Low Carbon Building Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Low Carbon Building Market SIZE AND SHARE ANALYSIS - GROWTH TRENDS AND FORECASTS (2025-2032)

Low Carbon Building Market is segmented By Type (Energy-Efficient Materials, Renewable Energy Systems, Low Carbon HVAC Systems, Green Building Certifications, Others), By Application(Commercial, Residential, Industrial), By Material, (Wood, Bamboo, Recycled Steel, Recycled Plastic, Other Sustainable Materials), By Geography (North America, Latin America, Asia Pacific, Europe, Middle East, and Africa). The report offers the value (in USD billion) for the above-mentioned segments.

Low Carbon Building Market is segmented By Type (Energy-Efficient Materials, Renewable Energy System...

Low Carbon Building Market Size - Analysis

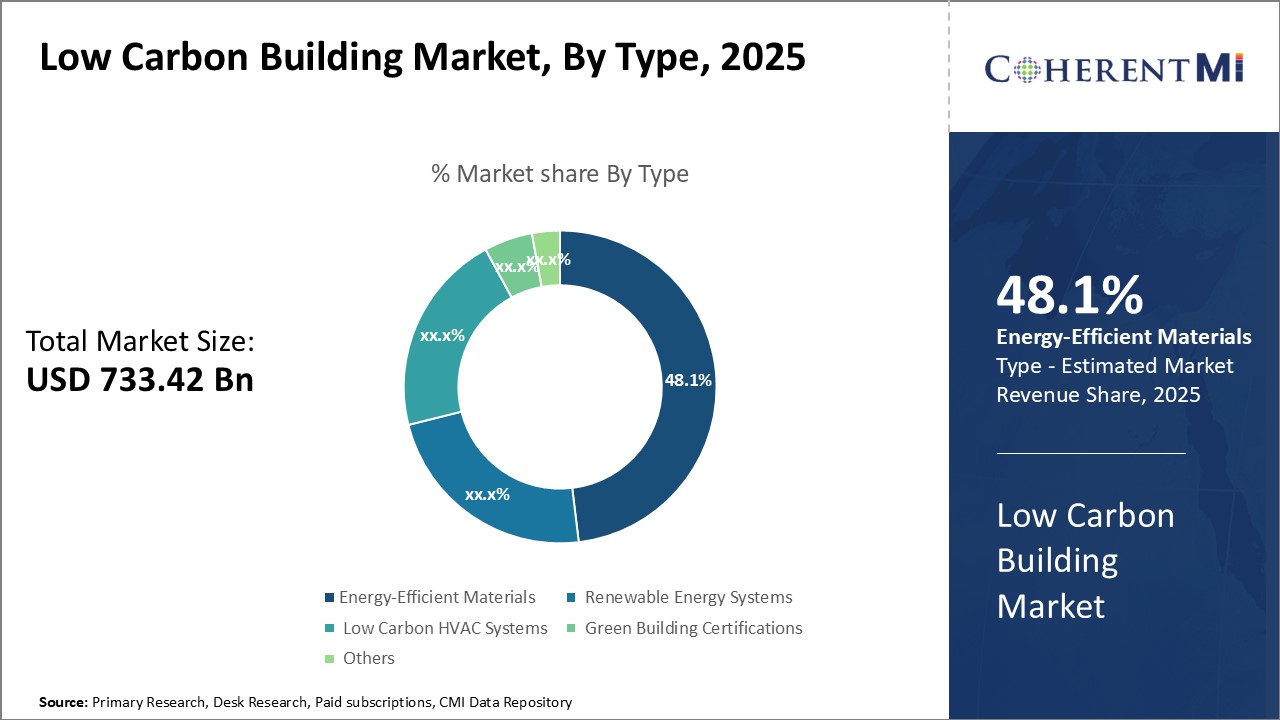

