Bone Metastasis in Solid Tumors Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2024 - 2031)

Bone Metastasis in Solid Tumors Market is segmented By Therapeutics (Bisphosphonates, Immunotherapies, Radiopharmaceuticals), By Diagnostics (Imaging,....

Bone Metastasis in Solid Tumors Market Size

Market Size in USD Bn

CAGR8.5%

| Study Period | 2024 - 2031 |

| Base Year of Estimation | 2023 |

| CAGR | 8.5% |

| Market Concentration | High |

| Major Players | Amgen Inc., Novartis AG, Pfizer Inc., Bayer AG, Johnson & Johnson Services, Inc. and Among Others. |

please let us know !

Bone Metastasis in Solid Tumors Market Analysis

The bone metastasis in solid tumors market is estimated to be valued at USD 3.8 billion in 2024 and is expected to reach USD 6.73 billion by 2031, growing at a compound annual growth rate (CAGR) of 8.5% from 2024 to 2031. The trend for bone metastasis in solid tumors indicates a rise in demand for precision therapies for effective treatment of bone metastases. Currently, most therapies focus on reducing tumor burden and managing associated pain.

Bone Metastasis in Solid Tumors Market Trends

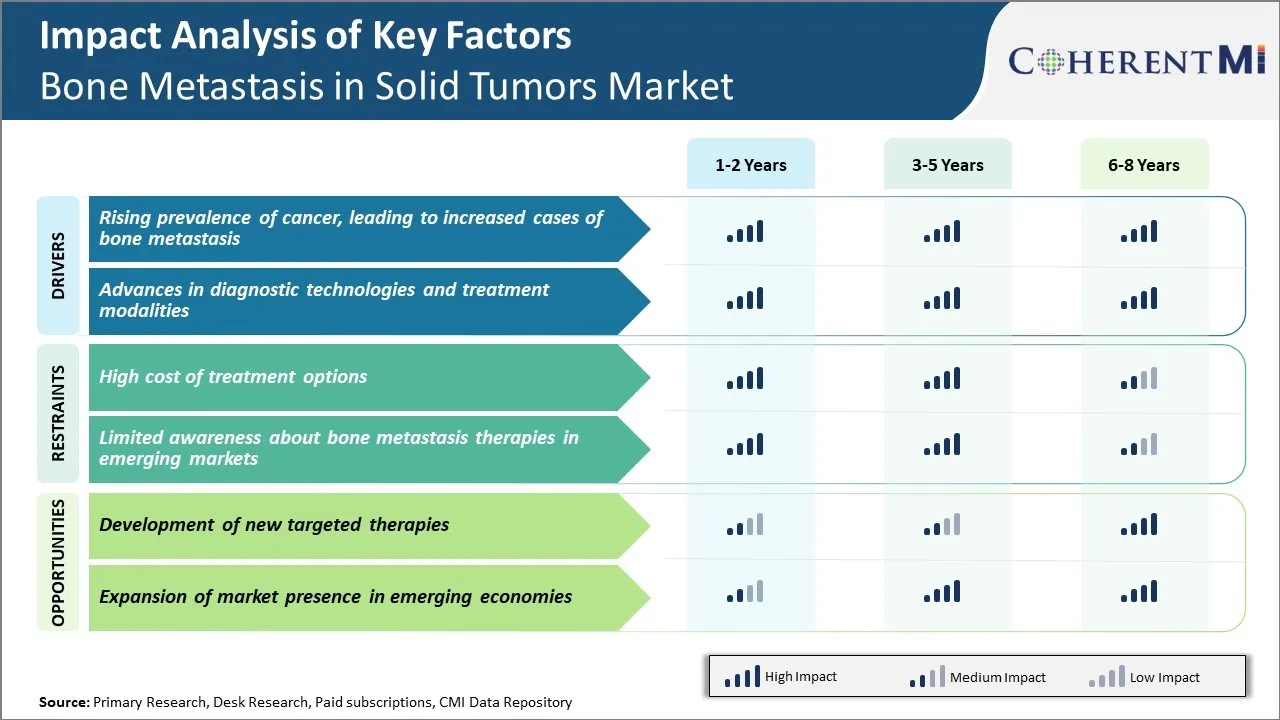

Market Driver - Rising Prevalence of Cancer, Leading to Increased Cases of Bone Metastasis

The increasing occurrence of cancer cases across the globe has led to a proportional rise in bone metastases. Rising obesity levels linked to unhealthy diets and lack of physical activity have major implications for cancers like breast and colorectal which demonstrate skeletal metastatic tendencies.

