Marché avancé de la gestion de la douleur du cancer ANALYSE DE LA TAILLE ET DU PARTAGE - TENDANCES DE CROISSANCE ET PRÉVISIONS (2024 - 2031)

Traitement avancé de la douleur du cancer Le marché est segmenté par classe de médicaments (anticorps monoclonal, cannabinoïde, aminoindane), par voie....

Marché avancé de la gestion de la douleur du cancer Taille

Taille du marché en USD Bn

TCAC5.6%

| Période d'étude | 2024 - 2031 |

| Année de base de l'estimation | 2023 |

| TCAC | 5.6% |

| Concentration du marché | High |

| Principaux acteurs | Tetra Bio-Pharma, Medlab Clinical Ltd, GW Pharmaceutiques, Pharmascience Inc., PharmaCielo et parmi d'autres |

Merci de nous le faire savoir !

Marché avancé de la gestion de la douleur du cancer Analyse

La gestion avancée de la douleur du cancer au niveau mondial Le marché est estimé à USD 8.1 Bn en 2024 et devrait atteindre 12,9 milliards de dollars en 2031, en croissance à un taux de croissance annuel composé (TCAC) de 5,6% de 2024 à 2031. La prévalence croissante du cancer dans le monde, associée à la demande croissante de médicaments et de thérapies efficaces pour la prise en charge de la douleur chez les patients cancéreux avancés, sont les facteurs clés de la croissance de ce marché. Des options avancées de gestion de la douleur ont considérablement amélioré la qualité de vie des patients cancéreux.

On s'attend à ce que le marché de la prise en charge avancée de la douleur du cancer augmente régulièrement au cours de la période de prévision en raison de l'augmentation de l'incidence du cancer et de l'adoption croissante de thérapies antidouleurs avancées. Le marché est témoin de l'introduction de nouvelles méthodes d'administration de médicaments et de thérapies combinées qui aident à mieux soulager la douleur avec des effets secondaires moindres. De plus, une sensibilisation accrue des patients, des fournisseurs de soins de santé ainsi qu'un soutien gouvernemental devraient également stimuler la demande de prise en charge efficace de la douleur dans le traitement avancé du cancer.