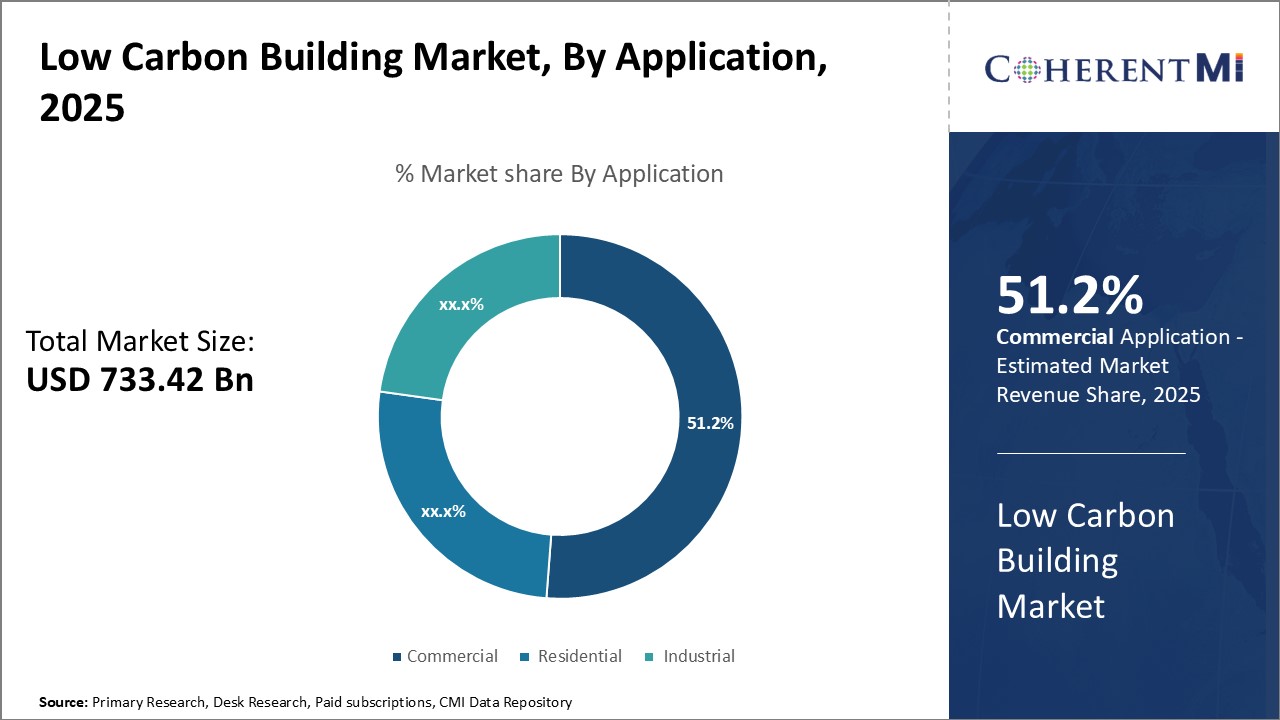

The low carbon building market is estimated to be valued at USD 733.42 Bn in 2025 and is expected to reach USD 1621.36 Bn by 2032, growing at a compound annual growth rate (CAGR) of 12.00% from 2025 to 2032. The low carbon building market is driven by the need for renewable energy solutions and efforts to reduce greenhouse gas emissions from the building sector.

Market Size in USD Bn

CAGR12.00%

Study Period

2025-2032

Base Year of Estimation

2024

CAGR

12.00%

Market Concentration

High

Major Players

Siemens AG, Honeywell International Inc., Johnson Controls International plc, Schneider Electric SE, Trane Technologies plc and Among Others

*Disclaimer: Major players are listed in no particular order.

*Source: Coherent Market Insights

Want to purchase customized report? please let us know !

