Pertussis Therapeutic Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Pertussis Therapeutic Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Pertussis Therapeutic Market is segmented By Clinical Stages of Development (Late Stage Products, Mid-Stage Products, Early-Stage Products, By Route of Administration (Oral, Intravenous, Subcutaneous, Parenteral, Topical), By Geography (North America, Latin America, Asia Pacific, Europe, Middle East, and Africa). The report offers the value (in USD Billion) for the above-mentioned segments.

Pertussis Therapeutic Market is segmented By Clinical Stages of Development (Late Stage Products, Mi...

Pertussis Therapeutic Market Size - Analysis

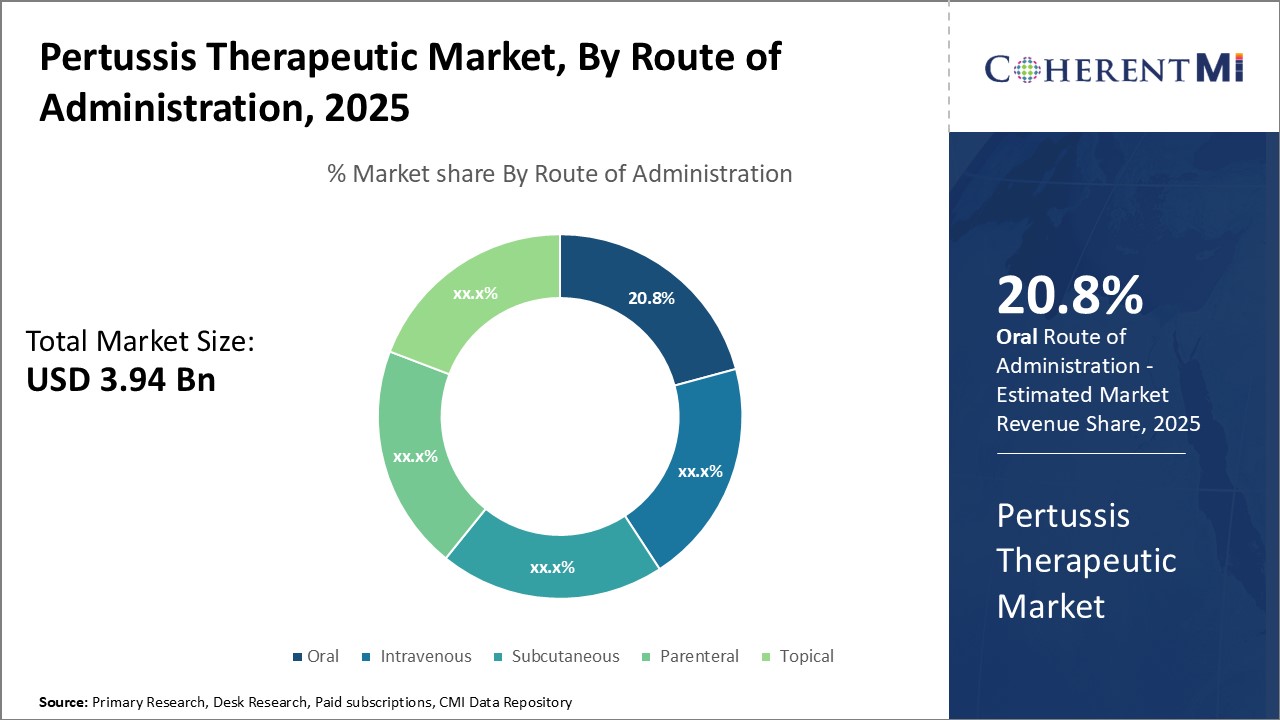

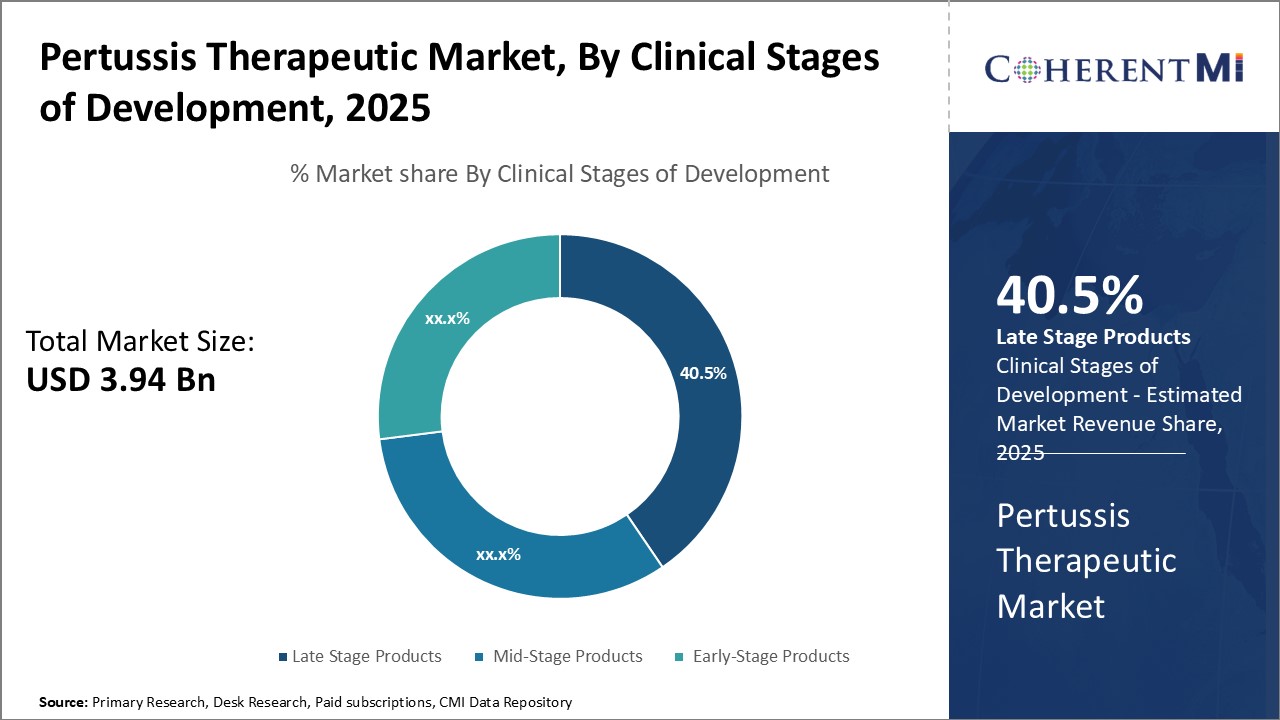

The pertussis therapeutic market is estimated to be valued at USD 3.94 Bn in 2025 and is expected to reach USD 5.05 Bn by 2032, growing at a compound annual growth rate (CAGR) of 3.6% from 2025 to 2032. The market has been witnessing steady growth over the past few years driven by high prevalence of pertussis across the globe.

Market Size in USD Bn

CAGR3.6%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

3.6%

Market Concentration

High

Major Players

Tianjin CanSino Biotechnology, ILiAD Biotechnologies, GlaxoSmithKline (GSK), Sanofi, AstraZeneca and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