Marché avancé de la gestion de la douleur du cancer Tendances

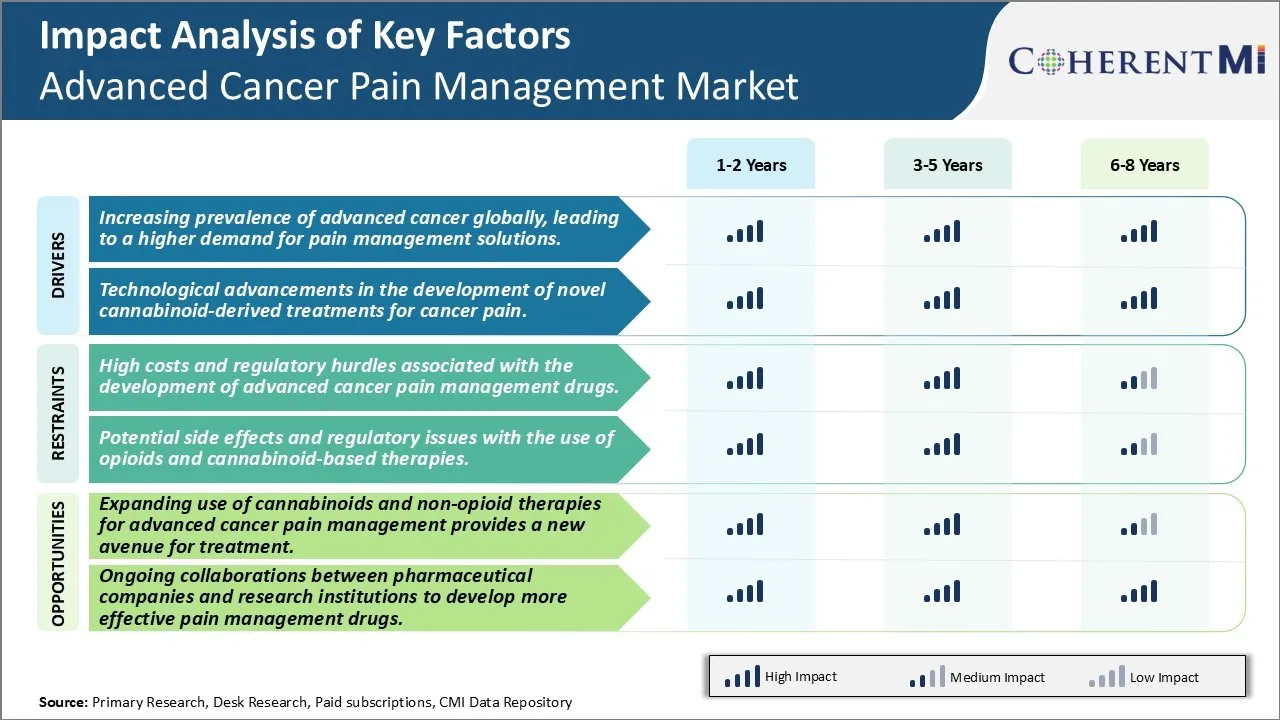

Pilote du marché - Augmentation de la prévalence du cancer avancé à l'échelle mondiale, menant à une demande accrue de solutions de gestion de la douleur.

À mesure que la prévalence des cancers de stade avancé continue d'augmenter dans les principales régions du monde, la nécessité d'une gestion efficace de la douleur devient de plus en plus importante. Diverses statistiques indiquent que l'incidence mondiale du cancer et la mortalité connexe ont augmenté à un rythme alarmant au cours des dernières décennies. Selon les estimations des experts de la santé, le nombre de nouveaux cas de cancer augmentera considérablement chaque année jusqu'en 2030. On s'attend à ce que la plupart de ces nouveaux cas soient diagnostiqués à des stades ultérieurs ou avancés lorsque la maladie a souvent déjà métastasé.

Avec les cancers de stade avancé viennent des complications graves qui influent grandement sur la qualité de vie d'un patient. L'un des symptômes les plus troublants est la douleur - qu'elle soit causée par la tumeur primaire, l'implication des tissus et organes environnants, ou par des lésions métastatiques dans d'autres parties du corps. Laissée sans traitement ou mal gérée, cette douleur peut parfois devenir chronique et même insupportable. Il entraîne une aggravation de la morbidité et du handicap chez les patients cancéreux avancés. Heureusement, des progrès considérables ont été réalisés ces dernières années pour mieux comprendre la douleur causée par le cancer et élaborer des approches de traitement plus efficaces. Néanmoins, alors que la prévalence des maladies avancées continue d'augmenter dans le monde entier, la gestion de la douleur associée demeure un défi clinique considérable ainsi qu'un domaine où les besoins ne sont pas satisfaits.

Pilote du marché - Les progrès technologiques dans les traitements dérivés des cannabinoïdes stimulent le marché avancé de la gestion de la douleur du cancer.

Les scientifiques étudient depuis longtemps le potentiel thérapeutique des cannabinoïdes, les composants chimiques actifs du cannabis, pour la gestion de la douleur. Cet intérêt a augmenté ces dernières années après la légalisation de la marijuana médicale dans de nombreuses régions du monde. Un domaine important a été l'élaboration de traitements à base de cannabinoïdes pour la douleur cancéreuse, qui s'est avérée très difficile à contrôler en utilisant uniquement des analgésiques conventionnels. Divers progrès technologiques permettent maintenant aux chercheurs de mieux comprendre les mécanismes de liaison des phytocannabinoïdes spécifiques aux récepteurs endogènes des cannabinoïdes dans le corps ainsi que leurs effets de signalisation en aval.

