Power Semiconductor Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Power Semiconductor Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Power Semiconductor Market is segmented By Component (Power Integrated Circuits, Discrete, Module), By Material (Silicon/Germanium, Silicon Carbide, Gallium Nitride), By End-user Industry (Automotive Industry, Consumer Electronics Industry, Military and Aerospace Industry, IT and Telecommunication Industry, Industrial Industry, Other End-User Industries), By Geography (North America, Latin America, Asia Pacific, Europe, Middle East, and Africa). The report offers the value (in USD billion) for the above-mentioned segments.

Power Semiconductor Market is segmented By Component (Power Integrated Circuits, Discrete, Module), ...

Power Semiconductor Market Size - Analysis

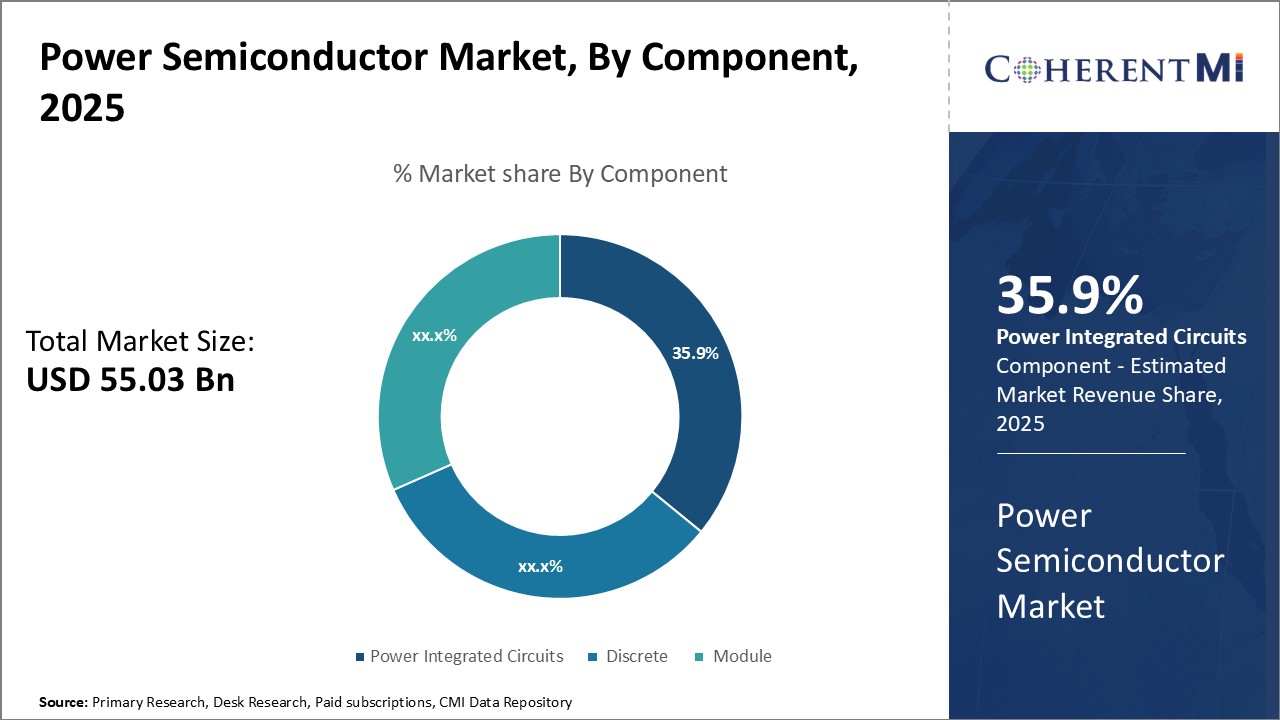

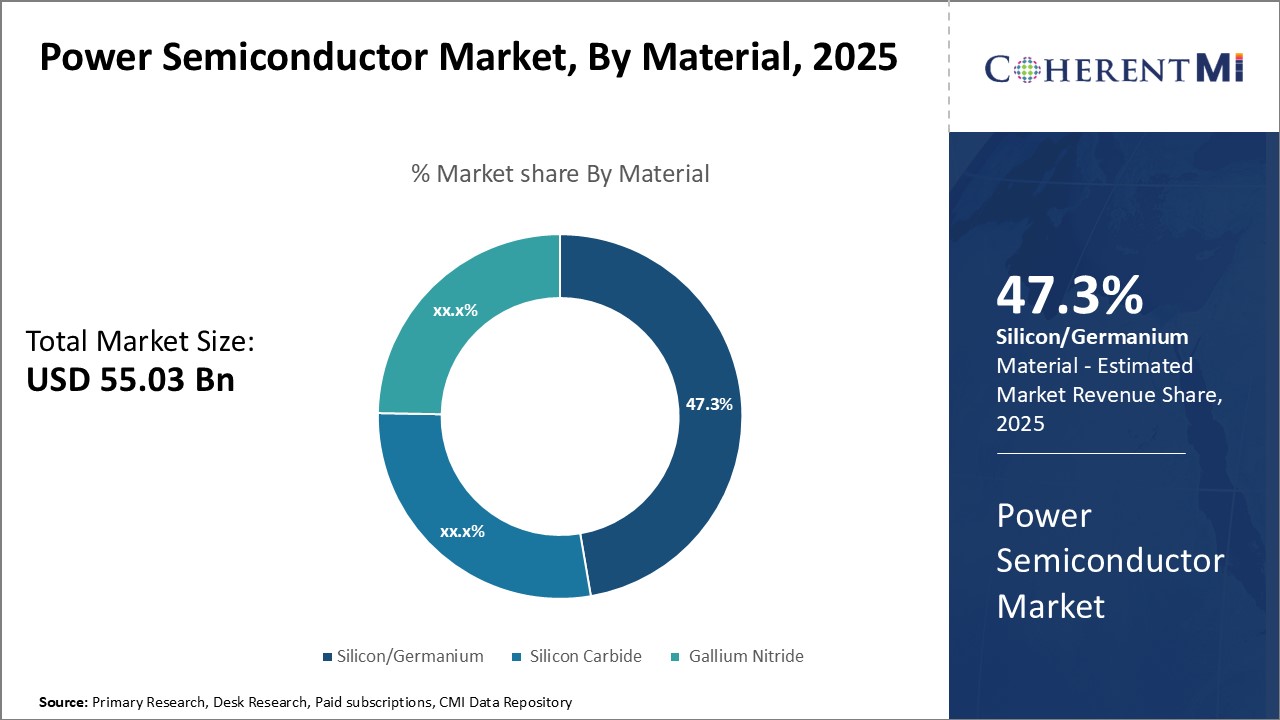

The power semiconductor market is estimated to be valued at USD 55.03 Bn in 2025 and is expected to reach USD 75.90 Bn by 2032, growing at a compound annual growth rate (CAGR) of 4.7% from 2025 to 2032. Key drivers of the power semiconductor market include growing adoption of electric and hybrid vehicles coupled with increasing penetration of smart grids and smart homes.

Market Size in USD Bn

CAGR4.7%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

4.7%

Market Concentration

Medium

Major Players

Infineon Technologies AG, Texas Instruments Inc., STMicroelectronics NV, Toshiba Corporation, Mitsubishi Electric Corporation and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