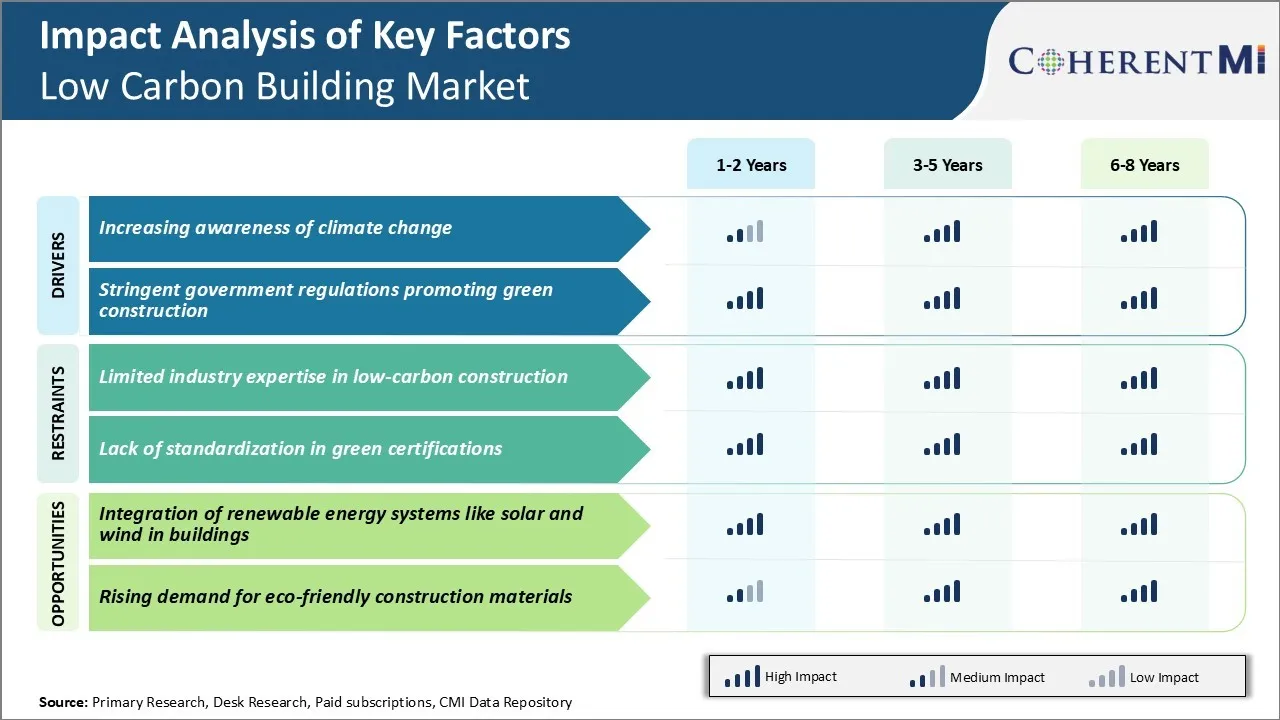

Low Carbon Building Market Trends

Market Driver - Increasing Awareness of Climate Change

As the impacts of climate change become more apparent through extreme weather events, people are becoming increasingly concerned about global warming. As awareness increases, more people are educating themselves on the relationship between buildings and climate change.

The materials, construction, and day-to-day functioning of a conventional building releases a lot of carbon into the atmosphere over its lifetime. Customers are realizing that the choices made regarding a building's design and operation can significantly help or hamper global efforts to curb climate change. This realization is driving demand for low carbon buildings which are energy efficient, use sustainable materials, and integrate renewable energy to reduce their environmental impact.

Developers and building owners have taken note of this shifting consumer sentiment. They know that being perceived as sustainability leaders can help their branding and give them a competitive edge in the low carbon building market. Manufacturers of green building products have ramped up research & development to meet the growing needs of an eco-conscious customer base. Overall awareness of how buildings link to global warming has become a major driver propelling the low carbon building market.

Market Driver - Stringent Government Regulations Promoting Green Construction

In response to public demand for stronger climate policy, many governments worldwide have introduced stricter building codes and regulations in recent years. These are aimed at curbing emissions from the building sector by mandating greater energy efficiency in new construction.

For example, the European Union has set sector-specific benchmarks through its Energy Performance of Buildings Directive which member states must implement at a domestic level. In the US, states like California and New York have led the nation with some of the toughest low carbon building standards domestically.

Financial incentives are also being put in place to encourage green building practices. Tax credits are offered for developments that pursue third party green certifications from LEED, Living Building Challenge, Passive House etc. Public funding supports research into innovative low carbon building materials and systems.

Governments are demonstrating that green building is a public policy priority, generating greater investor interest and private sector commitment towards low carbon solutions. Over time, regulations are anticipated to become even more rigorous, ensuring this remains a main growth driver for the low carbon building market.