Cela a permis la formulation de substances pharmaceutiques botaniques précisément conçues qui peuvent cibler le système endocannabinoïde plus sélectivement et avec moins d'effets secondaires par rapport aux préparations végétales entières. Les fabricants ont également mis au point de nouveaux modèles de livraison de médicaments comme des films sublinguals et des comprimés de dissolution orale qui aident à améliorer la biodisponibilité et les profils pharmacocinétiques des composés cannabinoïdes. Certaines formulations commencent même à combiner des cannabinoïdes avec d'autres médicaments contre la douleur pour développer des thérapies synergiques multi-cibles. Dans l'ensemble, les améliorations continues des techniques d'extraction des cannabinoïdes et de la pharmacie élargissent les options pour les cliniciens en tant que méthode complémentaire ou alternative dans le contexte avancé de la gestion de la douleur du cancer.

Défi du marché - Coûts élevés et obstacles réglementaires associés à l'élaboration de médicaments anticancéreux de pointe.

La mise au point de nouveaux médicaments innovateurs pour la prise en charge avancée de la douleur cancéreuse est confrontée à des défis importants en raison des coûts élevés et des exigences réglementaires rigoureuses en cause. Mettre un nouveau médicament sur le marché coûte généralement plus de USD 2,6 milliards et prend 10-15 ans en raison du processus de recherche et d'essai clinique requis pour prouver l'innocuité et l'efficacité d'un médicament selon les normes réglementaires. Pour les médicaments anticancéreux de pointe, en particulier, des essais cliniques de grande envergure et complexes sont nécessaires pour démontrer l'efficacité de la gestion des différents types de douleur subis par les patients atteints d'un cancer au stade avancé. Ces essais nécessitent un financement important et du temps pour recruter des milliers de patients afin d'obtenir des résultats statistiquement significatifs. Tout retard ou échec au cours des phases d'essai clinique peut obliger les promoteurs de médicaments à encourir plus de coûts ou à abandonner complètement le programme. De plus, des organismes de réglementation comme la FDA imposent des règles très strictes pour l'approbation de nouveaux médicaments contre la douleur causée par le cancer en raison de la population de patients vulnérables et du risque d'effets secondaires de puissants analgésiques. Les promoteurs de médicaments doivent satisfaire à toutes les exigences cliniques, de fabrication et d'étiquetage de la FDA, qui impliquent des études et des investissements supplémentaires, avant d'obtenir l'autorisation de commercialiser leur médicament. Ces coûts intensifs de recherche et de conformité réglementaire constituent des obstacles majeurs qui limitent le nombre d'organismes qui s'efforcent d'élaborer de nouveaux traitements pour la prise en charge avancée de la douleur cancéreuse.

Opportunité de marché : développer l'utilisation des cannabinoïdes et des thérapies non opioïdes pour la prise en charge avancée de la douleur cancéreuse offre une nouvelle avenue pour le traitement.

Une occasion émergente réside dans l'acceptation et l'exploration croissantes d'approches alternatives pour traiter les douleurs cancéreuses avancées qui évitent les dangers de la dépendance aux opioïdes et les effets secondaires. Les cannabinoïdes dérivés de la marijuana, à savoir le THC et le CBD, démontrent leur potentiel en tant que remèdes naturels. Les études montrent qu'elles peuvent aider à réduire la douleur, les nausées et d'autres symptômes. Leur nature non-addictive par rapport aux opioïdes réduit également les risques. Il faut davantage de données cliniques sur la posologie et les formulations, mais l'intérêt pour la recherche augmente compte tenu de la demande d'options non opioïdes. Parallèlement, des traitements pharmacologiques non opioïdes sont en cours de développement. Ceux-ci comprennent des patchs de lidocaïne, des antidépresseurs et des bloqueurs nerveux qui soulagent la douleur par des mécanismes non opioïdes. À mesure que la compréhension de la physiopathologie de la douleur au cancer s'étend, des traitements non opioïdes plus ciblés peuvent être identifiés. Avec un soutien sociétal accru pour le cannabis médical et l'accent mis sur la crise des opioïdes, les cannabinoïdes et les thérapies non sarcotiques complémentaires représentent un segment de marché largement inexploité. La croissance semble prometteuse car la sensibilisation à ces propagations alternatives au sein des cercles oncologiques et des fournisseurs de soins palliatifs et les patients cancéreux cherchent des solutions au-delà des opioïdes conventionnels. Tant les sociétés pharmaceutiques que les entreprises de produits du cannabis voient des gains à réaliser en créant des offres novatrices dans ce créneau en plein essor.