Power Semiconductor Market Trends

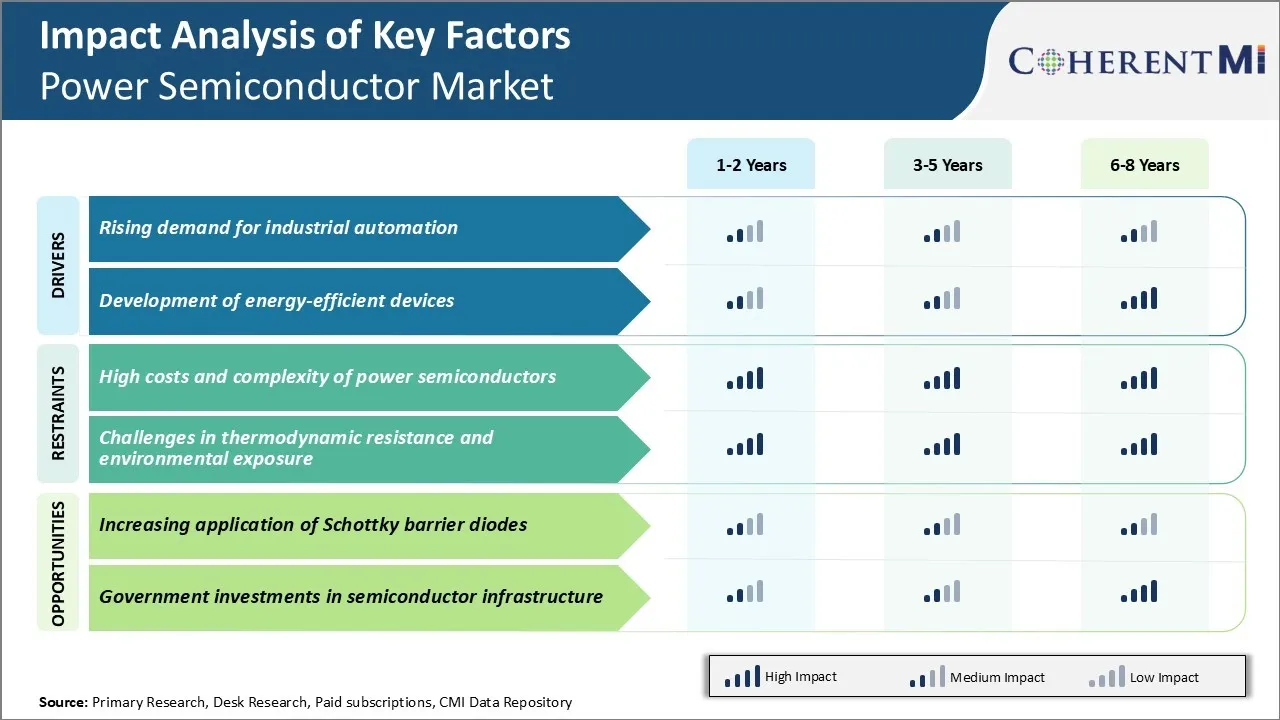

Market Driver - Rising Demand for Industrial Automation

Integration of automation across industries is increasing in order to optimize productivity and reduce costs. Thereby, the demand for power semiconductors that control and regulate industrial automation equipment has seen a significant rise. Many manufacturing plants have highly complex automated production lines equipped with machines, robots, and sensors that require power semiconductors to function properly.

The packaging industry has benefited hugely from automation with robots performing arduous and repetitive tasks like packing boxes at high speed. Similarly, automotive manufacturers are automating vehicle production lines to achieve mass production capabilities. Activities like welding, painting, and assembly that were previously done manually are now controlled by robots and other automated equipment powered by semiconductors. This has led OEMs to focus on building smart, connected factories of the future with end-to-end automation requiring advanced power devices. Other industries like food & beverage processing, plastic manufacturing, electronics assembly are also automating to improve productivity through 24/7 operations and meeting rising consumer demand.

Market Driver - Development of Energy-efficient Devices

With growing environmental concerns around the world, there is a strong push for reducing energy consumption and transitioning to cleaner sources of power. This presents a massive opportunity for power semiconductor manufacturers to develop more energy-efficient devices that can help optimize energy usage.

Consumer electronic devices like laptops and smart phones that people use daily rely on compact power management ICs containing efficient gallium nitride or silicon carbide transistors. In industries, switching from conventionally inefficient motor drive systems or linear power supplies to devices utilizing wide bandgap semiconductors can substantially cut energy bills. GaN and SiC power modules deliver higher power densities at much smaller sizes and lower power losses during operation.

As environmental consciousness rises globally and energy efficiency becomes a deciding factor, semiconductor companies will look to continuously enhance their wide bandgap offerings. Continuous R&D is focused on improving device performance metrics like lower on-resistance, higher breakdown voltage and higher operating temperatures. Such innovation will accelerate the growth of green applications and drive greater power semiconductor market revenues.