Pertussis Therapeutic Market Trends

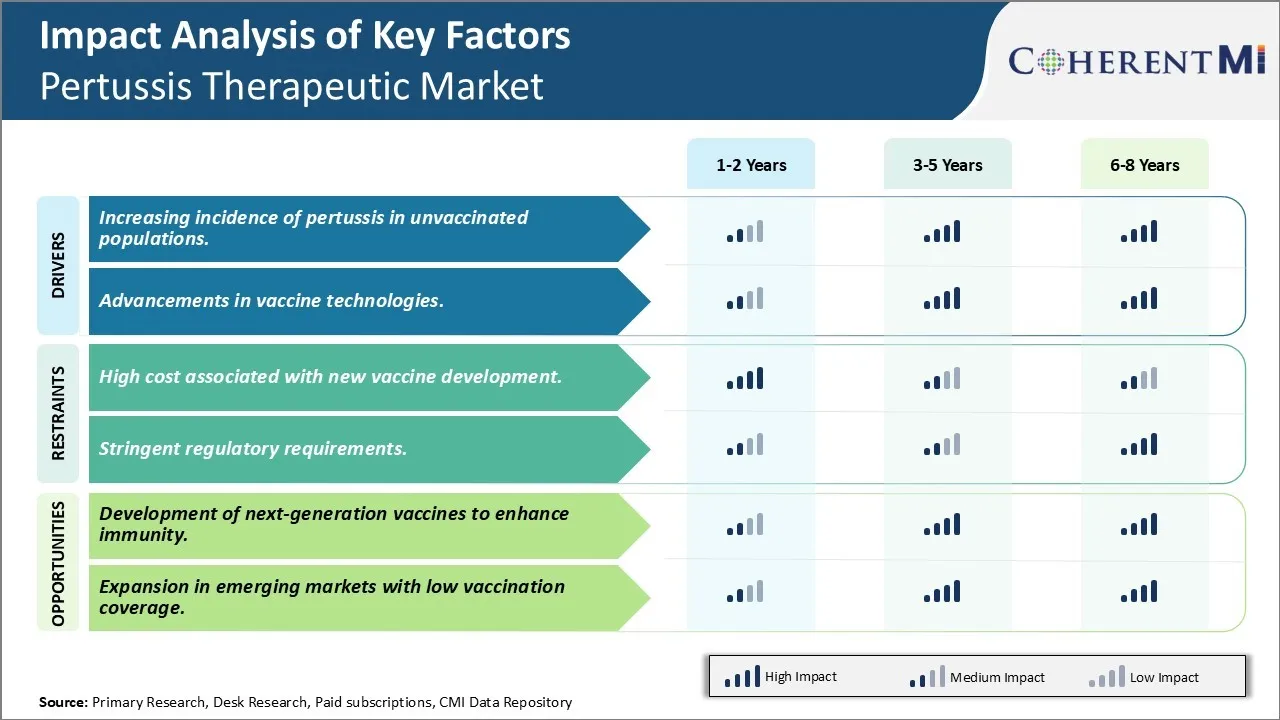

Market Driver - Increasing incidence of pertussis in unvaccinated populations

The resurgence of pertussis or whooping cough in the past decade, especially among unvaccinated populations has been a major concern for global public health experts. While pertussis vaccines have dramatically reduced cases in the late 20th century, recent years have witnessed an increase in reported pertussis cases. This rise has predominantly been among children, teenagers as well as adults who were unvaccinated or whose immunity has waned over time. The heightened vulnerability of unvaccinated populations is driving a potential demand for improved preventive options against this disease.

According to CDC reports, the last pertussis epidemic occurred from 2004–2005 and 2019–2020 has seen a sharp uptick in cases across several parts of United States. Many pediatricians point towards smaller percentage of children receiving timely vaccination as the likely cause. Several developed nations too have reported higher incidence among school going children and teenagers. The World Health Organization data suggests that global circulation of pertussis is widespread and disease transmission remains high in many communities despite vaccine coverage being adequate as per standards.

Market Driver - Advancements in vaccine technologies

Vaccine research has made immense progress in past decades; however pertussis vaccine technology has limitations like transient immunity which needs addressing. Scientists are constantly working towards enhancing vaccine performance. Several innovative vaccine platforms and antigen design strategies are being studied that can expedite the development of next generation pertussis vaccines.

One key area of research is developing acellular vaccines combining genetically engineered pertussis toxin mutants with other antigens. Genetic engineering allows production of non- or less-toxic mutants that are suitable as vaccine components. Combining these with immunostimulants holds promise to enhance the magnitude and quality of immune responses. Adjuvanted recombinant vaccines made of multiple antigen components conjugated to immunopotentiators are anticipated to induce improved protection.

