Wind Turbine Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Wind Turbine Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Wind Turbine Market is segmented By Axis (Vertical, Horizontal), By Installation(Onshore, Offshore), By Component (Rotator Blade, Generator, Gearbox, Nacelle), By Application (Residential, Utility, Industrial, Commercial), By Geography (North America, Latin America, Asia Pacific, Europe, Middle East, and Africa) . The report offers the value (in USD billion) for the above-mentioned segments.

Wind Turbine Market is segmented By Axis (Vertical, Horizontal), By Installation(Onshore, Offshore),...

Wind Turbine Market Size - Analysis

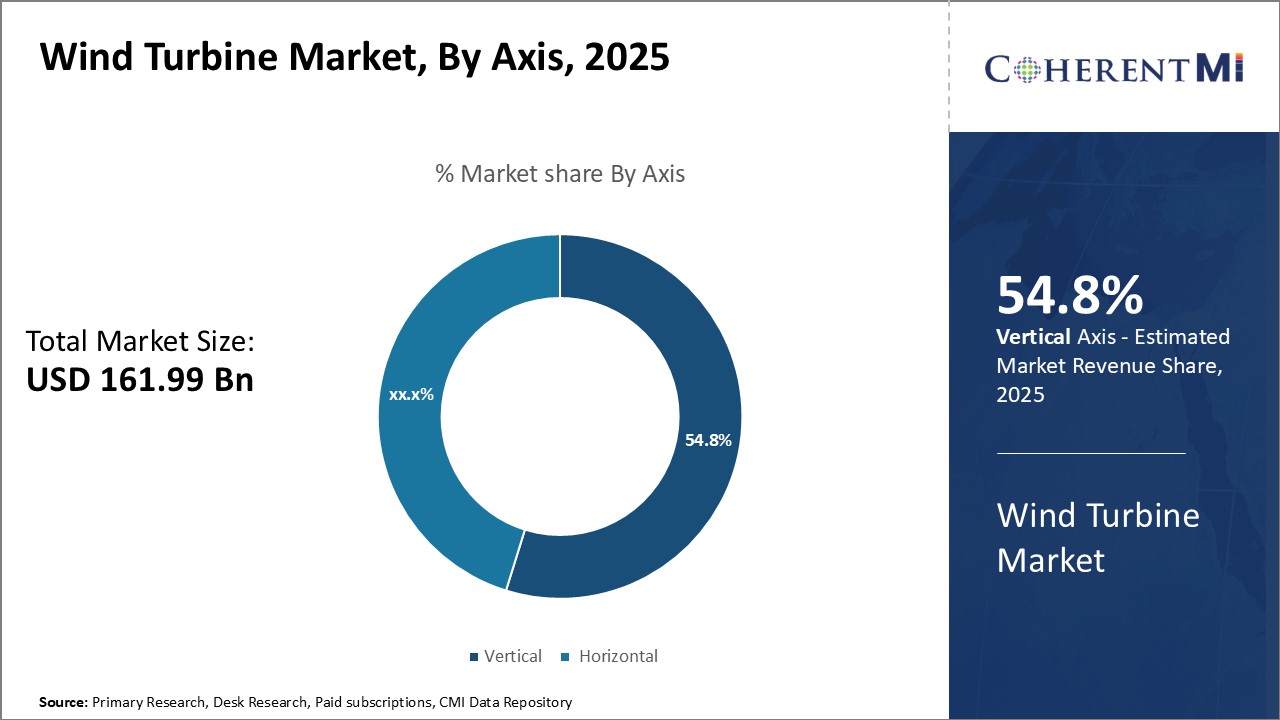

