和节省成本。

根据疾病控制与预防中心的统计数据,2019年约有6500万美国人接受了手术仪器,一次性装置和植入物等医疗程序. 在COVID-19大流行期间,对单用途医疗用品和设备的需求进一步激增,对通风机、氧气口罩和其他呼吸设备的需求增加。 热塑性弹性体由于其比其他材料的加工优势,在制造这些时间紧迫的产品方面发挥了关键作用。

市场挑战-热塑性弹性材料的高成本

热塑性弹性材料的高昂成本是美国热塑性弹性材料市场增长的主要障碍之一. 热塑性弹性体是工程化的聚合物,具有热塑性和弹性两种特性. 它们具有诸如可回收性、设计灵活性、耐久性和比常规热器橡胶更容易生产等优点。 然而,与普通的热塑性相比,热塑性弹性体因其复杂的分子结构和涉及的生产过程而更为昂贵。

生产热塑性弹性体所需的原材料成本很高,如苯乙烯块凝聚物,热塑性聚氨酯,热塑性聚烯烃等,进一步推高了价格. 据美国国际贸易委员会统计,美国苯乙烯块共聚物的进口价格从2020年1月的2.12/kg上升到2022年1月的2.38/kg. 同样,在同一时期,美国热塑性聚氨酯的进口价格从3.78美元/千克增加到4.23美元/千克。 丙烯、乙烯和原油是热塑性生产的主要原料,由于COVID-19大流行导致供应链中断,其价格在过去两年中也大幅上升。

市场机会-对基于生物的热塑性弹性体的需求日益增加

对以生物为基础的可持续材料的需求日益增加,是美国热塑性弹性体市场的一个重要机会。 传统上,大多数热塑性弹性体都来自石油原料。 然而,随着环境意识和可持续性目标的提高,品牌和消费者都在寻找碳足迹较低的替代品。

生物热塑性弹性体部分或完全来自可再生植物和农业资源,使制造商能够生产更环保的产品。 正在出现一些新的配方,在聚合物结构中利用基于生物的成分,如玉米、大豆、甘蔗或纤维素。 由于在生产过程中需要较少的矿物燃料,而且一旦废弃,已减少了报废排放量,因此符合更可持续的标准。 许多全球性组织还鼓励发展生物经济和循环生物产业。 根据经济合作与发展组织(经合组织)的一份报告,到2030年,生物经济有可能占全球制造业产出的7-8%。

汽车、消费品和医疗行业是生物热塑性弹性体的早期采用者。 例如,BASF与几家汽车制造商合作开发了以生物为基础的TPU,将其编译成内饰和其他汽车组件.

竞争概览 美国热塑性弹性体市场

在美国热塑性塑胶市场主要运营商包括吉拉德橡胶公司、航空橡胶公司、邓纳奇工程公司、联盟橡胶公司、高山塑胶产品公司、LLC、CS海德公司、Ames橡胶制造公司、VIP橡胶和塑料公司以及WARCO。

美国热塑性弹性体市场 领导者

- 吉拉德橡胶公司

- 航空橡胶公司

- 邓纳奇工程

- 橡胶公司联盟

- 高山弹性产品,有限责任公司

美国热塑性弹性体市场 - 竞争对手

美国热塑性弹性体市场

(主要参与者主导)

(竞争激烈,参与者众多。)

最新发展 美国热塑性弹性体市场

- 2023年8月,Covestro AG宣布计划在中国上海的Verbund遗址建造一座新的弹性体工厂. 预计这一扩展将提高公司的生产能力,满足该区域对热塑性弹性体日益增长的需求。

- 2020年7月,Asahi Kasei Corporation推出了"北美塑料"(APNA)和名为Soform的新型工程树脂系列,作为其Thermylene家族组合的一部分. 这一扩展旨在为客户提供范围更广的热塑性弹性体产品.

- 2021年1月,亨特斯曼公司以15.3亿美元收购了北美特产化学制造商加布里埃尔性能产品公司. 这次收购扩大了BASF的聚酰胺能力,以创新和著名的产品如Technyl.

美国热塑性弹性体市场 细分

- 按产品类型

- 钢筋混凝土

- 热塑性聚烯烃

- 热塑性 聚氨酯

- 热塑性聚酯

- 热塑性聚酰胺

- 热塑性挥发性

- 有机氟聚合物

- 以太塑胶

- 其他人员

- 通过应用程序

- 汽车

- 电缆( C)

- 太阳能(光伏应用)

- 建筑和建筑

- 粘合剂、西兰花和装饰

- 脚套

- 消费品

- 医疗和保健

- 其他人员

您想要了解购买选项吗?本报告的各个部分?

常见问题 :

哪些关键因素阻碍美国热塑性弹性市场的增长?

热塑性弹性体材料的高成本和某些应用中的市场饱和是阻碍美国热塑性弹性体市场增长的主要因素。

驱动美国热塑性弹性市场增长的主要因素是什么?

对轻量级和高性能材料的需求日益增加,在医疗和保健应用中越来越多地采用,这些都是推动美国热塑性弹性体市场的主要因素。

哪个是美国热塑性塑胶市场的主要产品类型?

主要产品类型段是Styrenic Block Copolymer(SBC).

在美国热塑性塑胶市场运营的主要角色是哪些?

Girard橡胶公司、Aero橡胶公司、Dunnage工程公司、联盟橡胶公司、高山弹性产品公司、LLC、CS海德公司、Ames橡胶制造公司、VIP橡胶和塑料公司以及WARCO是主要参与者。

美国热塑性塑胶市场CAGR将是什么?.

美国热塑弹性塑胶市场CAGR预计从2024-2031年达到5.5%.