As bone is one of the most common sites for cancer cells to spread to from primary tumors located elsewhere in the body, a higher prevalence of cancer inevitably translates to greater instances of this deadly phenomenon. While cancers like breast, lung and prostate have long had a strong association with bone metastasis, newer data shows even some less common cancer types demonstrate a propensity to metastasize to the skeleton.

Overall, the compounding effects of an expanding and aging demographic profile coupled with surrounding societal trends mean primary cancer diagnoses will keep mounting. Due to the nature of this disease wherein cells can spread from the initial tumor site, even cancers with historically lower bone metastasis potentials may manifest this complication in greater frequency going forward among larger patient pools. With bones representing such a common secondary site, it is intuitive that bone metastasis case volumes must also rise proportionately.

Market Driver - Advances in Diagnostic Technologies and Treatment Modalities

Significant progress has been made in developing highly sensitive and specific methods to detect the presence as well as extent of bone metastases. Advanced imaging technologies like PET scans and whole-body MRI enable earlier and more accurate identification of sites involved compared to traditional modalities. Likewise, newer biomarker tests are improving abilities to monitor disease progression or recurrence in a minimally invasive manner.

Modern systemic therapies are also offering expanded options for interfering with the pathobiology of bone metastases. Improved variants of bisphosphonates and RANK ligand inhibitors offer enhanced skeletal protection against complications. Additionally, a diverse portfolio of molecularly-targeted drugs, immunotherapies and other novel agents provide opportunities to not just palliate pain but also potentially restrict further tumor growth and spread.

Alongside pharmacological interventions, minimally invasive image-guided techniques enable targeted treatment delivery. Options include radiotherapy, cryotherapy, vertebroplasty and kyphoplasty.

With continuing therapeutic refinement as well as expanding clinical experience, bone metastasis management protocols are becoming increasingly optimized. This stimulates demand for the various diagnostic tools, medications, and procedures applicable across the disease continuum from early identification to long-term management. Their cumulative impact drives growth of the overall bone metastasis in solid tumors market.

Market Challenge - High Cost of Treatment Options

The bone metastasis in solid tumors market faces significant challenges in the high cost of treatment options available. Current treatment approaches such as chemotherapy, radiation therapy, and supportive therapies like pain management medications often require long-term usage to effectively manage the complex symptoms of bone metastases. This long-term treatment burden leads to substantial costs not only for healthcare systems and payers but also out-of-pocket costs for patients.

The advanced staged nature of metastatic bone cancers also means that patients have generally exhausted initial line therapies worsening their condition and increasing treatment costs. Additionally, the lack of curative options necessitates palliative care and supportive treatments over extended periods driving up costs.

Furthermore, many bone metastasis patients are elderly who are often on fixed incomes, making it difficult for them to afford high treatment expenses. The high barrier to access effective therapies poses a major barrier to quality of life and clinical outcomes for bone metastasis patients.

Market Opportunity - Development of New Targeted Therapies

The ongoing active research and development of new targeted therapies represents a major opportunity to drive advances in the bone metastasis in solid tumors market. Recent improvements in understanding the molecular mechanisms underlying bone metastases have opened doors for more precisely targeting key pathways and processes involved.

Several biopharmaceutical companies are conducting clinical trials for novel targeted agents aimed at proteins like DLL4, NRP2, PD-1, and TGF-β among others that play roles in the formation of bone metastases. The successful development of effective and well-tolerated targeted therapies can transform treatment approaches by delivering superior outcomes compared to traditional options like chemotherapy.

New targeted options also promise more affordable and personalized treatment paradigms as precise molecular profiling help match the right patients to the most suitable targeted agents. This will go a long way in addressing the current market challenge of high costs of care. Moreover, targeted therapies are anticipated to demonstrate improved safety profiles over conventional cytotoxic drugs, enhancing patient quality of life.

Prescribers preferences of Bone Metastasis in Solid Tumors Market

Bone metastases are generally treated based on the stage and extent of disease. For early stage or localized bone metastasis, prescribers commonly start with non-opioid analgesics like acetaminophen as the first line of treatment to manage pain.

In cases where the pain is not adequately managed, prescribers typically switch to weaker opioid analgesics like tramadol as the second line of treatment. Brand names like Ultram are prescribed for its ability to relieve both pain and improve physical functioning.

For advances stages with increasing number of sites of bone metastasis, prescribers prefer stronger opioid analgesics like morphine as the third line of treatment. Extended-release formulations of morphine sulfate under brand names like Kadian are preferred to achieve round-the-clock pain relief.