Préférences des prescripteurs de Marché avancé de la gestion de la douleur du cancer

Pour les cancers de stade avancé, le traitement suit plusieurs lignes au fur et à mesure que la maladie progresse et s'adapte. Pour le traitement de première intention des cancers métastatiques, la chimiothérapie demeure la norme en raison des rapports risques-avantages favorables. Les régimes combinés comprenant des médicaments à base de platine comme le carboplatine (Paraplatine) associés à des taxanes comme le paclitaxel (Taxol) sont couramment prescrits.

Si le cancer devient résistant ou cesse de répondre, l'immunothérapie est apparue comme une option de deuxième intention importante. Les inhibiteurs du point de contrôle ciblant les voies PD-1/PD-L1 comme le pembrolizumab (Keytruda) et l'atezolizumab (Tecentriq) sont fréquemment choisis en raison des réponses durables observées, même si une toxicité minimale permet d'autres lignes de traitement.

Pour les patients en immunothérapie ou avec des types de tumeurs moins faciles à utiliser, les thérapies ciblées offrent une approche alternative de deuxième ligne si des mutations spécifiques sont présentes. Par exemple, l'osimertinib (Tagrisso) est prescrit pour le cancer du poumon non à petites cellules de l'EGFR+ après l'échec des inhibiteurs de l'EGFR antérieurs.

Au-delà de la deuxième ligne, les choix de traitement visent à maximiser le contrôle des symptômes et la qualité de vie avec une toxicité minimale. La monothérapie taxane, les thérapies hormonales ou les médicaments expérimentaux dans les essais cliniques peuvent être considérés selon l'aptitude du patient et les traitements récents. Les préférences du prescripteur à des stades ultérieurs intègrent l'état de performance et la tolérance du patient en plus des données d'efficacité.

Les coûts globaux du traitement exercent également une influence, en particulier dans la collectivité où les coûts hors de portée ont une incidence sur l'accès et l'adhésion des patients. Cela incite les médecins à évaluer soigneusement la valeur thérapeutique à chaque ligne de traitement.

Analyse des options de traitement de Marché avancé de la gestion de la douleur du cancer

Le cancer avancé désigne le cancer qui s'est propagé au-delà du site original vers d'autres parties du corps. Le traitement dépend du type et du stade du cancer, ainsi que de la santé globale et des préférences du patient. Pour de nombreux cancers de tumeurs solides avancés, la norme de soins implique la chimiothérapie.

La chimiothérapie de première intention implique généralement un doublet à base de platine, comme le cisplatine ou le carboplatine associé au paclitaxel, au docétaxel, à la gemcitabine ou au pemetrexed. Ces combinaisons visent à contrôler la croissance tumorale et à prolonger la survie. Pour les cancers comme le cancer du poumon ou le cancer colorectal répondant mal au traitement de première ligne, les options de deuxième ligne comprennent les monothérapies comme le docétaxel, le paclitaxel, le pemetrexed, ou les médicaments ciblés comme le cetuximab, le panitumumab ou le bevacizumab selon le statut de biomarqueur.

Dans le cas des cancers qui progressent encore en traitement de deuxième intention, les options de troisième intention sont limitées et impliquent souvent des essais cliniques de nouveaux régimes ou médicaments. L'immunothérapie est également apparue comme une approche de traitement importante, avec des inhibiteurs de contrôle comme le nivolumab, le pembrolizumab et l'atezolizumab approuvés pour différents types de tumeurs. Ceux-ci sont généralement utilisés après les échecs de chimiothérapie en raison de leur profil favorable des effets secondaires. Pour certaines mutations tumorales, des thérapies ciblées qui bloquent des gènes spécifiques à la conduite du cancer sont également disponibles. chirurgie d'élimination de tumeurs agressives ou radiothérapie peut fournir un contrôle local et améliorer la qualité de vie, le cas échéant.