Market Challenge - Limited Industry Expertise in Low-carbon Construction

One of the key challenges currently facing the low-carbon buildings market is the limited industry expertise in designing, building and operating truly low-carbon structures. While there is growing awareness of the importance of reducing embodied and operational carbon in buildings, traditional building practices were not developed with sustainability as a core priority.

As a result, most construction firms, architects, engineers and tradespeople have relatively little hands-on experience delivering projects that minimize carbon footprint. This creates execution risks around ensuring designs that prioritize low-carbon outcomes can still be built cost-effectively within typical construction timeframes and budgets. There is also a shortage of specialists with in-depth knowledge around evolving low-carbon building technologies, materials, and processes.

Overcoming these expertise gaps will require significant training and upskilling of the existing industry workforce. Players in the low carbon building market will also need to change procurement processes to properly incentivize low-carbon design and construction practices.

Market Opportunity - Integration of Renewable Energy Systems like Solar and Wind in Buildings

One major opportunity for the low-carbon buildings market lies in more comprehensive integration of renewable energy systems directly into building design. By generating clean power on-site through solar photovoltaic panels, small wind turbines, or other renewable microgeneration technologies, buildings can substantially reduce their reliance on dirtier grid electricity and lower operational carbon footprint.

With renewable energy technology costs declining, building-integrated applications have become increasingly economically viable compared to traditional construction. Forward-looking developers see significant value in developing expertise around optimizing building envelopes, roofs, facades and other elements to harvest clean energy.

As policies like renewable portfolio standards increase demand for such systems, skills around “building as a power plant” have potential for growth. Adoption of integrated renewables also helps building owners reduce long-term energy costs through revenue from excess power fed back to the grid.

Key winning strategies adopted by key players of Low Carbon Building Market

Focus on energy efficiency and renewable energy sources: Players like Schneider Electric, Johnson Controls and United Technologies Corp have focused heavily on making buildings more energy efficient through various technologies and solutions.

Adopt whole building design approach: Leaders like Siemens, Johnson Controls and Honeywell have advocated for a whole building design approach where low carbon strategies are integrated from the design phase itself rather than as add-ons.

Offer building life-cycle services: Majority of the top players like Johnson Controls, Honeywell and Schneider Electric have transitioned from being product vendors to offering comprehensive building life-cycle services like energy audits, retrofits, facility management etc.

Partnerships and acquisitions: Players grow capabilities and market share through strategic partnerships and acquisitions. For example, in 2021 Johnson Controls acquired Tempered Networks to enhance its building cybersecurity portfolio.

Segmental Analysis of Low Carbon Building Market

Insights, By Type: Growing Awareness of Energy Efficiency Drives Demand for Energy-Efficient Materials

In terms of product type, energy-efficient materials contribute 48.1% share in the low carbon building market in 2025. This is due to growing awareness about energy efficiency among builders and consumers. Various energy-efficient material options such as insulated glazing, aerogel insulation, radiant barrier sheathing, and insulating concrete forms allow builders to significantly reduce a building's energy needs for heating and cooling.

Insulated glazing or double/triple glazing is becoming a standard in commercial and residential construction due to its ability to prevent heat transfer through windows. The extra layers of glass and insulating gas in between drastically reduce conduction and convection heat losses. Radiant barrier sheathing is another popular energy-efficient building material seeing rising installments. It helps stabilize indoor temperatures and minimize the need for space cooling in hot weather.

Aerogel is an ultra-light synthetic porous material with extremely low thermal conductivity, allowing it to insulate buildings four times better than fiberglass batts of the same thickness. Overall, the energy and money savings potential of advanced insulations like aerogel are boosting their acceptance in the low carbon building market.

Insights, By Applications: Commercial Buildings Lead Adoption of Low Carbon Technologies

The commercial sector accounts for 51.2% share of the low carbon building market in 2025 in terms of applications. It is due to the scale of construction activity and focus on energy management. Commercial builders have strong incentives for low carbon building designs to reduce operating expenses and appeal to environmentally-conscious tenants.

Low carbon HVAC systems find widespread adoption in the commercial segment. District energy plants with cogeneration, geothermal and solar thermal capabilities enable commercial parks and campuses to access clean heating and cooling in an efficient, low emissions manner. Chilled beam systems are also gaining traction as they use 30-50% less energy than standard variable air volume units while maintaining occupant comfort.