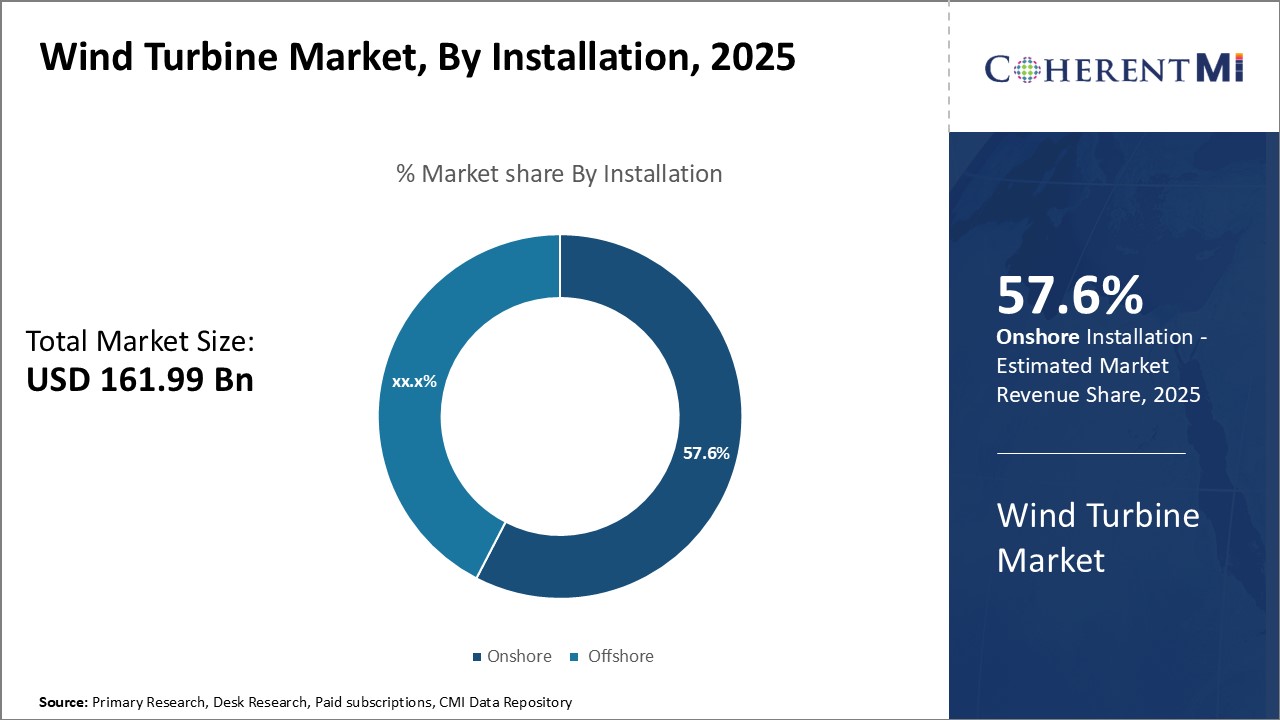

The wind turbine market is estimated to be valued at USD 161.99 Bn in 2025 and is expected to reach USD 277.62 Bn by 2032. It is projected to grow at a compound annual growth rate (CAGR) of 8.00% from 2025 to 2032. The wind turbine market has been witnessing significant growth driven by supportive government policies and regulations towards adoption of renewable sources of energy.

Market Size in USD Bn

CAGR8.00%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

8.00%

Market Concentration

Medium

Major Players

General Electric Company, Vestas Wind Systems A/S, Nordex SE, Suzlon Energy Limited, Siemens Gamesa Renewable Energy SA and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