Next-generation approaches like reverse vaccinology based on genomic sequences are utilized for identifying novel antigens. Studies have revealed proteins like BrkA, Vag8/9, FHA2 as potential candidates and various combinations are tested for synergistic effects. Newer technologies like protein structure prediction, in silico antigen design aid selection of epitopes that can pack maximum immunogenic firepower.

Market Challenge - High cost associated with new vaccine development

One of the key challenges faced in the pertussis therapeutic market is the high cost associated with new vaccine development. Developing a new vaccine requires extensive research and clinical trials to ensure safety and efficacy. This vaccine development process involves long periods of research, testing, regulatory review and approvals. It typically takes 10-15 years for a vaccine candidate to progress from discovery to regulatory approval and introduction in the market. Significant investments are required at each stage of vaccine R&D which pushes up the overall costs. The high capital requirements and risk of failure add to the costs. Additionally, the specialized equipment, facilities and skilled researchers required to develop vaccines add to their production costs. Stringent regulations related to vaccine safety and quality assurance further increase compliance costs for manufacturers. Unforeseen delays or regulatory roadblocks during clinical trials or approvals can significantly increase the costs beyond initial estimates. The incurred costs have to be recovered through final vaccine prices making new vaccines expensive for public health programs in resource constrained markets.

Market Opportunity - Development of next-generation vaccines to enhance immunity

One major opportunity in the pertussis therapeutic market is the development of next-generation vaccines that provide enhanced and longer lasting immunity. Currently available whole cell and acellular pertussis vaccines have limited durability of protection with immunity waning within 5-10 years post vaccination necessitating booster doses. There exists a need for vaccines that induce strong and long lasting immune memory against Bordetella pertussis. Novel conjugate, subunit, recombinant, live-attenuated and mRNA based vaccine platforms are being researched that can stimulate both cell mediated and neutralizing antibody immune responses through precision targeting of virulence factors. Advanced vaccine design approaches incorporating multiple antigens, immune potentiators and novel delivery methods hold promise to induce durable protective immune responses after fewer doses or a single dose vaccination. Development of vaccines that provide lifelong immunity or protection beyond childhood could reduce disease burden significantly and cut healthcare costs related to repeated vaccinations. Next-generation pertussis vaccines also provide opportunities for combination vaccines that protect against multiple respiratory illnesses.

Key winning strategies adopted by key players of Pertussis Therapeutic Market

GlaxoSmithKline has been the market leader in pertussis vaccines for decades due to its effective product differentiation strategy. In the 1990s, when efficacy of whole-cell pertussis vaccines started declining, GSK developed the acellular pertussis vaccine called Infanrix. This vaccine used purified pertussis antigens instead of whole killed bacteria. Clinical trials showed Infanrix had a better safety profile with fewer side effects compared to whole-cell vaccines. It received FDA approval in 1996 and quickly captured over 70% of the US pediatric pertussis market.

Sanofi adopted a dual strategy of collaboration and acquisition to strengthen its position. In 2008, it partnered with Biological E to develop an affordable acellular pertussis vaccine for developing countries. This vaccine was launched in India in 2015. Around the same time, Sanofi acquired Protein Sciences Corporation, which had developed an acellular vaccine candidate called SHIP. SHIP showed promise in clinical trials and was acquired by Sanofi to accelerate its development and marketing.

Mitsubishi Tanabe Pharma focused its strategy on the adolescent and adult vaccination market, which was largely untapped until recently. It developed Tdap vaccines like Infanrix IPV and Boostrix that protect against tetanus, diphtheria and pertussis. Clinical trials in Japan showed these vaccines induced strong immune responses and were well-tolerated.