Stratégies gagnantes clés adoptées par les principaux acteurs de Marché avancé de la gestion de la douleur du cancer

Innovation des produits : Les thérapies contre la douleur et les technologies de gestion de la douleur contre le cancer évoluent rapidement. L'une des stratégies les plus efficaces adoptées par les principaux intervenants a été l'investissement continu et l'accent mis sur la R-D pour élaborer des produits nouveaux et plus efficaces.

Partenariats et acquisitions : Les entreprises se sont associées ou ont acquis d'autres acteurs offrant des portefeuilles complémentaires pour étendre leurs gammes de produits.

Commercialisation ciblée Stratégies : Compte tenu de l'hétérogénéité de la douleur cancéreuse et de la nécessité de traitements personnalisés, les intervenants ont lancé des efforts de promotion énergiques à l'égard des patients et des médecins. Ils effectuent des études de marché approfondies pour comprendre les groupes spécialisés et adapter les campagnes éducatives en conséquence.

Ces initiatives stratégiques appuyées par des données probantes en matière d'investissement dans la R-D, de fusions et de partenariats tactiques et d'activités de promotion ciblées ont aidé les entreprises de premier plan dans l'espace avancé de gestion de la douleur liée au cancer à obtenir une forte traction en termes de revenus, de parts de marché et de perception de la marque. Une approche holistique des produits, des portefeuilles et du marketing semble essentielle au succès.

Analyse segmentaire de Marché avancé de la gestion de la douleur du cancer

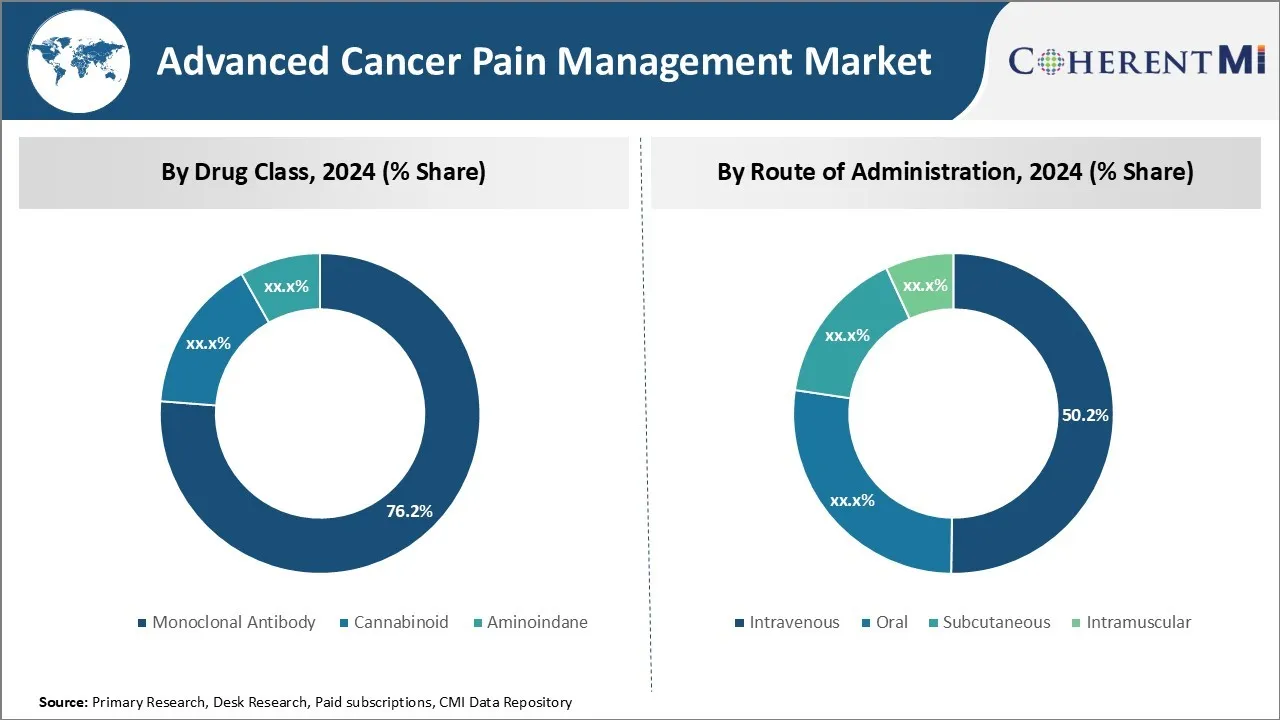

Insights, Par classe de médicaments, les options de traitement avancées favorisent la domination monoclonale des anticorps.