Wind Turbine Market Trends

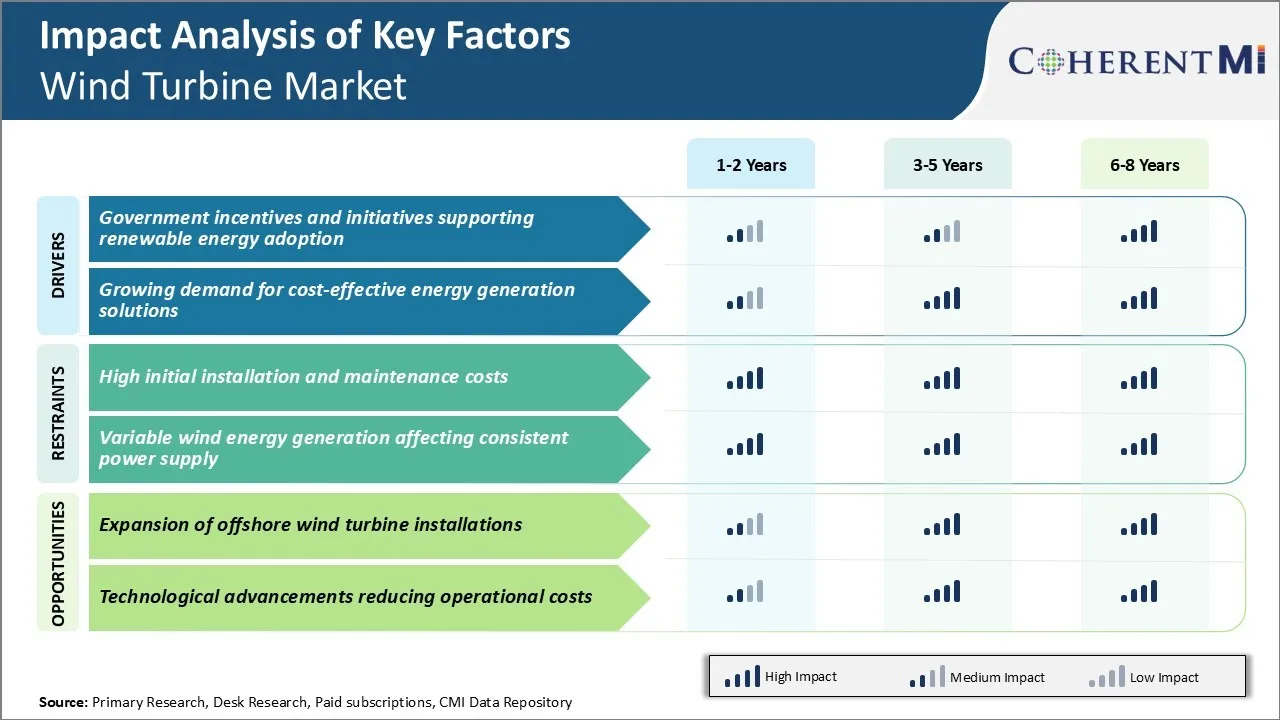

Market Driver - Government Incentives and Initiatives Supporting Renewable Energy Adoption

Various governments around the world have introduced attractive incentives and policies to promote the use of renewable energy sources like wind power. This has significantly boosted the setting up of new wind farms in recent years. Many countries have set ambitious targets to increase the share of electricity generated from renewable resources as part of their commitments to reduce carbon emissions under the Paris Agreement. Achieving these targets requires massive investments in wind energy projects.

Governments offer lucrative tax incentives, rebates, and financial subsidies for both residential and utility-scale wind turbine installations. This makes wind power projects more viable economically for developers and lowers the per unit cost of energy generated. Overall, the growing policy push and financial assistance to boost renewable energy adoption is a driving factor augmenting investments and installations in the wind turbine market.

Market Driver - Growing Demand for Cost-effectiveEnergy Generation Solutions

Soaring energy consumption worldwide along with rising electricity tariffs has intensified the need for reliable and affordable power sources across both developed and emerging economies. Meanwhile, traditional fossil fuel-based thermal generation is becoming increasingly expensive due to higher input costs and stricter emission norms.

This is propelling governments and large corporate buyers to explore renewable resources like wind that offer long-term electricity price stability along with environmental sustainability. Wind energy, in particular, is gaining popularity due to continual improvements in technology that have made it competitive against conventional power sources on cost.

Renewable costs are declining further with technological progress. Thereby, their price appeal compared to fossil alternatives will increase substantially over the coming decade. This will propel even greater demand for wind and solar installations as preferred choices for utility-level and distributed power generation.