Segmental Analysis of Pertussis Therapeutic Market

Insights, By Clinical Stages of Development: Late stage products (Phase III) sub-segment contributes the highest share

In terms of clinical stages of development, late stage products (Phase III) sub-segment contributes the highest share of 40.5% in the market owing to their proximity to commercialization. Products in late-stage clinical trials have demonstrated safety and efficacy, having passed Phase I and Phase II testing. This significantly de-risks their development timeline and increases the probability of regulatory approval compared to earlier-stage programs.

Companies prioritize advancing their late-stage assets because of this lower risk profile. Significant resources have already been invested in products that have reached Phase III testing. Successfully completing large, late-stage clinical trials and gaining approval represents the potential payoff on these sizable investments. It also means these products are closer to generating revenue from product sales.

The large patient populations enrolled in Phase III tests further refine appropriate positioning, dosing, and maximize understanding of a drug's performance. This late optimization improves the product profile and helps companies communicate a clear value proposition to prescribers and payers. It establishes well-defined commercial and reimbursement strategies prior to approval and launch.

Insights, By Clinical Stages of Development: Oral Administration Dominance

In terms of route of administration, the oral sub-segment contributes the highest share of 20.8% owing to preferences for convenient dosing forms among patients and prescribers. Oral drug delivery provides simplicity compared to options like injections that require syringes or intravenous administration done in clinical settings.

Convenience is a key factor influencing patient access and medication adherence. People are more likely to correctly and consistently take oral medications as directed versus treatments requiring visiting medical facilities or healthcare professionals for administration. This enhances clinical outcomes and lowers healthcare costs from improved adherence and fewer misreported doses.

Oral drugs also empower patients to self-administer therapy as needed, such as promptly starting treatment after potential exposure. This facilitates faster response times compared to treatments reliant on third-party administration. It increases the control patients feel over managing their condition.

From the prescriber perspective, oral medications are also more conformable to recommend long-term for asymptomatic carriers and immune compromised patients at higher risk of Pertussis. Simpler dosing translates to greater prescription volumes driven by the user-friendly nature and reliable outcomes of oral delivery.

Competitive overview of Pertussis Therapeutic Market

The major players operating in the pertussis therapeutic market include Tianjin CanSino Biotechnology, ILiAD Biotechnologies, GlaxoSmithKline (GSK), Sanofi, AstraZeneca, Pfizer, Merck & Co., Mitsubishi Tanabe Pharma, Serum Institute of India, and Dynavax Technologies.

Pertussis Therapeutic Market Leaders

Tianjin CanSino Biotechnology

ILiAD Biotechnologies

GlaxoSmithKline (GSK)

Sanofi

AstraZeneca

*Disclaimer: Major players are listed in no particular order.

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Pertussis Therapeutic Market

In August 2023, Tianjin CanSino Biotechnology initiated Phase III trials for DTcP Infant vaccine. This step is crucial for domestic market entry and reducing dependency on imported vaccines.

ILiAD Biotechnologies is conducting clinical trials for BPZE1, a next-gen pertussis vaccine, aiming to block the colonization of B. pertussis in nasal passages, reducing transmission and disease incidence.

Pertussis Therapeutic Market Report - Table of Contents

RESEARCH OBJECTIVES AND ASSUMPTIONS

Research Objectives

Assumptions

Abbreviations

MARKET PURVIEW

Report Description

Market Definition and Scope

Executive Summary

Pertussis Therapeutic Market, By Clinical Stages of Development

Pertussis Therapeutic Market, By Route of Administration

Coherent Opportunity Map (COM)

MARKET DYNAMICS, REGULATIONS, AND TRENDS ANALYSIS

Market Dynamics

Impact Analysis

Key Highlights

Regulatory Scenario

Product Launches/Approvals

PEST Analysis

PORTER’s Analysis

Merger and Acquisition Scenario

Global Pertussis Therapeutic Market, By Clinical Stages of Development, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Late Stage Products (Phase III)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Mid-Stage Products (Phase II)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Early-Stage Products (Phase I)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Pertussis Therapeutic Market, By Route of Administration, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Oral

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Intravenous

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Subcutaneous

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Parenteral

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Topical

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Pertussis Therapeutic Market, By Region, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Clinical Stages of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

U.S.