Market Challenge - High Costs and Complexity of Power Semiconductors

The power semiconductor market faces significant challenges due to the high costs and complexity associated with power semiconductors. Power semiconductors cater to industries with high power requirements such as automotive, industrial motors, and renewable energy.

However, producing power semiconductors involves complex manufacturing processes that utilize expensive raw materials like silicon carbide and gallium nitride. This makes power semiconductor devices more costly compared to regular semiconductors used in consumer electronics.

Additionally, intricate cooling mechanisms are required to dissipate heat generated during operation. The cooling systems add further to production expenses. The technical complexities also mean longer development cycles for new power semiconductor designs. This high level of complexity poses significant barriers for companies working in the power semiconductor market.

Market Opportunity - Increasing Application of Schottky Barrier Diodes

The power semiconductor market provides opportunities for companies focused on new device types and materials. One such technology gaining prominence is Schottky Barrier Diodes (SBDs). Their ability to function at high switching frequencies also provides design advantages over other alternatives. These benefits have led to increasing application of SBDs across various industries that rely on power management and conversion

In electric vehicles, SBDs allow more compact and effective onboard chargers. They are also facilitating more efficient wireless charging systems. With electrification trends accelerating globally, the demand for power conversion and management is growing rapidly.

This growing requirement provides a massive opportunity for wider usage of SBDs across different applications involved in new energy systems. Companies developing advanced SBDs using wide bandgap materials can gain significantly in the power semiconductor market.

Key winning strategies adopted by key players of Power Semiconductor Market

Strategy 1: Product innovation through continuous R&D investments

Infineon introduced its latest CoolSiC MOSFETs in 2018 which offer 30% lower switching and conduction losses compared to traditional silicon MOSFETs.

Strategy 2: Strategic acquisitions to expand product portfolio

In 2016, ON Semiconductor acquired Fairchild Semiconductor to enhance its power and analog solutions. This strengthened ON's position in automotive, industrial, and mobile markets.

Strategy 3: Focus on fast growing electric vehicle and renewable energy sectors

STMicroelectronics ramped up Silicon Carbide wafer production capacity from 4" to 6" between 2015-2019 to cash in on the rising EV market.

Strategy 4: Establishing strategic partnerships and supply agreements

In 2018, Mitsubishi entered a 5-year strategic partnership and a multi-year supply agreement with Renesas for automotive microcontrollers.

Segmental Analysis of Power Semiconductor Market

Insights, By Component: Power Integrated Circuits - Rise of System on Chip (SoC) Designs

In terms of component, power integrated circuits contributes 35.9% share of the power semiconductor market in 2025. This is owning to increasing demand for System on Chip (SoC) designs across various industries. Power integrated circuits incorporate power management and power saving systems on a single substrate which is ideal for applications requiring miniaturization of components.

The automotive industry has seen tremendous growth in demand for advanced driver-assistance systems (ADAS) that depend on power efficient SoC designs. This has boosted the market for power ICs as they integrate vital functions like voltage regulation, battery charging and power factor correction onto one silicon chip. Similarly, the proliferation of smart appliances and Internet-of-Things (IoT) devices has fueled the need for low power and multifunctional chips.

With growing digitization across sectors, the scope for customized power SoC designs combining logic, analog and power management features remains high. This presents an ongoing lucrative opportunity for power IC vendors in the coming years.

Insights, By Material: Ascendance of Wide Bandgap Materials

In terms of material, silicon/germanium contributes 47.3% share of the power semiconductor market in 2025. However, Silicon Carbide (SiC) and Gallium Nitride (GaN) based power semiconductors are gaining rapid acceptance due to their superior material properties compared to traditional Silicon. SiC devices can operate at much higher voltages, currents and temperatures than silicon. They reduce power losses significantly which makes them ideal for power conversion in electric vehicles, fast charging stations, renewable energy equipment and other similar applications.