Par classe de médicaments, les anticorps monoclonaux devraient représenter la part de marché la plus élevée 76,2 % en 2024 en raison de leur mécanisme d'action ciblé et de l'amélioration des profils d'efficacité et d'innocuité par rapport aux autres classes de médicaments traditionnelles. Les anticorps monoclonaux ont révolutionné le traitement du cancer ces dernières années en fournissant un ciblage plus précis des cellules cancéreuses tout en limitant l'exposition systémique et les effets non ciblés. Ces anticorps agissent en se liant à des protéines spécifiques sur les cellules cancéreuses et immunitaires, comme les récepteurs, et en perturbant les voies de signalisation qui permettent aux tumeurs de croître et de se propager.

Comparativement à d'autres classes de médicaments comme les opioïdes qui fournissent un large soulagement de la douleur systémique mais qui comportent des risques importants de sécurité, les anticorps monoclonaux offrent une approche plus ciblée pour bloquer les signaux de douleur directement à leur source. Ce mécanisme d'action supérieur a donné lieu à des anticorps monoclonaux démontrant une réduction robuste de la douleur dans les essais cliniques avec moins d'effets secondaires que d'autres options. Leur développement a également été motivé par la nécessité de thérapies plus durables et avancées pour gérer les douleurs cancéreuses, car les patients vivent plus longtemps avec une maladie métastatique.

Les grandes sociétés pharmaceutiques ont beaucoup investi dans le développement d'anticorps monoclonaux nouveaux pour traiter divers types de cancer ainsi que leur douleur associée. Les médicaments Blockbuster comme le bevacizumab et le rituximab ont préparé le terrain pour une nouvelle génération de thérapies anticorps avec des capacités de ciblage raffinées. La tendance vers les médicaments de précision a élevé les anticorps monoclonaux comme le choix de traitement préféré parmi les oncologues et les patients. Avec leurs profils de sécurité différenciés et leur efficacité élevée contre la douleur cancéreuse, les anticorps monoclonaux devraient continuer de dominer ce segment du marché de la gestion avancée de la douleur cancéreuse.

Insights, Par voie d'administration, Augmenter les options d'administration Fuel Secteur intraveineux Dominance.

Par voie d'administration, la part de l'administration intraveineuse devrait atteindre 50,2 % en 2024 en raison d'avantages par rapport aux autres voies d'administration. Bien que l'administration orale offre la commodité aux patients, de nombreuses thérapies anticancéreux ont une faible biodisponibilité orale ou nécessitent des doses élevées pour atteindre des niveaux thérapeutiques systémiques. Cela peut entraîner une absorption incohérente et des effets secondaires dus à des niveaux élevés de médicaments dans le foie et le tractus gastro-intestinal.

En revanche, l'administration intraveineuse permet une administration précise des médicaments directement dans la circulation sanguine, maximisant la disponibilité au site d'action et évitant les problèmes liés au métabolisme gastro-intestinal et du premier passage. Pour les médicaments anticancéreux qui doivent atteindre des concentrations systémiques rapides et élevées comme les opioïdes, la voie intraveineuse permet d'administrer des doses titrables en milieu médical pour gérer soigneusement les niveaux de douleur. Certaines thérapies sont également conçues spécifiquement pour l'usage par voie intraveineuse en raison de leurs demi-vies courtes et la nécessité de refaire fréquemment.