Canada

Latin America

Introduction

Market Size and Forecast, By Clinical Stages of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

Brazil

Argentina

Mexico

Rest of Latin America

Europe

Introduction

Market Size and Forecast, By Clinical Stages of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

Germany

U.K.

Spain

France

Italy

Russia

Rest of Europe

Asia Pacific

Introduction

Market Size and Forecast, By Clinical Stages of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

China

India

Japan

Australia

South Korea

ASEAN

Rest of Asia Pacific

Middle East

Introduction

Market Size and Forecast, By Clinical Stages of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

GCC Countries

Israel

Rest of Middle East

Africa

Introduction

Market Size and Forecast, By Clinical Stages of Development , 2020-2032, Value (USD Bn)

Market Size and Forecast, By Route of Administration , 2020-2032, Value (USD Bn)

South Africa

North Africa

Central Africa

COMPETITIVE LANDSCAPE

Tianjin CanSino Biotechnology

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

ILiAD Biotechnologies

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

GlaxoSmithKline (GSK)

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Sanofi

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

AstraZeneca

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Pfizer

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Merck & Co.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Mitsubishi Tanabe Pharma

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Serum Institute of India

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Dynavax Technologies

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analyst Recommendations

Wheel of Fortune

Analyst View

Coherent Opportunity Map

References and Research Methodology

References

Research Methodology

About us

Pertussis Therapeutic Market Segmentation

By Clinical Stages of Development

Late Stage Products (Phase III)

Mid-Stage Products (Phase II)

Early-Stage Products (Phase I)

By Route of Administration

Oral

Intravenous

Subcutaneous

Parenteral

Topical

Would you like to explore the option of buying individual sections of this report?

About author

Ghanshyam Shrivastava - With over 20 years of experience in the management consulting and research, Ghanshyam Shrivastava serves as a Principal Consultant, bringing extensive expertise in biologics and biosimilars. His primary expertise lies in areas such as market entry and expansion strategy, competitive intelligence, and strategic transformation across diversified portfolio of various drugs used for different therapeutic category and APIs. He excels at identifying key challenges faced by clients and providing robust solutions to enhance their strategic decision-making capabilities. His comprehensive understanding of the market ensures valuable contributions to research reports and business decisions.

Ghanshyam is a sought-after speaker at industry conferences and contributes to various publications on pharma industry.

Frequently Asked Questions :

How big is the Pertussis Therapeutic Market?

The Pertussis Therapeutic Market is estimated to be valued at USD 3.94 Bn in 2025 and is expected to reach USD 5.05 Bn by 2032.

What are the major factors driving the pertussis therapeutic market growth?

The increasing incidence of pertussis in unvaccinated populations and advancements in vaccine technologies are the major factors driving the pertussis therapeutic market.

Which is the leading clinical stages of development in the pertussis therapeutic market?

The leading clinical stages of development segment is late stage products (Phase III).

Which are the major players operating in the pertussis therapeutic market?

Tianjin CanSino Biotechnology, ILiAD Biotechnologies, GlaxoSmithKline (GSK), Sanofi, AstraZeneca, Pfizer, Merck & Co., Mitsubishi Tanabe Pharma, Serum Institute of India, and Dynavax Technologies are the major players.

What will be the CAGR of the pertussis therapeutic market?

The CAGR of the pertussis therapeutic market is projected to be 3.6% from 2025-2032.

What are the key factors hampering the growth of the pertussis therapeutic market?

The high cost associated with new vaccine development and stringent regulatory requirements are the major factors hampering the growth of the pertussis therapeutic market.

Missing comfort of reading report in your local language? Find your preferred language :

Insights, By Clinical Stages of Development: Late stage products (Phase III) sub-segment contributes the highest share

Insights, By Clinical Stages of Development: Late stage products (Phase III) sub-segment contributes the highest share