Meanwhile, GaN semiconductors provide even higher efficiency than SiC at higher switching frequencies. They combine very low on-resistance with high breakdown voltage. The compact size of GaN components allows for more powerful and smaller power supplies. With continuous advancements in SiC and GaN semiconductor manufacture, their use is growing remarkably creating lasting demand shift from silicon over time.

Insights, By End-user Industry: Stimulation from Clean Energy Transition

In terms of end-user industry, automotive industry contributes the highest share currently driven by surging electric vehicle production worldwide. However, the Industrial Industry sector is emerging as a major end-user with progressive commitment towards carbon neutrality. Nations and corporations have outlined ambitious targets and timelines to shift towards cleaner sources of energy such as solar and wind power. This calls for robust power electronic systems for energy conversion, transmission and storage.

The growing commercial and utility-scale integration of renewables is thus stimulating power semiconductor consumption considerably. Semiconductor manufacturers are actively innovating product portfolios aligned with the technical needs of green energy industries. With the clean energy transition gathering momentum on a global scale, the industrial sector is expected to sustain high demands for power devices in the upcoming years.

Additional Insights of Power Semiconductor Market

Adoption of SiC in Electric Vehicles: Companies like Tesla have integrated SiC power semiconductors in their vehicles, improving efficiency and driving range.

5G Infrastructure Expansion: Deployment of 5G networks increases demand for power semiconductors capable of handling higher frequencies and power levels.

Automotive Sector Contribution: The sector accounts for 31.4% of the power semiconductor market, primarily due to the EV boom.

Asia-Pacific Market Share: Holds approximately 42.7% of the global power semiconductor market, attributed to manufacturing hubs and consumer base.

Shift Towards Renewable Energy: Investments in renewable energy are projected to increase power semiconductor demand by 8% annually in this sector.

Competitive overview of Power Semiconductor Market

The major players operating in the power semiconductor market include Infineon Technologies AG, Texas Instruments Inc., STMicroelectronics NV, Toshiba Corporation, Mitsubishi Electric Corporation, Renesas Electronic Corporation, Broadcom Inc., ON Semiconductor Corporation, ROHM Co., Ltd., Nexperia BV, Fuji Electric Co., Ltd., NXP Semiconductors N.V., Renesas Electronics Corporation, and Analog Devices Inc.

Power Semiconductor Market Leaders

Infineon Technologies AG

Texas Instruments Inc.

STMicroelectronics NV

Toshiba Corporation

Mitsubishi Electric Corporation

*Disclaimer: Major players are listed in no particular order.

Power Semiconductor Market - Competitive Rivalry

Power Semiconductor Market

Market Consolidated (Dominated by major players)

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Power Semiconductor Market

In May 2024, Polar Semiconductor announced plans to expand its existing manufacturing facility in Bloomington, Minnesota, with a $525 million investment aimed at enhancing production capabilities. This expansion is expected to double the company's production capacity from approximately 20,000 wafers per month to nearly 40,000 wafers per month.

In April 2024, Fuji Electric introduced the HPnC Series, a new line of large-capacity industrial IGBT modules designed for applications such as power converters in solar and wind power generation systems.

In January 2024, Texas Instruments (TI) introduced the AWR2544, a 77GHz millimeter-wave radar sensor chip designed to enhance automotive safety. This chip is the industry's first single-chip radar sensor tailored for satellite radar architectures, which output semi-processed data to a central processor for advanced driver assistance systems (ADAS) decision-making.

Power Semiconductor Market Report - Table of Contents

RESEARCH OBJECTIVES AND ASSUMPTIONS

Research Objectives

Assumptions

Abbreviations

MARKET PURVIEW

Report Description

Market Definition and Scope

Executive Summary

Power Semiconductor Market, By Component

Power Semiconductor Market, By Material

Power Semiconductor Market, By End-user Industry

Coherent Opportunity Map (COM)

MARKET DYNAMICS, REGULATIONS, AND TRENDS ANALYSIS

Market Dynamics

Impact Analysis

Key Highlights

Regulatory Scenario

Product Launches/Approvals

PEST Analysis

PORTER’s Analysis

Merger and Acquisition Scenario

Global Power Semiconductor Market, By Component, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Power Integrated Circuits

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Discrete

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Module

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Power Semiconductor Market, By Material, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Silicon/Germanium

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Silicon Carbide (SiC)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Gallium Nitride (GaN)

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Power Semiconductor Market, By End-user Industry, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Automotive Industry

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Consumer Electronics Industry

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Military and Aerospace Industry

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

IT and Telecommunication Industry

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Industrial Industry

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Other End-User Industries

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Power Semiconductor Market, By Region, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-user Industry, 2020-2032, Value (USD Bn)

U.S.