De plus, de nombreux patients atteints d'un cancer avancé éprouvent des problèmes tels que des nausées, des vomissements ou des difficultés à avaler, qui limitent l'apport oral à mesure que la maladie progresse. La voie intraveineuse contourne ces problèmes et assure l'administration efficace des médicaments quel que soit leur état de performance. Les options auto-administrées comme les injections sous-cutanées ou intramusculaires nécessitent également des conditions physiques et mentales stables. Ainsi, pour les patients atteints d'un cancer grave avec une douleur sévère, la thérapie intraveineuse reste la méthode d'administration standard d'or.

Insights, By Distribution Channel, Prevalence of Hospital Based Care Boosts Hospital Pharmacies Segment.

En termes de By Distribution Channel, Hospital Pharmacies contribue la plus grande part du marché en raison de nombreux patients cancéreux recevant un traitement dans les hôpitaux. Pour les personnes diagnostiquées avec un cancer avancé ou métastatique, des thérapies agressives comme la chirurgie, la chimiothérapie ou le rayonnement sont souvent nécessaires. Ces interventions sont principalement pratiquées dans les hôpitaux hospitaliers par des oncologues et des chirurgiens médicaux.

Pendant les phases de traitement actif impliquant des régimes complexes et une surveillance fréquente, la plupart des médicaments anticancéreux sont également initiés et titrés sous surveillance médicale dans les hôpitaux. Cela permet d'observer de plus près les patients en cas d'effets indésirables ou de complications de médicaments à haut risque comme les opioïdes. Il garantit également un approvisionnement constant en médicaments adaptés aux plans de soins en évolution rapide, car l'état du patient et les niveaux de douleur fluctuent par la thérapie.

Une fois le traitement terminé, de nombreux survivants du cancer font encore face à des rendez-vous de suivi de mois à années et à des soins palliatifs potentiels si la douleur persiste. Cette collaboration continue avec les fournisseurs de soins hospitaliers soutient la demande de médicaments contre la douleur par l'intermédiaire des pharmacies hospitalières. Les services spécialisés de préparation, d'entreposage et de documentation fournis font également des hôpitaux un guichet unique pour les traitements complexes contre la douleur au cancer.

Avec la majorité de la prise en charge du cancer toujours centrée autour des hôpitaux, il s'ensuit que les pharmacies hospitalières domineraient la distribution de médicaments de gestion de la douleur affiliés. Leur intégration au sein des systèmes de soins de santé permet une exécution transparente des prescriptions par rapport aux sources externes de vente au détail. Cela positionne les pharmacies hospitalières comme le principal canal d'approvisionnement pour le marché avancé de la gestion de la douleur du cancer.

Informations supplémentaires sur Marché avancé de la gestion de la douleur du cancer

La prise en charge avancée de la douleur du cancer demeure un domaine critique des soins en oncologie. Les patients atteints d'un cancer avancé souffrent souvent de douleurs sévères qui peuvent affecter leur qualité de vie et leur adhésion au traitement. Les approches traditionnelles de gestion de la douleur, comme les opioïdes, bien qu'efficaces, présentent des risques importants, y compris la dépendance et les effets secondaires indésirables. Le nouveau pipeline de médicaments, comme QIXLEEF de Tetra Bio-Pharma et NanaBis de Medlab Clinical Ltd, représente un virage vers des thérapies à base de cannabinoïdes qui offrent des avantages potentiels avec moins de risques par rapport aux opioïdes. Ces médicaments dérivés des cannabinoïdes ciblent des voies de douleur spécifiques et offrent une alternative naturelle aux patients souffrant de douleurs cancéreuses non contrôlées. De plus, les collaborations continues entre les sociétés pharmaceutiques, comme le partenariat entre Medlab Clinical Ltd et Pharmascience Inc., devraient améliorer la disponibilité de ces traitements novateurs à l'échelle mondiale. L'avenir de la prise en charge avancée de la douleur cancéreuse est susceptible de se concentrer sur des traitements personnalisés non opioïdes qui améliorent à la fois le soulagement de la douleur et les résultats des patients.