Beyond analgesics, prescribers also utilize osteoplastics like Aredia (pamidronate) and Zometa (zoledronic acid) for their antiresorptive properties, especially in sites of high risk of skeletal complications. These intravenous bisphosphonates are administered on a monthly basis depending on kidney function tests.

Additionally, factors like performance status, prognosis, goals of care, side effect profile, insurance coverage and patient affordability influence the specific medication prescribed by oncologists and palliative care specialists for advanced bone metastatic cancers.

Treatment Option Analysis of Bone Metastasis in Solid Tumors Market

Bone metastasis is generally classified into 4 stages - asymptomatic, localized pain, functional impairment, and Spinal cord/bone pathology.

For early asymptomatic stages, the mainstay is bone-modifying agents like Denosumab and Bisphosphonates to prevent fractures. Denosumab is preferred due to its convenience of subcutaneous dosing every 4 weeks compared to intravenous Bisphosphonates.

As the disease progresses to localized bone pain, radiation therapy can provide effective pain palliation. Stereotactic Body Radiotherapy or SBRT allows delivery of a high dose of radiation precisely to the tumour site in 1-5 sessions, minimizing damage to surrounding healthy tissues.

For advanced stages with functional impairment, chemotherapy may be added for its antitumor effects. The PARP inhibitor Olaparib tablets provide a well-tolerated oral treatment option for prostate or breast cancer patients with BRCA mutations. Docetaxel or Cabazitaxel infusion combined with Denosumab is a common backbone regimen to reduce fractures as well as delay disease progression.

The final stage with spinal cord/bone compression often requires surgical intervention for decompression and stabilization in addition to the above treatments. Radium-223 dichloride, a novel alpha-emitting radiopharmaceutical, has shown overall survival benefits for castration-resistant prostate cancer patients with symptomatic bone metastases by targeting bone tissues while sparing the marrow.

Key winning strategies adopted by key players of Bone Metastasis in Solid Tumors Market

Collaboration for drug development has been a popular strategy adopted by leading players to advance their pipeline of drugs for bone metastasis treatment. For example, Novartis partnered with MorphoSys in 2018 to develop and commercialize MOR202/TJ202, an anti-CD38 antibody for multiple myeloma treatment including bone lesions. This allows both companies to leverage their collective R&D capabilities and resources.

Acquisitions is another strategy used to expand product portfolios and capabilities. For example, in 2018, Bayer acquired BlueRock Therapeutics to gain access to BlueRock's cell therapy platform and pipeline of treatments targeting several hard-to-treat conditions causing bone metastases. This strengthened Bayer's oncology portfolio.

Customized drug delivery systems have proven effective at improving outcomes. Merck & Co adopted this strategy with their FDA-approved drug called SIMPONI ARIA which uses sophisticated identity recognition to deliver customized treatment directly to disease sites like bone metastases.

Launching biomarker companion diagnostic tests along with drugs helps identify patients most likely to respond. For example, Clovis Oncology co-developed the FIGHT diagnostic test to select prostate cancer patients with DNA repair defects for their PARP inhibitor Rubraca. This improved patient selection increased the drug's response rate from 19% to 56%, demonstrating the commercial and clinical value of such companion diagnostic strategies.

Segmental Analysis of Bone Metastasis in Solid Tumors Market

Insights, By Therapeutics: >Bisphosphonates Witnesses a Rise in Adoption across End Users

In terms of therapeutics, bisphosphonates contribute the highest share of the market owing to its widespread adoption across end-users for the management of cancer-related bone diseases. Bisphosphonates are analogs of inorganic pyrophosphate that bind strongly to the bone mineral hydroxyapatite. This binding allows bisphosphonates to effectively reduce osteoclast activity and consequently bone resorption. The anti-resorptive properties of bisphosphonates have proven highly effective in relieving cancer-related skeletal complications such as bone pain, hypercalcemia, pathological fractures, and spinal cord compression. Bisphosphonates are also found to reduce the incidence of bone complications in patients with various solid tumors affecting the bone including breast cancer and prostate cancer. The easy administration and low cost of bisphosphonates compared to alternative therapeutics have spurred their adoption across hospitals, cancer care centers, and clinics. Wide physician recommendation and patient preference for bisphosphonates over other therapeutic classes also contribute to the segment's high value share.

Insights, By Diagnostics: Imaging Dominates Diagnostics with Wide Application in Detecting Skeletal Lesions

In terms of diagnostics, imaging contributes the highest share of the market due to its ability to accurately detect skeletal lesions associated with bone metastasis. Imaging techniques such as X-ray, computed tomography (CT), nuclear medicine scans (bone scan), and magnetic resonance imaging (MRI) enable the visualization of destructive bone changes that occur as a result of metastatic cancer cells affecting the skeleton. X-rays and CT scans are highly effective in identifying osteolytic or osteoblastic lesions characteristic of cancer metastasis in bone.