Market Challenge - High Initial Installation and Maintenance Costs

The high initial capital costs associated with installing wind turbines poses a significant challenge for the wind turbine market. Setting up both onshore and offshore wind farms requires massive upfront investments in purchasing and transporting large turbine components, foundations, cables, and substations.

For example, the average cost of installing an onshore wind turbine range between $1-2 million. On the other hand, an offshore turbine can cost upwards of $5 million due to additional expenses related to ocean logistics and infrastructure.

Furthermore, wind turbines have a lifespan of only 15-25 years and require regular scheduled and unscheduled maintenance to operate efficiently. Maintenance activities such as replacing worn components, painting, repairing blades and gearboxes generate substantial operating expenditures over the project lifetime.

The remote offshore locations further increase maintenance costs due to expenses related to vessels, crews and necessary downtime. With competition from relatively cheaper conventional power sources, high capital costs pose a considerable barrier for large scale adoption of wind turbine technology.

Market Opportunity - Expansion of Offshore Wind Turbine Installations

The expansion of offshore wind turbine installations across the world presents a major opportunity for the wind turbine market. Compared to onshore sites, offshore areas experience stronger and more consistent winds, allowing for larger, more productive turbines to be deployed. This translates to higher energy yields and returns on investment.

Many coastal nations are increasingly tapping into their vast offshore potential. They are and setting ambitious renewable targets that promise robust demand for offshore wind turbine projects in the coming decades. For example, countries like China, UK, Germany and others have outlined plans to install thousands of megawatts of offshore capacity through the 2020s and beyond.

Driven by supportive policies, technological advancements, and falling costs of offshore solutions, the global offshore wind turbine market is projected to grow at double digit rates over the next 10 years. Established and new players in the wind turbine market stand to benefit from proliferation of utility-scale offshore wind farms worldwide.

Key winning strategies adopted by key players of Wind Turbine Market

Strategy #1: Focus on innovation and R&D to develop advanced wind turbine technologies

Some of the major players like Vestas, Siemens Gamesa, General Electric have invested heavily in R&D to develop more efficient and powerful wind turbines.

Strategy #2: Pursue strategic acquisitions and partnerships for business expansion

Many companies have acquired or partnered with other players to expand their portfolio and geographic reach. For instance, in 2017, Siemens acquired Gamesa to become a global leader. Vestas partnered with Mitsubishi in 2018 for cooperation in developing offshore wind turbines.

Strategy #3: Focus on lowering levelized cost of energy (LCOE) through economies of scale

Players focus on increasing turbine size to reduce LCOE. For example, Vestas launched its largest onshore turbines V162-6.0 MW and V168-8.0 MW in 2019 and 2020 respectively. This allowed 10-15% reduced LCOE. GE launched its Haliade-X 12 MW offshore turbine in 2020, the most powerful one today.

Strategy #4: Expand to growing end-markets through timely market entry

Majority of demand is now coming from offshore and emerging markets. Vestas and Siemens Gamesa have proven successful due to their early focus on these opportunities.

Segmental Analysis of Wind Turbine Market

Insights, By Axis: Heightened Stability Drives Vertical Axis Segment Growth

In terms of axis, vertical contributes 54.8% share of the wind turbine market owning to its inherent stability compared to horizontal designs. Vertical axis turbines can operate in a wide range of wind directions without needing to mechanically change orientation. This makes installation and maintenance far simpler as there is no gearbox or motor needed for orientation.

The lack of complex internal components like gearboxes that are failure prone in horizontal designs further boosts reliability. Vertical turbines can operate continuously for a very long period without any interruptions even in turbulent wind conditions. This stability attracts many industrial and commercial customers who desire an uninterrupted power supply for their critical operations and equipment.

Inherent stability of vertical wind turbines compared to other axis orientations has cemented vertical axis segment's dominance in the current wind turbine market.