Canada

Latin America

Introduction

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-user Industry, 2020-2032, Value (USD Bn)

Brazil

Argentina

Mexico

Rest of Latin America

Europe

Introduction

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-user Industry, 2020-2032, Value (USD Bn)

Germany

U.K.

Spain

France

Italy

Russia

Rest of Europe

Asia Pacific

Introduction

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-user Industry, 2020-2032, Value (USD Bn)

China

India

Japan

Australia

South Korea

ASEAN

Rest of Asia Pacific

Middle East

Introduction

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-user Industry, 2020-2032, Value (USD Bn)

GCC Countries

Israel

Rest of Middle East

Africa

Introduction

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

Market Size and Forecast, By End-user Industry, 2020-2032, Value (USD Bn)

South Africa

North Africa

Central Africa

COMPETITIVE LANDSCAPE

Infineon Technologies AG

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Texas Instruments Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

STMicroelectronics NV

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Toshiba Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Mitsubishi Electric Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Renesas Electronic Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Broadcom Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

ON Semiconductor Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

ROHM Co., Ltd.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Nexperia BV

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Fuji Electric Co., Ltd.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

NXP Semiconductors N.V.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Renesas Electronics Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analog Devices, Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analyst Recommendations

Wheel of Fortune

Analyst View

Coherent Opportunity Map

References and Research Methodology

References

Research Methodology

About us

Power Semiconductor Market Segmentation

By Component

Power Integrated Circuits

Discrete

Module

By Material

Silicon/Germanium

Silicon Carbide (SiC)

Gallium Nitride (GaN)

By End-user Industry

Automotive Industry

Consumer Electronics Industry

Military and Aerospace Industry

IT and Telecommunication Industry

Industrial Industry

Other End-User Industries

Would you like to explore the option of buying individual sections of this report?

About author

As an accomplished Senior Consultant with 7+ years of experience, Pooja Tayade has a proven track record in devising and implementing data and strategy consulting across various industries. She specializes in market research, competitive analysis, primary insights, and market estimation. She excels in strategic advisory, delivering data-driven insights to help clients navigate market complexities, optimize entry strategies, and achieve sustainable growth.

Frequently Asked Questions :

How big is the power semiconductor market?

The power semiconductor market is estimated to be valued at USD 55.03 Bn in 2025 and is expected to reach USD 75.90 Bn by 2032.

What are the key factors hampering the growth of the power semiconductor market?

The high costs and complexity of power semiconductors and challenges in thermodynamic resistance and environmental exposure are the major factor hampering the growth of the power semiconductor market.

What are the major factors driving the power semiconductor market growth?

The rising demand for industrial automation and development of energy-efficient devices are the major factor driving the power semiconductor market.

Which is the leading component in the power semiconductor market?

The leading component segment is power integrated circuits.

Which are the major players operating in the power semiconductor market?

Infineon Technologies AG, Texas Instruments Inc., STMicroelectronics NV, Toshiba Corporation, Mitsubishi Electric Corporation, Renesas Electronic Corporation, Broadcom Inc., ON Semiconductor Corporation, ROHM Co., Ltd., Nexperia BV, Fuji Electric Co., Ltd., NXP Semiconductors N.V., Renesas Electronics Corporation, and Analog Devices Inc. are the major players.

What will be the CAGR of the power semiconductor market?

The CAGR of the power semiconductor market is projected to be 4.7% from 2025-2032.

Missing comfort of reading report in your local language? Find your preferred language :

Insights, By Material: Ascendance of Wide Bandgap Materials

Insights, By Material: Ascendance of Wide Bandgap Materials