Aperçu concurrentiel de Marché avancé de la gestion de la douleur du cancer

Les principaux acteurs du marché avancé de la gestion de la douleur du cancer sont Tetra Bio-Pharma, Medlab Clinical Ltd, GW Pharmaceuticals, Pharmascience Inc., PharmaCielo, Tilray Pharmaceuticals, WEX Pharmaceuticals, Pfizer, eurofins, Sigma-Aldrich, GSK plc et Recipharm.

Marché avancé de la gestion de la douleur du cancer Leaders

- Tetra Bio-Pharma

- Medlab Clinical Ltd

- GW Pharmaceutiques

- Pharmascience Inc.

- PharmaCielo

Marché avancé de la gestion de la douleur du cancer - Rivalité concurrentielle

Marché avancé de la gestion de la douleur du cancer

(Dominé par des acteurs majeurs)

(Très compétitif avec de nombreux acteurs.)

Développements récents dans Marché avancé de la gestion de la douleur du cancer

- En mai 2024, Tetra Bio-Pharma a avancé son médicament QIXLEEF aux essais de phase II, ciblant le soulagement de la douleur à base de cannabinoïdes pour les patients cancéreux avancés. Le médicament vise à offrir une option non opioïde pour la gestion de la douleur et améliorer la qualité de vie des patients.

- En mars 2024, Medlab Clinical Ltd s'est associée à Pharmascience Inc. pour développer et distribuer son médicament NanaBis à l'échelle mondiale et élargir ainsi l'accès aux traitements non opioïdes pour la prise en charge avancée de la douleur cancéreuse.

Marché avancé de la gestion de la douleur du cancer Segmentation

- Par catégorie de drogues

- Monoclonale Anticorps

- Cannabinoïde

- Aminoindane

- Par voie d'administration

- Voie intraveineuse

- Voie orale

- Voie sous-cutanée

- Voie intramusculaire

- Par canal de distribution

- Pharmacies hospitaliers

- Pharmacies en ligne

- Pharmacies de détail

Souhaitez-vous explorer l'option d'achat sections individuelles de ce rapport ?

Questions fréquemment posées :

Quelle est la taille du marché avancé de la gestion de la douleur cancéreuse?

La gestion avancée de la douleur du cancer au niveau mondial Le marché est évalué à 8,1 milliards de dollars en 2024 et devrait atteindre 12,9 milliards de dollars d'ici 2031.

Quel sera le TCAC du marché avancé de la gestion de la douleur du cancer?

Le TCAC du marché avancé de la gestion de la douleur du cancer devrait être de 5,6 % entre 2024 et 2031.

Quels sont les principaux facteurs à l'origine de la croissance du marché de la gestion avancée de la douleur cancéreuse?

La prévalence croissante du cancer avancé dans le monde, qui entraîne une demande accrue de solutions de gestion de la douleur et des progrès technologiques dans la mise au point de nouveaux traitements dérivés des cannabinoïdes pour la douleur du cancer. Ce sont les principaux facteurs à l'origine du marché avancé de la gestion de la douleur du cancer.

Quels sont les principaux facteurs qui entravent la croissance du marché avancé de la gestion de la douleur cancéreuse?

Les coûts élevés et les obstacles réglementaires associés à la mise au point de médicaments avancés pour la gestion de la douleur dans le cancer, ainsi que les effets secondaires potentiels et les problèmes réglementaires liés à l'utilisation d'opioïdes et de thérapies à base de cannabinoïdes. Ce sont là les principaux facteurs qui entravent la croissance du marché avancé de la gestion de la douleur cancéreuse.

Quelle est la première catégorie de médicaments sur le marché avancé de la gestion de la douleur du cancer?

Monoclonale L'anticorps est le premier segment de la classe des drogues.

Quels sont les principaux acteurs du marché avancé de la gestion de la douleur cancéreuse?

Tetra Bio-Pharma, Medlab Clinical Ltd, GW Pharmaceuticals, Pharmascience Inc., Pharma Cielo, Tilray Pharmaceuticals, WEX Pharmaceuticals, Pfizer, eurofins, Sigma-Aldrich, GSK plc, Recipharm sont les principaux acteurs.