Low carbon building certifications continue enhancing the appeal of certified commercial space to businesses invested in sustainability. Measures like adaptive reuse of existing building stock, integration of renewable energy generation and electric vehicle infrastructure further strengthen the green credentials of certified commercial developments. This enables property owners/developers to charge premium rents while meeting business sustainability goals.

Insights, By Material: Wood Emerges as the Carbon-friendly Building Material of Choice

Among different sustainable materials, wood has emerged as the leading low carbon option in the low carbon building market owing to various superior properties. Fast-growing softwood plantations and engineered wood products allow wood buildings to be constructed with a lower embodied carbon footprint compared to alternatives like concrete and steel.

Cradle-to-gate life cycle assessments find wood sequesters more carbon than the amount released during its production, harvesting, transport and eventual disposal. Additionally, wood is a renewable resource that does not require intensive fossil fuel usage in processing like some minerals.

Aesthetically, natural wood finishes are preferred for their warmth and appeal. In the commercial sector, exposed wood interiors are linked to higher occupant well-being, satisfaction, and productivity. This growing recognition of wood's environmental, technical, and experiential merits relative to fossil-intensive alternatives is cementing its position as the material of choice in low carbon building.

Additional Insights of Low Carbon Building Market

The completion of One Central Park in Sydney serves as a prime example of low carbon building practices. The building features vertical gardens and energy-efficient systems, significantly reducing its environmental impact and serving as a model for future sustainable developments.

Buildings account for nearly 40% of global carbon emissions, highlighting the critical need for low carbon construction practices. Adopting sustainable materials and low carbon building technologies could reduce emissions by up to 50% by 2050, according to industry reports.

The energy-efficient materials segment held the largest share (48%) in the global low carbon building market in 2023.

The renewable energy systems segment is projected to grow at a CAGR of 16.1% (2024-2034).

Europe held a 46% revenue share in the global low carbon building market in 2023. Asia Pacific is expected to experience the fastest growth in the global low carbon building market due to government incentives for sustainable construction.

Competitive overview of Low Carbon Building Market

The major players operating in the low carbon building market include Siemens AG, Honeywell International Inc., Johnson Controls International plc, Schneider Electric SE, Trane Technologies plc, Mitsubishi Electric Corporation, ABB Ltd, Kingspan Group plc, Skanska AB, Lendlease Corporation Ltd, LafargeHolcim Ltd., Saint-Gobain, and BASF SE.

Low Carbon Building Market Leaders

Siemens AG

Honeywell International Inc.

Johnson Controls International plc

Schneider Electric SE

Trane Technologies plc

*Disclaimer: Major players are listed in no particular order.

Low Carbon Building Market - Competitive Rivalry

Low Carbon Building Market

Market Consolidated (Dominated by major players)

Market Fragmented (Highly competitive with lots of players.)

*Source: Coherent Market Insights

Recent Developments in Low Carbon Building Market

In 2023, Kingspan Group plc acquired Troldtekt A/S, a Danish company renowned for its sustainable wood-based acoustic panels. This strategic move adds eco-friendly acoustic solutions to Kingspan's product portfolio, further enhancing its focus on low carbon building materials and solutions. The acquisition aligns with Kingspan's commitment to sustainability and innovation in the low carbon building market.

Low Carbon Building Market Report - Table of Contents

RESEARCH OBJECTIVES AND ASSUMPTIONS

Research Objectives

Assumptions

Abbreviations

MARKET PURVIEW

Report Description

Market Definition and Scope

Executive Summary

Low Carbon Building Market, By Type

Low Carbon Building Market, By Application

Low Carbon Building Market, By Material

Coherent Opportunity Map (COM)

MARKET DYNAMICS, REGULATIONS, AND TRENDS ANALYSIS

Market Dynamics

Impact Analysis

Key Highlights

Regulatory Scenario

Product Launches/Approvals

PEST Analysis

PORTER’s Analysis

Merger and Acquisition Scenario

Global Low Carbon Building Market, By Type, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Energy-Efficient Materials