Insights, By Installation: Terrestrial Access Drives Onshore Segment Leadership

In terms of installation, onshore installation contributes 57.6% share of the wind turbine market. This is owing to simpler access and deployment on land areas. Setting up wind turbines offshore requires specialized heavy-lift vessels and equipment along with complicated installation procedures at sea. High costs associated with equipment mobilization, transportation to site and actual installation at sea deter many project developers and operators.

Abundance of suitable relatively larger smooth land parcels in close proximity to demand centers aid concentrating more turbine installations onshore. Siting wind farms near towns and cities enables lower line losses during power evacuation through existing grids. This synergistic co-location with transmission infrastructure and load centers amplifies onshore segment growth in the wind turbine market.

Insights, By Component: Enhanced Durability Powers Rotating Blade Dominance

In terms of component, rotating blade contributes the highest share of the wind turbine market in 2024. This is due to advancements improving its longevity. Modern wind turbine rotating blades are engineered with durable composite materials like glass and carbon fiber reinforced polymers that withstand high centrifugal stresses better.

Sophisticated aerodynamic profiling and variable pitch capabilities help optimizing energy extraction even during transient gusty winds. Advanced coating technologies further augment blade service life by protecting against environmental degradation. Rotor blades therefore last significantly longer now without needing replacements, lowering lifecycle costs.

In summary, rotating blades have emerged as the flagship component driving higher penetration of wind turbines owing to longevity leadership achieved through cutting-edge material and engineering developments. This entrenched dominance is likely to hold strong in the wind turbine market going forward as well.

Additional Insights of Wind Turbine Market

The Asia-Pacific region holds the largest share of the global wind turbine market due to substantial wind power generation capabilities and favorable government policies.

Offshore installations are gaining traction with innovations like taller turbines and larger blades for improved efficiency.

The Asia-Pacific region in the global wind turbine market accounted for 59% share in 2023.

China and India dominate the Asia-Pacific market for wind turbines due to large-scale wind energy projects.

Competitive overview of Wind Turbine Market

The major players operating in the wind turbine market include General Electric Company, Vestas Wind Systems A/S, Nordex SE, Suzlon Energy Limited, Siemens Gamesa Renewable Energy SA, China Shipbuilding Industry Corporation, Shanghai Electric, Windey Energy Technology Group Co Ltd, Goldwind Science & Technology Co., Ltd., Ming Yang Smart Energy Group Co. Ltd., Suzlon Energy Limited, Enercon GmbH, Envision Group, and Senvion S.A.

Wind Turbine Market Leaders

General Electric Company

Vestas Wind Systems A/S

Nordex SE

Suzlon Energy Limited

Siemens Gamesa Renewable Energy SA

*Disclaimer: Major players are listed in no particular order.

Wind Turbine Market - Competitive Rivalry

Wind Turbine Market

Market Consolidated (Dominated by major players)

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Wind Turbine Market

In October 2023, GE Vernova’s Onshore Wind business (part of GE Renewable Energy) announced that it had been selected by JSW Energy to supply onshore wind turbines totaling 810 MW for projects in Tamil Nadu, India.

In January 2023, Vestas announced that it had secured an order for 116 MW of onshore wind turbines for the Pantelimon and Apollo wind projects in Romania (a country considered part of Eastern Europe). The projects were for DTEK Renewables International and represented a meaningful regional contract.

Wind Turbine Market Report - Table of Contents

RESEARCH OBJECTIVES AND ASSUMPTIONS

Research Objectives

Assumptions

Abbreviations

MARKET PURVIEW

Report Description

Market Definition and Scope

Executive Summary

Wind Turbine Market, By Axis

Wind Turbine Market, By Installation

Wind Turbine Market, By Component

Wind Turbine Market, By Application

Coherent Opportunity Map (COM)

MARKET DYNAMICS, REGULATIONS, AND TRENDS ANALYSIS

Market Dynamics

Impact Analysis

Key Highlights

Regulatory Scenario

Product Launches/Approvals

PEST Analysis

PORTER’s Analysis

Merger and Acquisition Scenario

Global Wind Turbine Market, By Axis, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Vertical

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Horizontal

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Wind Turbine Market, By Installation, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Onshore

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Offshore

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Wind Turbine Market, By Component, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Rotator Blade

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Generator

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Gearbox

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Nacelle

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Wind Turbine Market, By Application, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Residential

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Utility

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Industrial

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Commercial

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Wind Turbine Market, By Region, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Axis, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Installation, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

U.S.