However, nuclear bone scans and MRI offer higher sensitivity in detecting bone involvement, especially at an early stage. The non-invasive nature and widespread accessibility of imaging modalities have cemented their role as the standard of care for initial identification and subsequent monitoring of bone metastasis. Advances in imaging technologies with improved resolution and fewer side effects also support continued dominance of the segment.

Insights, By Treatment Option: Surgery Drives Treatment Driven by Capacity to Improve Quality of Life

In terms of treatment option, surgery contributes the highest share of the market owing to its ability to improve patients' quality of life. Surgical intervention plays a vital palliative role in the management of metastatic bone diseases caused by solid tumors.

Surgical procedures aid in stabilizing fractures, correcting spinal deformities, restoring mobility by replacing fractured bones, and alleviating persistent pain associated with bone metastasis. Such pain relief and restoration of motor functions has proven crucial in bolstering patients' quality of life during advanced cancer stages. The capacity of surgical approaches to address aggressive skeletal complications more effectively than alternative options also drives its adoption.

The rising number of specialized cancer orthopedic surgeons and expansion of surgical oncology further supports the segment's growth. In addition, advancements in minimally invasive techniques and localized therapies have eased surgical intervention, contributing to the treatment segment's high market value share.

Competitive overview of Bone Metastasis in Solid Tumors Market

The major players operating in the Bone Metastasis in Solid Tumors Market include Amgen Inc., Novartis AG, Pfizer Inc., Bayer AG, and Johnson & Johnson Services, Inc.

Bone Metastasis in Solid Tumors Market Leaders

- Amgen Inc.

- Novartis AG

- Pfizer Inc.

- Bayer AG

- Johnson & Johnson Services, Inc.

Bone Metastasis in Solid Tumors Market - Competitive Rivalry, 2024

Bone Metastasis in Solid Tumors Market

(Dominated by major players)

(Highly competitive with lots of players.)

Recent Developments in Bone Metastasis in Solid Tumors Market

- In June 2024, Amgen Inc. announced the development of a new immunotherapy targeting bone metastases in prostate cancer, which is expected to improve survival rates by 20%. This development represents a significant advancement in personalized treatment options. Amgen Inc. is actively working on novel immunotherapies for advanced prostate cancer, specifically targeting bone metastases, which is a common and challenging progression in this disease. Their investigational BiTE (bispecific T-cell engager) therapies, such as AMG 160 and AMG 212, are showing promise in early clinical trials.

- In April 2024, Novartis AG partnered with a leading diagnostics company to enhance bone metastasis imaging technologies, enabling earlier detection and treatment planning. Novartis has been actively involved in the development of radiopharmaceuticals, including imaging agents like Locametz®, which is used to identify prostate cancer metastasis through advanced imaging techniques. These efforts align with Novartis' broader focus on improving diagnostic capabilities for metastatic cancers, including those involving bone

Bone Metastasis in Solid Tumors Market Segmentation

- By Therapeutics

- Bisphosphonates

- Immunotherapies

- Radiopharmaceuticals

- By Diagnostics

- Imaging

- Biomarker Testing

- Biopsy

- By Treatment Option

- Surgery

- Radiation Therapy

- Chemotherapy

- By Disease Management

- Pain Management

- Rehabilitation

Would you like to explore the option of buying individual sections of this report?

Frequently Asked Questions :

How big is the bone metastasis in solid tumors market?

The bone metastasis in solid tumors market is estimated to be valued at USD 3.8 billion in 2024 and is expected to reach USD 6.73 billion by 2031.

What are the key factors hampering the growth of the bone metastasis in solid tumors market?

The high cost of treatment options and limited awareness about bone metastasis therapies in emerging markets are the major factors hampering the growth of the bone metastasis in solid tumors market.

What are the major factors driving the bone metastasis in solid tumors market growth?

The rising prevalence of cancer, which leads to increased cases of bone metastasis, and advances in diagnostic technologies and treatment modalities are the major factors driving the bone metastasis in solid tumors market.

Which are the leading therapeutics in the bone metastasis in solid tumors market?

The leading therapeutics segment is bisphosphonates.

Which are the major players operating in the bone metastasis in solid tumors market?

Amgen Inc., Novartis AG, Pfizer Inc., Bayer AG, and Johnson & Johnson Services, Inc. are the major players.

What will be the CAGR of the bone metastasis in solid tumors market?

The CAGR of the bone metastasis in solid tumors market is projected to be 8.5% from 2024-2031.