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Renewable Energy Systems

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Low Carbon HVAC Systems

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Green Building Certifications

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Others

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Low Carbon Building Market, By Application, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Commercial

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Residential

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Industrial

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Low Carbon Building Market, By Material, 2025-2032, (USD Bn)

Introduction

Market Share Analysis, 2025-2032 (%)

Y-o-Y Growth Analysis, 2021 - 2032

Segment Trends

Wood

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Bamboo

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Recycled Steel

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Recycled Plastic

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Other Sustainable Materials

Introduction

Market Size and Forecast, and Y-o-Y Growth, 2020-2032, (USD Bn)

Global Low Carbon Building Market, By Region, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

U.S.

Canada

Latin America

Introduction

Market Size and Forecast, By Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

Brazil

Argentina

Mexico

Rest of Latin America

Europe

Introduction

Market Size and Forecast, By Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

Germany

U.K.

Spain

France

Italy

Russia

Rest of Europe

Asia Pacific

Introduction

Market Size and Forecast, By Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

China

India

Japan

Australia

South Korea

ASEAN

Rest of Asia Pacific

Middle East

Introduction

Market Size and Forecast, By Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

GCC Countries

Israel

Rest of Middle East

Africa

Introduction

Market Size and Forecast, By Type, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Application, 2020-2032, Value (USD Bn)

Market Size and Forecast, By Material, 2020-2032, Value (USD Bn)

South Africa

North Africa

Central Africa

COMPETITIVE LANDSCAPE

Siemens AG

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Honeywell International Inc.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Johnson Controls International plc

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Schneider Electric SE

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Trane Technologies plc

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Mitsubishi Electric Corporation

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

ABB Ltd

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Kingspan Group plc

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Skanska AB

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Lendlease Corporation Ltd

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

LafargeHolcim Ltd.

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Saint-Gobain

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

BASF SE

Company Highlights

Product Portfolio

Key Developments

Financial Performance

Strategies

Analyst Recommendations

Wheel of Fortune

Analyst View

Coherent Opportunity Map

References and Research Methodology

References

Research Methodology

About us

Low Carbon Building Market Segmentation

By Type

Energy-Efficient Materials

Renewable Energy Systems

Low Carbon HVAC Systems

Green Building Certifications

Others

By Application

Commercial

Residential

Industrial

By Material

Wood

Bamboo

Recycled Steel

Recycled Plastic

Other Sustainable Materials

Would you like to explore the option of buying individual sections of this report?

About author

Sakshi Suryawanshi is a Research Consultant with 6 years of extensive experience in market research and consulting. She is proficient in market estimation, competitive analysis, and patent analysis. Sakshi excels in identifying market trends and evaluating competitive landscapes to provide actionable insights that drive strategic decision-making. Her expertise helps businesses navigate complex market dynamics and achieve their objectives effectively.

Frequently Asked Questions :

How big is the low carbon building market?

The low carbon building market is estimated to be valued at USD 733.42 Bn in 2025 and is expected to reach USD 1,720.5 Bn by 2032.

What are the key factors hampering the growth of the low carbon building market?

Limited industry expertise in low-carbon construction and lack of standardization in green certifications are the major factors hampering the growth of the low carbon building market.

What are the major factors driving the low carbon building market growth?

Increasing awareness of climate change and stringent government regulations promoting green construction are the major factors driving the low carbon building market.

Which is the leading type in the low carbon building market?

The leading type segment is energy-efficient materials.

Which are the major players operating in the low carbon building market?

Siemens AG, Honeywell International Inc., Johnson Controls International plc, Schneider Electric SE, Trane Technologies plc, Mitsubishi Electric Corporation, ABB Ltd, Kingspan Group plc, Skanska AB, Lendlease Corporation Ltd, LafargeHolcim Ltd., Saint-Gobain, and BASF SE are the major players.

What will be the CAGR of the low carbon building market?

The CAGR of the low carbon building market is projected to be 12.00% from 2025-2032.

Missing comfort of reading report in your local language? Find your preferred language :

Insights, By Applications: Commercial Buildings Lead Adoption of Low Carbon Technologies

Insights, By Applications: Commercial Buildings Lead Adoption of Low Carbon Technologies