Canada

Latin America

Introduction

Market Size and Forecast, By Axis, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Installation, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

Brazil

Argentina

Mexico

Rest of Latin America

Europe

Introduction

Market Size and Forecast, By Axis, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Installation, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

Germany

U.K.

Spain

France

Italy

Russia

Rest of Europe

Asia Pacific

Introduction

Market Size and Forecast, By Axis, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Installation, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

China

India

Japan

Australia

South Korea

ASEAN

Rest of Asia Pacific

Middle East

Introduction

Market Size and Forecast, By Axis, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Installation, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

GCC Countries

Israel

Rest of Middle East

Africa

Introduction

Market Size and Forecast, By Axis, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Installation, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Component, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

South Africa

North Africa

Central Africa

COMPETITIVE LANDSCAPE

General Electric Company

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Vestas Wind Systems A/S

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Nordex SE

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Suzlon Energy Limited

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Siemens Gamesa Renewable Energy SA

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

China Shipbuilding Industry Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Shanghai Electric

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Windey Energy Technology Group Co Ltd

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Goldwind Science & Technology Co., Ltd.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Ming Yang Smart Energy Group Co. Ltd.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Suzlon Energy Limited

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Enercon GmbH

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Envision Group

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Senvion S.A.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analyst Recommendations

Wheel of Fortune

Analyst View

Coherent Opportunity Map

References and Research Methodology

References

Research Methodology

About us

Wind Turbine Market Segmentation

By Axis

Vertical

Horizontal

By Installation

Onshore

Offshore

By Component

Rotator Blade

Generator

Gearbox

Nacelle

By Application

Residential

Utility

Industrial

Commercial

Would you like to explore the option of buying individual sections of this report?

About author

Sakshi Suryawanshi is a Research Consultant with 6 years of extensive experience in market research and consulting. She is proficient in market estimation, competitive analysis, and patent analysis. Sakshi excels in identifying market trends and evaluating competitive landscapes to provide actionable insights that drive strategic decision-making. Her expertise helps businesses navigate complex market dynamics and achieve their objectives effectively.

Frequently Asked Questions :

How big is the wind turbine market?

The wind turbine market is estimated to be valued at USD 161.99 Bn in 2025 and is expected to reach USD 277.62 Bn by 2032.

What are the key factors hampering the growth of the wind turbine market?

High initial installation and maintenance costs and variable wind energy generation affecting consistent power supply are the major factors hampering the growth of the wind turbine market.

What are the major factors driving the wind turbine market growth?

Government incentives and initiatives supporting renewable energy adoption and growing demand for cost-effective energy generation solutions are the major factors driving the wind turbine market.

Which is the leading axis in the wind turbine market?

The leading axis segment is vertical.

Which are the major players operating in the wind turbine market?

General Electric Company, Vestas Wind Systems A/S, Nordex SE, Suzlon Energy Limited, Siemens Gamesa Renewable Energy SA, China Shipbuilding Industry Corporation, Shanghai Electric, Windey Energy Technology Group Co Ltd, Goldwind Science & Technology Co., Ltd., Ming Yang Smart Energy Group Co. Ltd., Suzlon Energy Limited, Enercon GmbH, Envision Group, and Senvion S.A. are the major players.

What will be the CAGR of the wind turbine market?

The CAGR of the wind turbine market is projected to be 8.00% from 2025-2032.

Missing comfort of reading report in your local language? Find your preferred language :

Insights, By Installation: Terrestrial Access Drives Onshore Segment Leadership

Insights, By Installation: Terrestrial Access Drives Onshore Segment Leadership